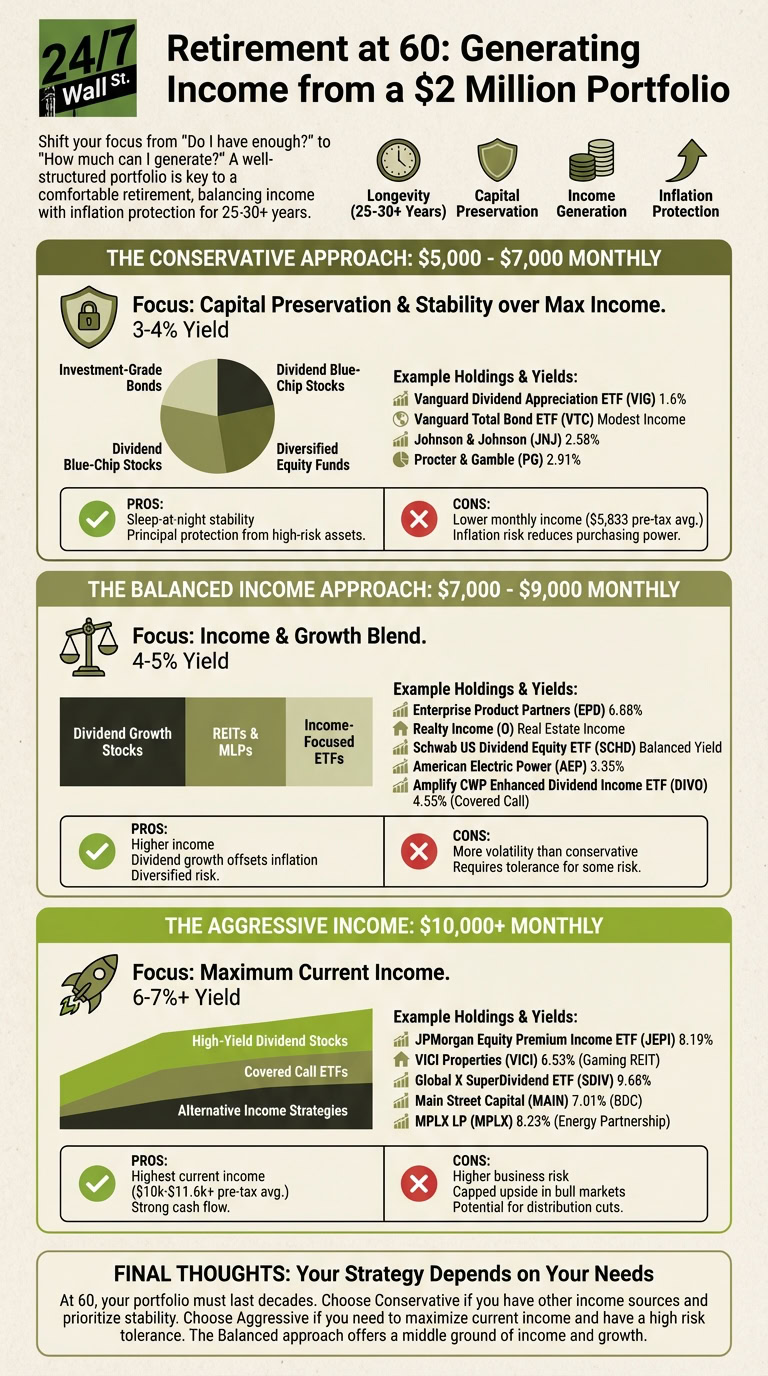

At 60 years old with $2 million saved, you can safely say that you are in a good position that most people will never reach. At this point, the question in your mind should shift from whether you have enough to retire to how much income you can generate from a $2 million portfolio to enjoy a comfortable retirement.

Of course, the answer depends entirely on how you structure your portfolio, as a conservative approach focused mainly on capital preservation might generate only $5,000 to $7,000 monthly. Alternatively, a more aggressive income strategy could push monthly earnings to $10,000 or more as long as you are willing to accept a little more volatility and risk.

Arguably, the most important consideration here is that when you turn 60, you have to think through the idea that you want your money to last for at least 25-30 years. In other words, how you structure your portfolio is more than just how to generate income, it’s also how to maintain purchasing power as costs rise because of inflation.

