Investing

SoFi Technologies (SOFI) Price Prediction and Forecast 2025-2030 for February 28

Published:

Last Updated:

Shares of SoFi Technologies Inc. (NASDAQ: SOFI) fell −2.8% on Thursday, continuing the past week’s downward trend and dragging down the stock’s one-month performance to −12.70%. SoFi had a strong start to 2025, but on last look it was down 4.7% year to date but still had a one-year gain to 93.2%.

Morgan Stanley recently raised its price target for the stock from $7.50 to $13.00 and called the company “underweight,” and Needham raised its outlook for SoFi from $13.00 to $20.00 while giving it a “buy” rating. The company recently reported strong Q4 earnings but tempered forward guidance. The fintech firm announced EPS of 5 cents, beating analysts’ estimates of 4 cents. But the company’s expectation of annual EPS of 25 cents to 27 cents disappointed investors, who have been selling off the stock since the announcement.

In January, another investment bank — William Blair & Company — initiated coverage of SoFi with a “Buy” rating around the same time SoFi announced that it raised $525 million from a loan program with PGIM Fixed Income. Shares of SOFI have risen more than 99% over the past six months.

SoFi made its public debut on June 1, 2021, through a merger with a special purpose acquisition company (SPAC), Social Capital Hedsophia Holding Corp. V. Before the merger, the company was originally known as Social Finance, which started as a student loan financing firm before expanding into loans, and mortgage products among other finance products. After the SPAC acquisition, SoFi was equipped with substantial capital to enhance its technology stack to better scale its 2020 acquisition of Galileo. The Galileo platform was developed to deploy a wide range of financial services quickly, giving SoFi the tools to take numerous financial products to a mass market.

SoFi IPO’d at $10 per share and quickly jumped 150%, but the stock has seen lackluster performance since. However, investors only care about what happens from this point on, particularly over the next one, three, and five years. Let’s crunch the numbers and give you our best guess on SoFi’s future share price. No one has a crystal ball and even the Wall Street “experts” are often wrong more than they are right in predicting future stock prices. But we give you our revenue and earnings projections as our peer-to-peer valuation.

