Investing

Renewable deals rack up as oil firms fight for new markets

Published:

Last Updated:

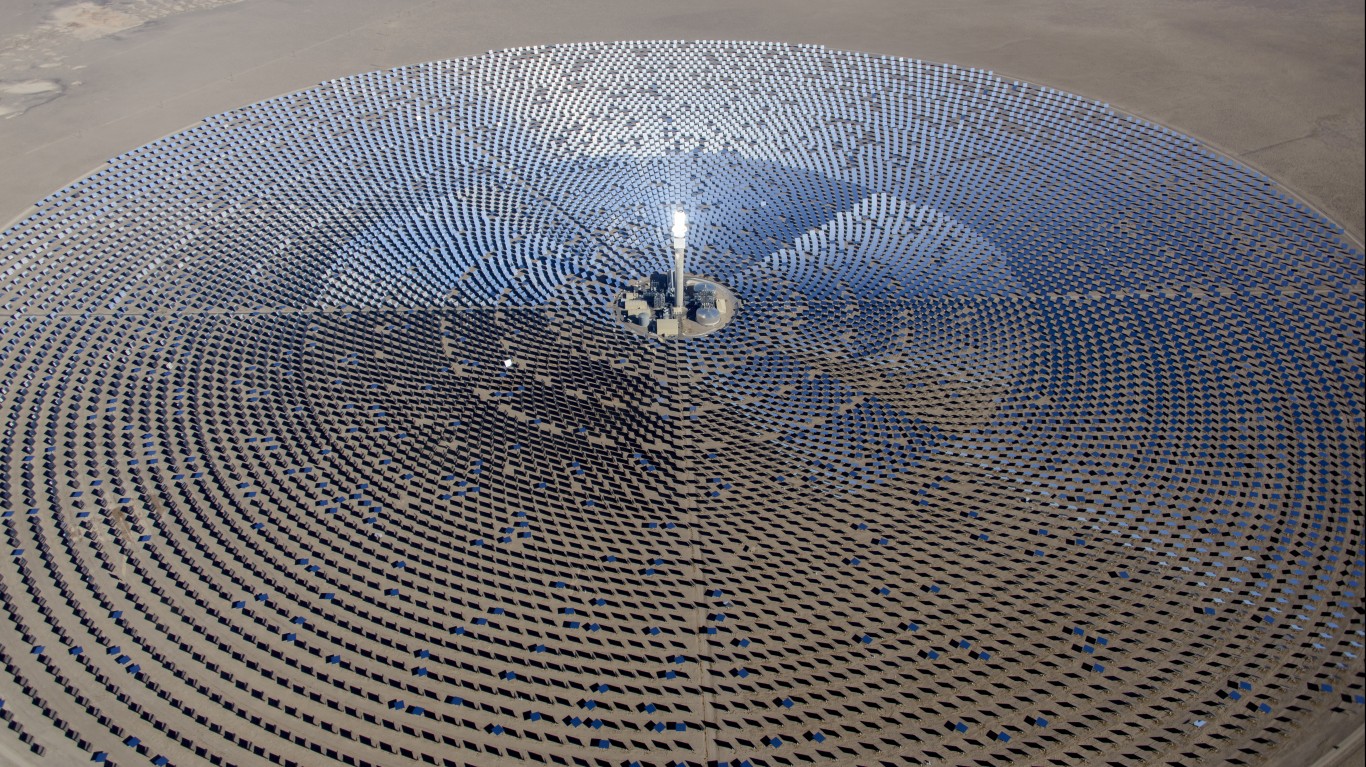

Renewables rule: A large share of the new generating capacity built in the U.S. over the past few years is powered by solar or wind. The U.S. electric power sector added an estimated 14.5 GW of solar generating capacity and about 8.0 GW of wind capacity during the 12 months ending May 31, 2023, according to the U.S. Energy Information Administration. The electric power sector has added an estimated 5.3 GW of battery capacity in the past 12 months, a nearly 90% increase. Above, Crescent Dunes solar project in Nevada.

