In a note to investors Monday, Cowen analyst Vivien Azer wrote that Canada’s cannabis sales in 2020 would reach just $3.2 billion, nearly a third lower than her original estimate of around $4.6 billion. Some of the industry’s biggest names suffered a double whammy as U.S. stock markets dropped by more than 3% as the coronavirus (Covid-19) outbreak continues to spread across the globe.

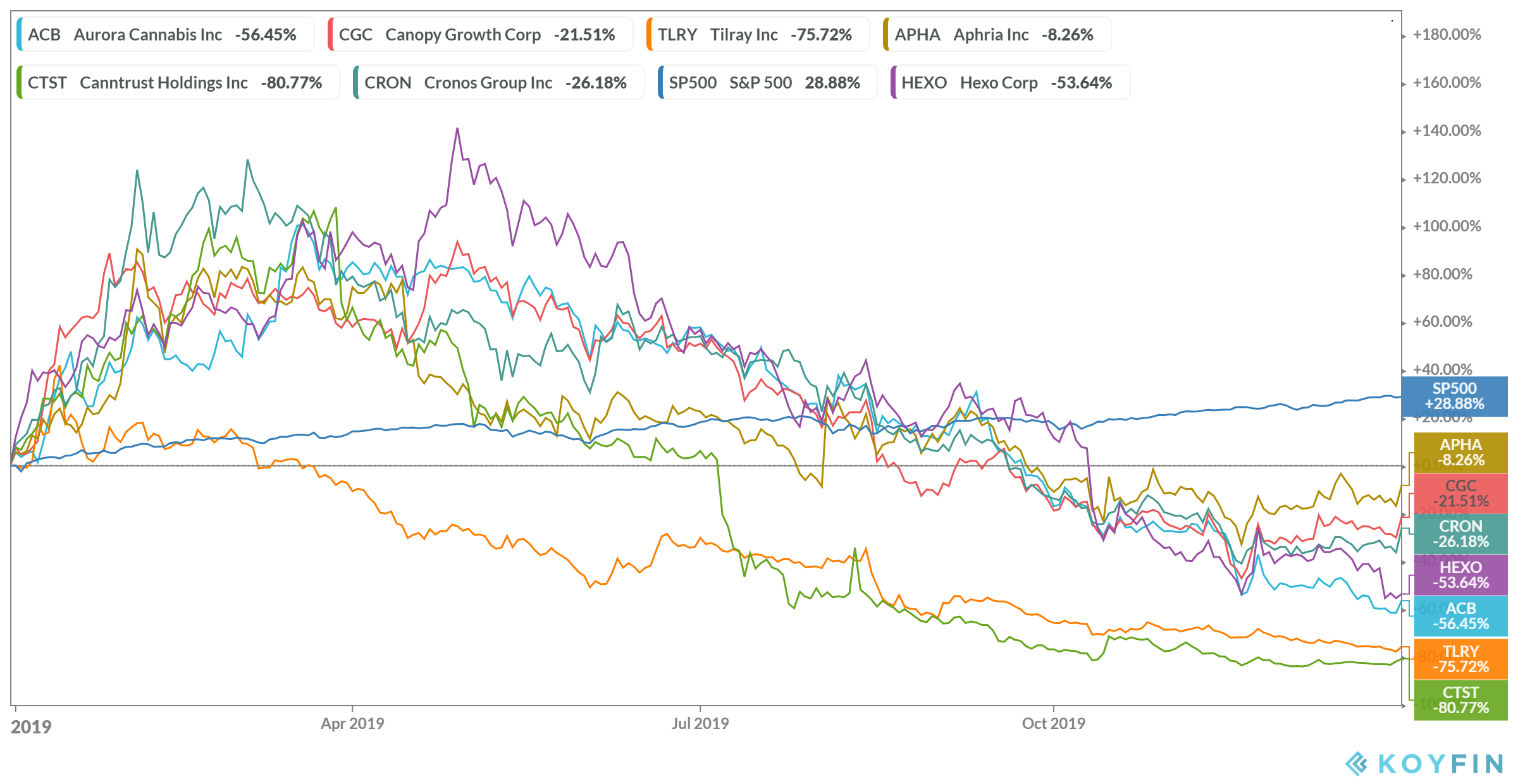

Two top cannabis stocks dropped more than 10% in Monday trading. Cronos Group Inc. (NASDAQ: CRON) fell by 10.9% and Tilray Inc. (NYSE: TLRY) dropped 10.7%. Azer downgraded Tilray, along with Aurora Cannabis Inc. (NYSE: ACB) and Sundial Growers Inc. (NASDAQ: SNDL) to Market Perform from Outperform. Aurora shares fell by 7.2% on Monday and Sundial, defying the odds, added 2.6%.

Cronos was not included in Azer’s downgrade, but likely that’s only because the news from Cronos came too late to be included in her note. The company announced Monday morning that it would not file its fourth-quarter and full-year earnings report on time. There are few things that investors like less than late filings, especially when one of an industry’s top analysts is getting increasingly cautious about that industry’s prospects.