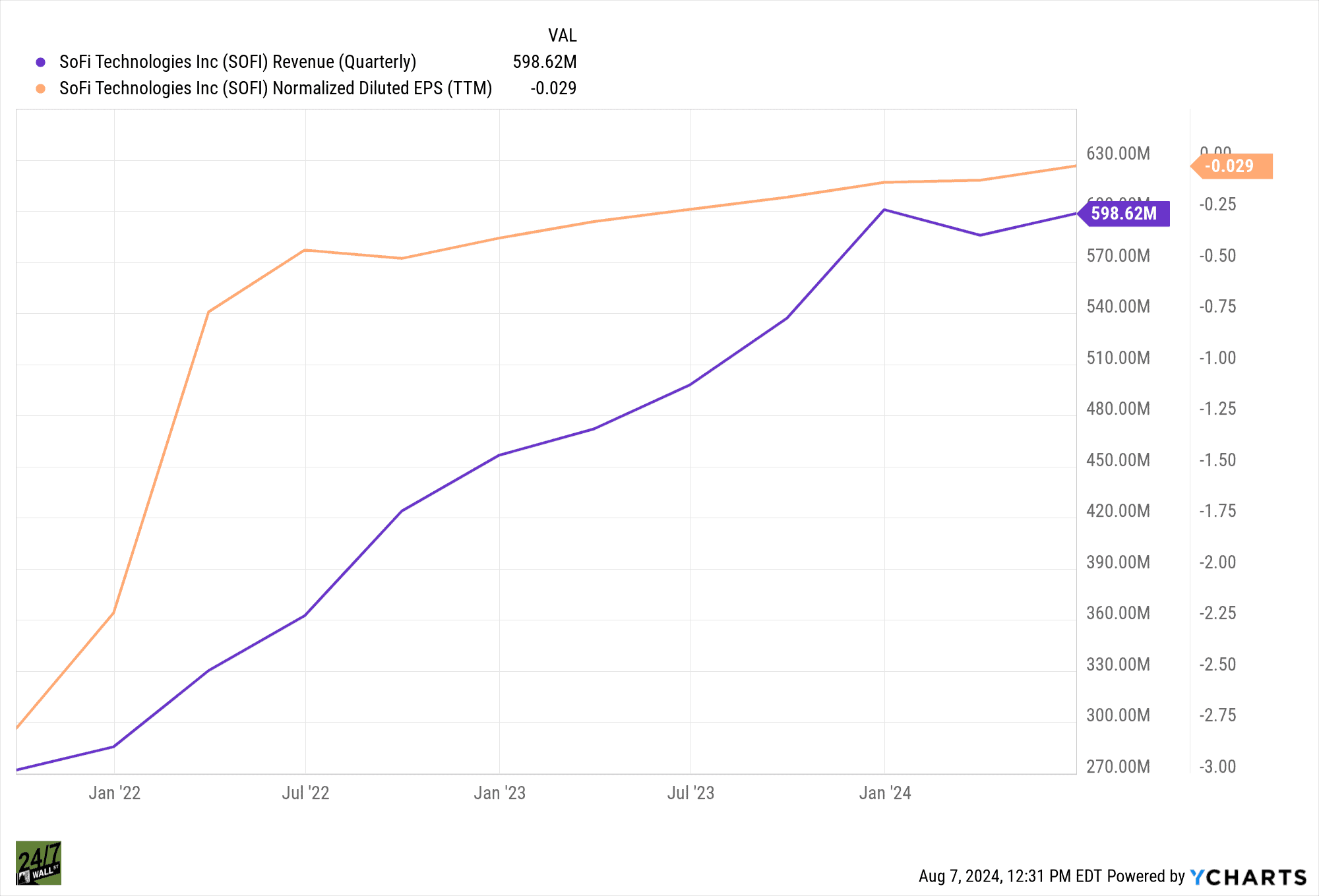

Here’s a table summarizing performance in share price, revenue, and profits (net income) from IPO.

| Year | Share Price | Revenue* | Net Income* |

| 2021 | $12.50 | $977.3 | ($483.9) |

| 2022 | $15.81 | $1,519.2 | ($320.4) |

| 2023 | $4.62 | $2,067.8 | ($300.7) |

| 2024 | $15.40 | $2,343.5 | ($113.3) |

*Revenue and Net Income in millions

In the past four years, SoFi has more than doubled revenue but that top-line growth also carried a jump in total operating costs, particularly the $720 million in sales and marketing expense in 2023. However, the increases in operating costs are money well spent with in-house technology improvements and member-generating marketing spending.

SoFi is close to hitting an inflection point in profitability and has done a stellar job of expanding revenue and improving earnings per share (EPS).

As SoFi’s revenue grows, it becomes more profitable, meaning its costs per customer decrease. This scalability is important because it indicates that as the company grows, it will become even more profitable. Given that the industry is growing and SoFi is outperforming its peers, there’s strong optimism that SoFi’s earnings per share will continue to rise.