LONDON (Callaway Climate Insights) — Behind the headlines about energy politics and saving the fossil fuel industry for security from Vladimir Putin in the U.S. and Europe, oil and gas leaders are quietly — and quickly — expanding their renewable portfolios.

As Callaway Climate Insights pointed out last year, the surge in available capital for oil and gas majors as prices soared and oil stocks rose has given them ample cash hoards to pursue acquisitions in the growing renewables industry. Now we’re starting to see deals coming through.

In the past few weeks, Norwegian energy giant Equinor said it will buy onshore wind and solar company Rio Energy of Brazil from its private equity owner, making it one of the largest renewable players in that country. TotalEnergies of France said it would pay $4.2 billion to buy out the remaining 70% of Total Eren, a renewables joint venture, it doesn’t own, shifting its asset mix more toward renewables.

And Exxon $XOM has started talking with EV makers Tesla $TSLA , Ford $F and Volkswagen about supplying them with lithium for their battery operations, as part of a larger foray into lithium mining by oil giant, according to Bloomberg. Lithium mining is a natural adjacent business for a company like Exxon.

Oil leaders realize the world is moving toward renewable energy, and they want to own those businesses. A period of consolidation is inevitable as oil cash meets renewable capital calls to build what TotalEnergies CEO Patrick Pouyanne calls a “profitable integrated power player.”

It may be that the Europeans will move first, but when the big U.S. oil giants start to get more serious, we should expect deals in America as well. Not for nothing are the likes of BlackStone $BX and JPMorgan Chase $JPM suddenly investing in carbon capture technologies.

For investors, this means the rotation back into renewable stocks after almost two years in the wilderness as oil and gas stocks rose, at some point becomes an interesting play. The question is whether it’s sooner or later.

. . . . The never-ending battle over whether investors should engage with fossil fuel firms to make them more climate friendly or divest from them entirely has now spilled into the massive business of private equity, writes Mark Hulbert. Pushing his thesis that divesting from oil companies simply leaves them to do what they want or go private, Hulbert cites a new study that reveals the record of the biggest PE firms on environmental, social and governance standards is almost non-existent, and that the vast majority of their energy holdings are oil and gas companies. . . .

. . . . Any doubts that this fall’s UN climate summit, COP28, would be a celebration of all things carbon capture and storage were dispelled this week when Occidental Petroleum $OXY and COP28 President Sultan Ahmed Al-Jabar’s UAE national oil company announced a deal to explore investment in what could be dozens of carbon capture and storage plants, including one in the UAE.

The agreement between Al-Jabar’s Abu Dhabi National Oil Company (ADNOC) and Occidental, which is a quarter owned by Warren Buffett’s Berkshire Hathaway (BRK.A), creates the groundwork to build financing for what Occidental hopes could be as many as 100 plants by 2035.

Carbon capture and storage is fast emerging as the preferred way for fossil fuel companies to comply with the push to fight climate change and mitigate emissions from their product development. By sucking vast amounts of carbon from the air while drilling, they can continue drilling in what is billed as a safe and productive manner. Trouble is, the technology is nascent, and there is no current path to scaling it to the level that would be needed to have a positive impact.

Still, the theory is being pushed, and invested in, by most of the world’s oil majors to some degree, and championed by Al-Jabar, who holds the dual role of president of a climate change event and CEO of the UAE’s national oil company.

While pushing oil companies to invest more in renewable energy is what most climate diplomats prefer, for the moment, carbon capture and storage has, um, captured the attention of both oil executives and Wall Street. For those looking to this year’s COP for progress in actually decarbonizing the world’s economy, it might be worth saving the money (and the flight emissions) on the trip to Dubai in November for next year’s summit. . . .

. . . . They don’t call this time of summer the silly season for nothing. Of all the reasons put forward not to buy an electric car — from range anxiety to flaming batteries to high prices — a British auto industry leader made headlines this week with concerns that they are a national security threat from China.

