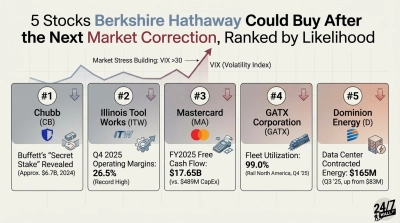

Chubb (NYSE:CB | CB Price Prediction) trades at $329.99 as of writing, and our proprietary model points to meaningful upside. The 24/7 Wall St. price target for Chubb is $363.54, implying 10.17% upside over the next 12 months. Our model assigns a 90% confidence level to this target.

| Metric | Value |

|---|---|

| Current Price | $329.99 |

| 24/7 Wall St. Price Target | $363.54 |

| Upside | 10.17% |

| Model Confidence | 90% |

| Confidence Level | 90% |

Chubb is the world’s largest publicly traded property and casualty insurer. The stock has gained 6.04% year-to-date and 17.05% over the past year, yet valuation remains undemanding.

Record Results Fuel Rally

Chubb has climbed steadily since bottoming near $274 in mid-2025. The stock now sits just 1% below its 52-week high of $344.65, recovering from a 52-week low of $261.59.

Q4 2025 delivered core operating EPS of $7.52, beating consensus of $6.78 by 10.91%. The P&C combined ratio hit a record low of 81.2%, down from 85.7% a year earlier. Full-year net income reached $10.31 billion, up 11.19% year over year, on operating EPS of $24.79. CEO Evan Greenberg called it the best year in the company’s history.

Bull Case: Three Compounding Drivers

The bull case centers on record underwriting margins, accelerating investment income, and aggressive capital return. CEO Greenberg guided for “double-digit growth in EPS and tangible book value” in 2026, with January renewals described as “more favorable than anticipated.”

Life insurance premiums grew 16.9% in Q4, overseas consumer lines expanded 18.7%, and personal auto surged 28.8%. Chubb returned $4.91 billion to shareholders in Q4 alone, buying back shares at an average of $282.57 while management stated the stock traded “well below intrinsic value.”

Analysts set a consensus target of $341.39, with 10 buy-rated analysts on the stock. Our bull scenario reaches $380.04 within 12 months if premium growth accelerates and catastrophe losses normalize.

Risks to Monitor

Full-year 2025 catastrophe losses totaled $2.92 billion, up from $2.39 billion in the prior year. Q1 2025 alone absorbed $1.47 billion from California wildfires. A repeat could pressure results. Commercial insurance markets are growing more competitive, with large-account property rates declining.

Revenue declined 5.59% for the full year. CEO Greenberg acknowledged that “odds of recession have risen substantially.”. Our bear scenario lands at $322.55, roughly flat to today.

The revenue decline reflects foreign currency headwinds and portfolio mix shifts rather than deteriorating core demand. Underlying premium growth in constant dollars remains positive, and the record combined ratio of 81.2% suggests peak underwriting efficiency.

Verdict: A Steady Compounder With Upside

The 24/7 Wall St. price target of $363.54 reflects a high-quality insurer trading at a reasonable 13x trailing earnings with a clear path to double-digit EPS growth in 2026. Our 90% confidence level is among the highest we assign.

The record combined ratio, accelerating investment income at a 5.2% fixed-income yield, and management’s explicit double-digit growth guidance support the bull case. Revisit if catastrophe losses spike materially above the $3 billion annual range or if the commercial market softens faster than expected.

Price Targets 2026-2030

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $363.54 |

| 2027 | $395.00 |

| 2028 | $420.00 |

| 2029 | $448.00 |

| 2030 | $470.90 |

These projections assume mid-single-digit premium growth and steady margin expansion. Significant upside or downside could result from major catastrophe cycles, interest rate shifts, or accelerating growth in Asian and Latin American life insurance markets.