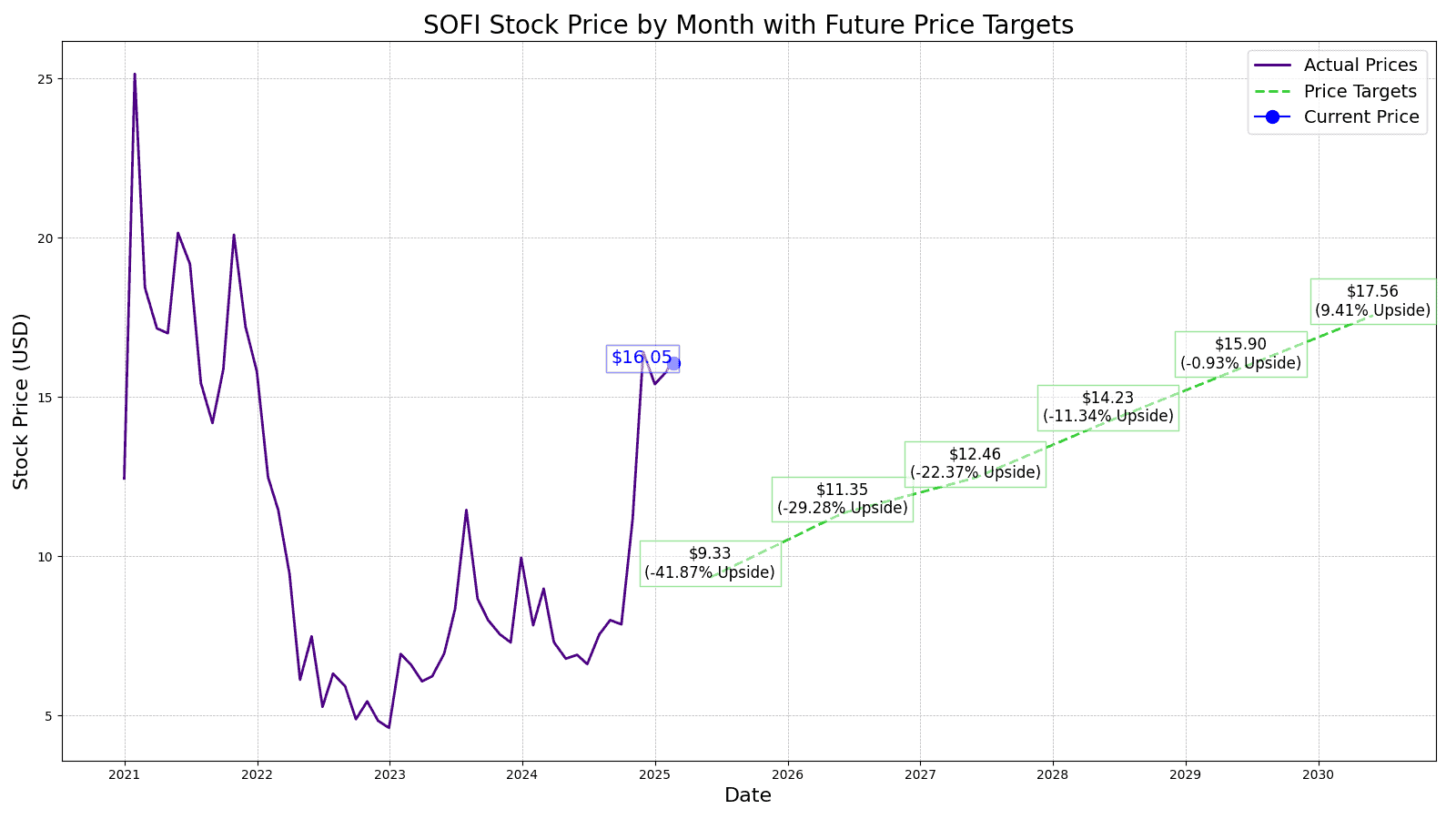

The Wall Street consensus one-year price target for SoFi Technologies is $14.64, which is a −5.91% downside from today’s stock price. Of the 15 analysts covering the stock, the stock is a consensus “Hold” with a 2.88 rating (one being a “Strong Buy” and five a “Strong Sell”).

| Year | Est. Revenue ($B) | Est. Net Income ($B) | Est. EPS Normalized | Price to Sales Multiple | Est. Market Cap ($B) |

| 2025 | $2.84 | $0.32 | $0.21 | 3.5 | $9.94 |

| 2026 | $3.45 | $0.584 | $0.43 | 3.5 | $12.08 |

| 2027 | $3.79 | $0.707 | $0.62 | 3.5 | $13.27 |

| 2028 | $4.33 | $0.902 | $0.83 | 3.5 | $15.16 |

| 2029 | $4.84 | $1.096 | $1.02 | 3.5 | $16.94 |

| 2030 | $5.34 | $1.279 | $1.10 | 3.5 | $18.69 |

24/7 Wall St. compared other fintech/ lenders when deciding on our price-to-sales valuation of 3.5 times for the entire time frame of our analysis. Included in the analysis were Block Inc. (NYSE: XYZ), PayPal Holdings Inc. (NASDAQ: PYPL), Upstart Holdings Inc. (NASDAQ: UPST), LendingClub Corp. (NYSE: LC) and Affirm Holdings Inc. (NASDAQ: AFRM), which gives us a blending valuation of around 3.3x sales.

We estimate SoFi’s stock price to be $17.56 per share with 10% year-over-year revenue growth. Our estimated stock price will be 19.21% higher than the current stock price of $14.73.

| Year | Price Target | Change From Current Price |

| 2025 | $9.33 | −41.87% |

| 2026 | $11.35 | −29.28% |

| 2027 | $12.46 | −22.37% |

| 2028 | $14.23 | −11.34% |

| 2029 | $15.90 | −0.93% |

| 2030 | $17.56 | 9.41% |

Seven Financial Benefits Baby Boomers Got That We’ll Likely Never See Again

After two decades of reviewing financial products I haven’t seen anything like this. Credit card companies are at war, handing out free rewards and benefits to win the best customers.

A good cash back card can be worth thousands of dollars a year in free money, not to mention other perks like travel, insurance, and access to fancy lounges.

Our top pick today pays up to 5% cash back, a $200 bonus on top, and $0 annual fee. Click here to apply before they stop offering rewards this generous.

Flywheel Publishing has partnered with CardRatings for our coverage of credit card products. Flywheel Publishing and CardRatings may receive a commission from card issuers.

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

Our expert who first called NVIDIA in 2009 is predicting 2025 will see a historic AI breakthrough.

You can follow him investing $500,000 of his own money on our top AI stocks for free.