Ahead of what is expected to be a flood of cheap Chinese EVs in Europe and maybe America as gas-powered cars are phased out in coming years, Jim Saker of the Institute of the Motor Industry said that China could paralyze Britain by remotely turning off hundreds of thousands of vehicles at the same time with spyware. Comparing the threat to the 5G controversy over the tech firm Huawei, Saker and some right-wing politicians said the risk demands any Chinese EV products be scrubbed of any digital data that could carry the spyware.

This type of paranoia is a sign of what could be to come in the U.S. as the China threat grows, and certainly will be an obstacle for China automakers as they try to export the popular BYD models and others over the next few years to compete with Tesla.

But in train-strike plagued Britain this summer, where troubled public transportation has led to massive traffic jams, one wag dismissed the threat of motorways paralyzed with hundreds of thousands of stalled EVs with a simple “how would we know?” . . . .

The most affordable Blazer EV you can buy now costs $56,715. That’s because Chevrolet, owned by GM $GM , has killed off the more affordable Chevy Blazer 1LT. A Chevrolet spokesperson confirmed to Inside EVs this week that the 2LT FWD will be the entry-level option of the Blazer EV. Earlier this week, Chevy released details of the 2024 Blazer EV lineup, including finalized prices and EPA range ratings for the trim levels launching this calendar year. The report notes this is likely a disappointment for EV shoppers. The Blazer EV 1LT would have started at $44,995 — almost $12,000 less than the $56,715 Blazer EV 2LT AWD. But maybe Tesla doesn’t mind The Blazer 1LT would have been a legitimate competitor to the Tesla Model Y with a price almost $3,000 less. Chevrolet did not provide details on why it eliminated the 1LT.

Some of America’s Rust Best cities and towns are experiencing a rebirth, reinventing themselves as “climate refuges” with less risk of extreme weather and more opportunities for growth in renewable energy and sustainability. In a report for Sierra Club Magazine, Jacqueline Kehoe outlines this Rust Belt renaissance, highlighting how legacy cities — with solid infrastructure — are transforming from de-populated, mostly defunct manufacturing hubs into incubators by attracting “artists, start-ups, creatives, lower-income or first-time buyers, and new residents — like so many climate refugees.” One example is Buffalo, N.Y., which calls itself a “climate refuge city” and is promoting solar, hydropower, and even porous, rain-absorbing pavement, the report says.

This article examines the impact of monetary policy on firms’ stock prices across CO₂ emission levels. The authors of Is Monetary Policy Transmission Green? provide a theoretical model in which green firms are less sensitive to MP shocks than brown firms, because they are less exposed to transition risk and provide non-pecuniary utility to investors. They test this prediction by using a panel event-study regression approach on 857 U.S. firms between 2010 and 2019. From the abstract: The results show “robust evidence that firms with high carbon intensity are significantly more affected by policy rate surprises. The sensitivity premium of brown firms remains significant when controlling for classic sources of MP heterogeneity, is persistent, and increases with climate awareness. Our results suggest that the market neutrality principle guiding the implementation of monetary policy could induce a bias toward brown firms.” Authors: Louis Raffestin, University of Bordeaux; Aurélien Leroy, LAREFI, University of Bordeaux; Inessa Benchora, University of Orléans

Words to live by . . . .

“To plant a garden is to believe in tomorrow.” — Audrey Hepburn.

Retirement planning doesn’t have to feel overwhelming. The key is finding expert guidance—and SmartAsset’s simple quiz makes it easier than ever for you to connect with a vetted financial advisor.

Here’s how it works:

Why wait? Start building the retirement you’ve always dreamed of. Click here to get started today!

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

Our expert who first called NVIDIA in 2009 is predicting 2025 will see a historic AI breakthrough.

You can follow him investing $500,000 of his own money on our top AI stocks for free.