Providing full-stack infrastructure for the artificial intelligence industry, IonQ (NYSE:IONQ | IONQ Price Prediction) has delivered revenue growth that almost no one predicted at this pace, yet the stock sits 21% below where it started 2026, and that gap between business performance and price is what retail investors are debating right now.

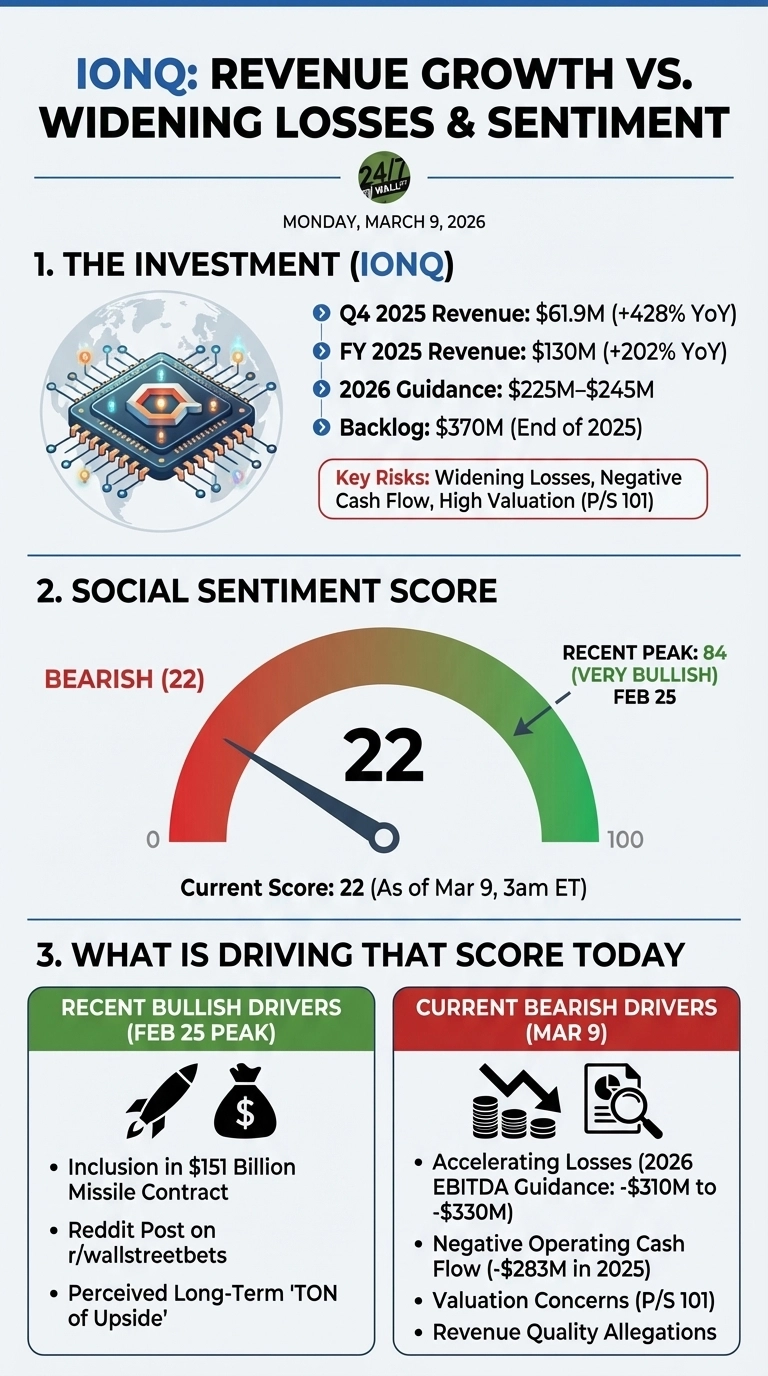

Ultimately, the Q4 2025 numbers are hard to dismiss as quarterly revenue hit $61.9 million, a 429% year-over-year jump that beat consensus estimates by 53.7%. Full-year 2025 revenue reached $130 million, tripling 2024 and making IonQ the first public quantum company to exceed $100 million in annual GAAP revenue. Management is guiding for $225 million to $245 million in 2026 revenue, with CEO Niccolo de Masi calling it a “strategic and financial inflection point.”

The problem is what sits on the other side of that growth. The 2026 Adjusted EBITDA loss is expected to widen to between -$310 million and -$330 million. Operating cash flow in 2025 was -$283 million. The stock trades at a price-to-sales ratio of around 100-120, a valuation that prices in breakthroughs still years away.

Reddit Is Split, and the Data Shows It

Social sentiment on IonQ has whipsawed over the past two weeks. A post on r/wallstreetbets on February 25 drove sentiment to 84 (Very Bullish) after a user flagged IonQ’s inclusion in a $151 billion missile contract. That spike faded fast. By March 8-9, sentiment in r/stocks had fallen back to 22-28 (Bearish), with comment-to-upvote ratios suggesting genuine debate rather than consensus.

IONQ SECURES PLACE IN MISSLE CONTACT

by u/therealJcrusin in wallstreetbets

The post’s author, u/therealJcrusin, wrote: “Unfortunately, most people don’t understand Quantum and that makes the company an easy target for short sellers… I believe there is a TON of upside to investing now and way, way more in the long term (5 to 10 years).”

The bearish case in r/stocks centers on three concerns:

- Losses are accelerating, not shrinking: the 2026 EBITDA loss guidance of -$310M to -$330M is wider than the -$186.75M posted in 2025

- The 2026 EBITDA loss guidance of -$310M to -$330M is wider than the -$186.75M posted in 2025, meaning losses are expanding even as revenue scales.

- Per prior coverage, Wolfpack Research has alleged revenue quality concerns tied to government contract dependency, a claim IonQ disputes

The Backlog Is Real, but the Burn Rate Is the Test

As of the end of 2025, remaining performance obligations stood at $370 million, nearly five times the $77 million figure at the end of 2024, and that backlog is not speculative. The QuantumBasel contract alone exceeds $60 million over four years, and IonQ holds $3.3 billion in cash and investments to fund the roadmap. Analysts carry a consensus price target of $74 with 7 Buy ratings and zero Sells.

The pending SkyWater Technology acquisition, expected to close in Q2 or Q3 2026, is the clearest near-term test of IonQ’s execution credibility. A clean close would strengthen its position with government buyers who increasingly require domestic manufacturing capability. A stumble would expose how little room the current valuation leaves for operational setbacks.