Digital payments processor PayPal Holdings Inc. (NASDAQ: PYPL | PYPL Price Prediction) reported fiscal fourth-quarter earnings after U.S. markets closed on Wednesday. PayPal stock traded up about 4% in after-hours trading.

After a good night’s sleep, investors pushed PayPal stock up by around 7% in premarket trading Thursday morning.

Third-quarter results

| Estimate | Actual | Surprise | |

|---|---|---|---|

| Revenue ($B) | 7.39 | 7.40 | 0.1% |

| Adj EPS | 1.23 | 1.30 | 5.7% |

Compared to the third quarter of last year, revenue was up 8.1% and EPS was up 20.4%.

The headline numbers are good, but looking beyond the headlines reveals at least three good reasons to consider adding PayPal stock to a portfolio.

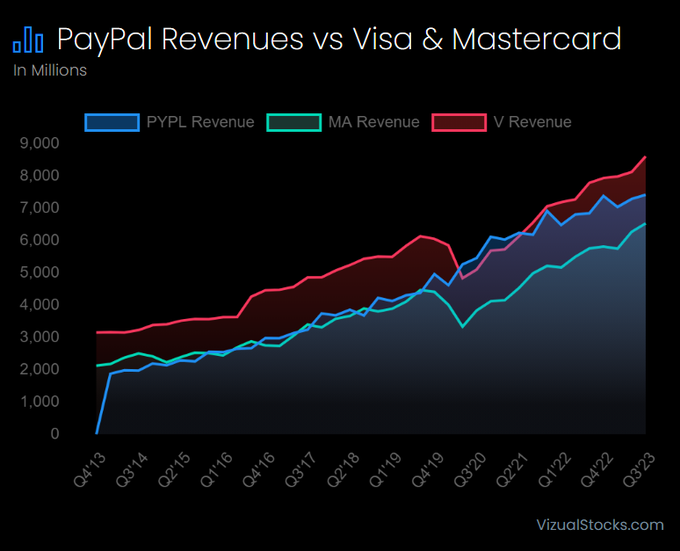

Revenue growth

PayPal’s revenue growth has kept pace with that of the payment industry’s two giants.

But PayPal’s market cap lags, by a lot:

- PayPal market cap: $56.73 billion (at Wednesday’s closing price)

- Mastercard market cap: $354.31 billion

- Visa market cap: $493.59 billion

Over the past 12 months, PayPal revenue totals $28.56 billion to Mastercard’s $9.4 billion and Visa’s $32.65 billion.

Free cash flow yield

- PayPal: 6.4%

- Mastercard: 2.96%

- Visa: 4.1%

Because PayPal does not pay a dividend, the FCF yield depends primarily on share buybacks. When Visa reported quarterly results last week, it announced a new $25 billion buyback program. In fiscal 2022, PayPal repurchased $4.9 billion in stock, Visa repurchased $11.7 billion in stock, and Mastercard bought back $8.75 billion in stock.

Profitability

Put simply, PayPal gets no investor love.