The Conservative Approach: $5,000 to $7,000 Monthly

For those who want to be more conservative at 60, the focus of any portfolio is going to heavily rely on a strategy that helps with capital appreciation and prioritizes stability over maximum income. This means you will likely be focused on a mix of investment-grade bonds, dividend-paying blue-chip stocks, and a range of diversified equity funds that together generate around 3-4% monthly.

With around $2 million invested at an average 3.5% yield, you’re looking at generating approximately $70,000 annually or $5,833 before taxes. Building this portfolio might include holdings such as Vanguard’s Dividend Appreciation ETF (NYSE:VIG | VIG Price Prediction), yielding 1.6% with consistent dividend growth, combined with the Vanguard Total Bond ETF (NASDAQ:VTC) for modest income. There is also the consideration of adding individual positions in companies like Johnson & Johnson (NYSE:JNJ) at 2.58% or Procter & Gamble (NYSE:PG) at 2.91%, both of which are businesses with decades of dividend increases that won’t cut payouts during a recession.

The advantage of the more conservative approach is what we like to call the sleep-at-night stability, which is basically a level of comfort that your principal isn’t exposed to high-risk assets that could crater during a bear market, so you sleep better. The challenge is that $5,833 before taxes monthly might not feel like a lot, especially if you are used to six-figure earnings. Inflation is also a concern, especially if it runs higher than 4%, which means your purchasing power declines. Ultimately, this strategy is best for anyone with low expenses, paid-off homes, and supplemental income from Social Security or pensions.

The Balanced Income Approach: $7,000 to $9,000 Monthly

A balanced approach targeting 4-5% yield returns would be ideal, combining dividend growth stocks, REITs, and income-focused ETFs without chasing the highest yields available. At $2 million generating 4.5% annually, you’re producing approximately $90,000 per year, $7,500 per month before taxes.

To structure this portfolio, you might look to include positions in Enterprise Product Partners (NYSE:EPD) yielding 6.88% with 28 years of distribution increases, as well as Realty Income (NYSE:O). These real estate income taxes would go along nicely with an allocation to dividend ETFs like the Schwab US Dividend Equity ETF (NYSE:SCHD) that balance yield and liquidity. You might also want to include American Electric Power (NASDAQ:AEP) at a 3.35% yield for utilities exposure or a position in Amplify CWP Enhanced Dividend Income ETF (NYSE:DIVO) at 4.55% for covered call income.

This approach is going to work well for retirees who want higher income but are not comfortable with the volatility that comes with having 8%+ yields. The dividend growth component here will help offset inflationary costs, and the diversification from different sources like REITs, MLPs, and covered calls reduces the risk that any one strategy will fail. The tradeoff is that some of these holdings will be more volatile than your traditional blue chips, but this balanced strategy is arguably the best combination of income, growth, and risk management.

The Aggressive Income: $10,000+ Monthly

If you want to really get aggressive with a $2 million portfolio, you absolutely can, but this means chasing 6-7% yields or higher by focusing on dividend stocks, covered call ETFs, and alternative income strategies. If you want to generate 6% annually, you’re looking at $120,000 per year or $10,000 per month, before taxes. Going for 7% yields, and you’re looking at $11,667 monthly, again, before taxes.

To build this kind of aggressive portfolio, you’re going to want to look at large positions in holdings like the JPMorgan Equity Premium Income ETF (NYSE:JEPI) at 8.19% for monthly covered call income. You can also invest in VICI Properties (NYSE:VICI) at 6.53% for gaming REIT exposure, and the Global X SuperDividend ETF (NYSE:SDIV) at 9.68% for diversified international high-yield exposure. If you want to get more aggressive, add in Main Street Capital (NYSE:MAIN) at 7.01% for Business Development Companies exposure or an energy partnership like MPLX (NYSE:MPLX) at 8.23%.

Unsurprisingly, the risk with this more aggressive approach is that high yields equate to higher business risk, limited growth potential, or unsustainable payout ratios. Covered call strategies are going to cap your upside during bull markets, and REITs and MLPs can cut distributions if business weakens. However, retirees at 60 who want to prioritize current income over long-term growth and have a strong tolerance for risk will enjoy the $10,000 monthly upside with this strategy.

Ultimately, at 60 years old, you’re young enough to need a portfolio to last at least 30 years, or more, which means the right strategy is going to depend on your situation. If you have a pension that covers most expenses and just need supplemental income, go with the conservative approach, but if you have high expenses and no other income sources until Social Security, going aggressive might be the right path.