What’s Wrong With Cannabis in Canada

Regulating the new cannabis industry took longer than expected. Legal sales of recreational pot in Canada did not begin until the fall of 2018, even though legislation approving sales was passed almost 18 months earlier. On top of that, Canada’s federal and provincial governments have been slow in approving retail licenses for cannabis retail shops.

In Ontario, Canada’s highest population province, only about two dozen retail stores were open a full year after sales began. The provincial government has been accused of slow-walking the licensing process with its lottery system for selecting license holders. This past December, Ontario replaced the lottery with an open licensing system. That will help, but the industry has a lot of catching up to do.

Given the lack of speed in approving new licenses, cannabis producers turned to cannabis 2.0; that is, edibles and derivatives that extended the industry’s reach beyond smokable pot. Health Canada, the federal agency charged with regulating the cannabis industry, failed to move quickly enough to license derivative products like edibles, vapes, infused beverages, topicals, tinctures and concentrates. These high-margin products were not available until late last year. The sale of derivatives was expected to boost revenues and profits and to keep investors buying stock in Canada’s cannabis companies.

A third big issue facing Canadian cannabis growers is competition, both legal and illegal. There are more than a hundred companies licensed in Canada to grow and sell recreational and medical cannabis. Even if Azer is right about total sales reaching $3.5 billion this year, that’s not a lot of revenue to spread around to so many companies.

The bigger part of the problem, however, is competition from illegal growers. According to Azer, “[W]e now assume that 80 per cent of the market will remain in the illicit trade in 2020, as it seems less clear to us that heightened enforcement will materialize this year to facilitate purchase migration to the legal trade.”

The reason is simple. Illegal pot is a lot cheaper. According to Azer, the average price per gram of dried flower on the illegal market is $5.73, some 80% below the average price of legal marijuana.

How Investors View Canada’s Pot Growers

Last year’s results among Canada’s pot growers were dreadful. Tilray’s stock price dropped by more than 75% while CannTrust Holdings Inc. (NYSE: CTST) saw a plunge of nearly 81%.

It should be no surprise, then, that short sellers are thick on the ground in the pot sector. According to research firm S3 Partners, in 2019 short sellers posted mark-to-market profits net of financing totaling more than $993 million.

On February 24, the same day that Azer’s note was published, short sellers made more than $237 million shorting marijuana stocks. Canopy Growth Corp. (NYSE: CGC) generated mark-to-market profits of $92.5 million for short sellers on that one day alone.

24/7 Wall St.

24/7 Wall St.Short sellers pocketed $31.3 million in profits by betting against Cronos, $41.2 million by shorting Aurora Cannabis and $21.9 million by taking a short position in Tilray.

For the year to date, short sellers were up $107 million after Monday’s collapse. According to S3 Partners, Canopy Growth short sellers were still down $142 million in 2020, while Aurora shorts were up $91 million and Cronos shorts were up $69 million. To date in February, Tilray short sellers have added $5.3 million to their positions.

The value of short interest in Canopy Growth stock is $1.28 billion. Short interest in Cronos totals $46.6 million, while Aurora’s short interest is valued at $352 million. Short interest in Tilray totals $200 million

As a percentage of the company’s float, 15.65% of Tilray stock is short, but that pales next to the 38% of Cronos shares that are held short. The downside is that borrowing shares of the most highly shorted cannabis stocks now commands a fee of around 35%.

Why Tilray Still Might Hold On

Last year, Tilray spent about $55 million to acquire cultivator Natura and $316 million to acquire Manitoba Harvest, a maker of hemp-based edibles. The company then completed a merger with Seattle-based private equity firm Privateer Holdings in December in a deal valued at $2.9 billion.

The company’s cash picture is dim, however. Cash and equivalents dropped from around $487 million in the third quarter of 2018 to $100 million 12 months later. Long-term debt only increased by about $8 million to $428 million in the same period. The net debt to EBITDA ratio dropped from a positive 1.1 times to a negative 2.3 times.

Cash flow from operations dropped from a negative $19.8 million to negative $57 million in the 12 months through September 2019. Capital spending doubled to $24.2 million, and levered free cash flow tumbled from negative $27.5 million to negative $133.2 million.

Tilray has not yet reported fourth-quarter results, but analysts are not expecting much. The net loss per share is estimated at $0.35 and revenues are forecast at $55.76 million. For the fiscal year, the net loss per share is tabbed at $1.40 on sales of $175.14 million.

100 Million Americans Are Missing This Crucial Retirement Tool

The thought of burdening your family with a financial disaster is most Americans’ nightmare. However, recent studies show that over 100 million Americans still don’t have proper life insurance in the event they pass away.

Life insurance can bring peace of mind – ensuring your loved ones are safeguarded against unforeseen expenses and debts. With premiums often lower than expected and a variety of plans tailored to different life stages and health conditions, securing a policy is more accessible than ever.

A quick, no-obligation quote can provide valuable insight into what’s available and what might best suit your family’s needs. Life insurance is a simple step you can take today to help secure peace of mind for your loved ones tomorrow.

Click here to learn how to get a quote in just a few minutes.

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

Latest from 24/7

Our expert who first called NVIDIA in 2009 is predicting 2025 will see a historic AI breakthrough.

You can follow him investing $500,000 of his own money on our top AI stocks for free.