The firm has also said that it is maintaining its preference for large-cap stocks over small-cap ones. In this view, Small caps have continued to underperform since peaking in mid-March. Oppenheimer’s cyclical indicators and relative valuations argue that the trend of small caps underperforming could continue.

Economic data has been generally better in April and May, but corporate capital spending is still a soft spot. While the Institute for Supply Management readings and personal consumption readings have improved, Oppenheimer sees that growth of capital goods new orders remains subdued.

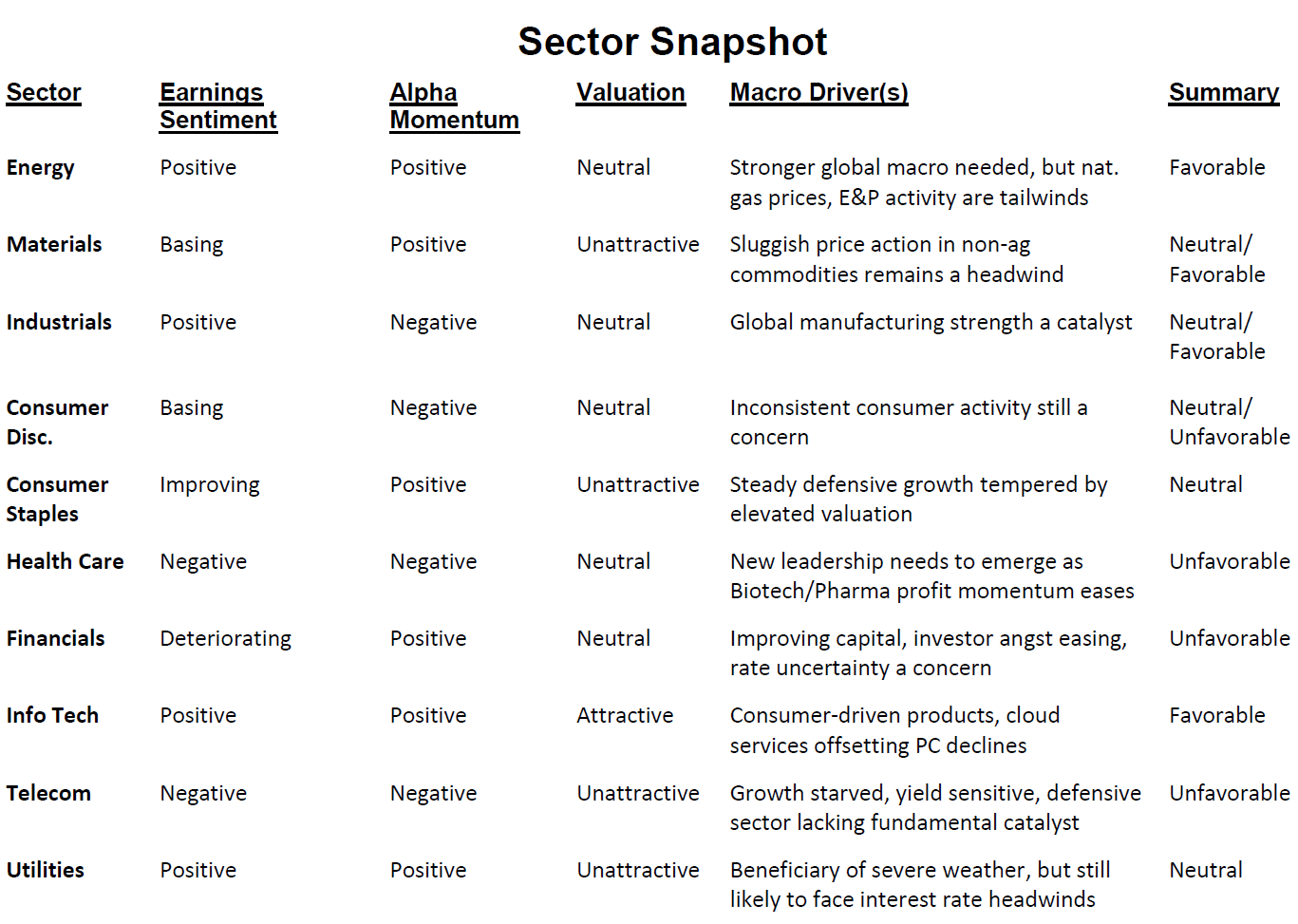

On the sector calls, Oppenheimer said that energy joins information technology as the firm’s most favorably viewed sectors. The note also suggests that industrials and materials are also well positioned to outperform the market.

There are some problem sectors identified as well in the strategy report: financials, health care and telecom. These appear to be the most vulnerable to underperform in the near term. Oppenheimer suggests that the consumer discretionary sector is incrementally looking “less bad” based on potentially stabilizing analyst sentiment for the sector. Also, elevated valuations continue to restrict the prospects for the utilities and consumer staples sectors.

ALSO READ: Five Analyst Stock Picks With 100% or More Implied Upside

After beating earnings estimates in the first quarter, the S&P 500 has seen cuts to second-quarter estimates that are less severe than those seen in recent quarters. What the firm sees here is that this implies a slightly lower level of earnings upside that would likely be realized when companies begin reporting their second-quarter earnings in July. Also of concern here is that there has been a steep ramp in earnings per share growth expected for the second half of 2014 and for 2015, with sales growth of only 2% to 5%.

The team said:

Our Equity Risk Model took another step down this month, leaving it at mildly bullish to neutral readings. Extremely low VIX readings show investor complacency, and stocks are closer to overbought than oversold near-term, by our analysis. The Implied Growth model was little changed as bond yields and earnings yields both fell. The current reading of 2.7% remains somewhat above our expected fair value range of 2.0-2.5%, and is heavily dependent on bond yields remaining low.

A sector-by-sector outlook from Oppenheimer has been provided for your review.