Personal Finance

This is how much you should have saved by 50 — are you on track?

Published:

If you are 50, you’ve seen firsthand throughout your life how volatile the market can be, how prices of goods can change through the decades, and how quickly the job market can fluctuate. The good news about being 50 and reviewing your retirement savings is that you can have a more accurate estimation of how much you will need for retirement. Edward Jones came out with a benchmark of how much you should have saved based on income and age.

According to Edward Jones, if you are 50 and are currently making up to $50,000, you should have $250,000–$300,000. If you make between $50,000–$100,000, you should have $500,000–$600,000 saved for retirement. If you make $100,000-$150,000, you should have $920,000–$1,090,000 saved. And if you make $150,000–$200,000, you should have $1,430,000–$1,690,000 saved for retirement.

| Current Annual Income | Recommended Savings at Age 50 |

|---|---|

| Up to $50,000 | $250,000–$300,000 |

| $50,000–$100,000 | $500,000–$600,000 |

| $100,000–$150,000 | $920,000–$1,090,000 |

| $150,000–$200,000 | $1,430,000–$1,690,000 |

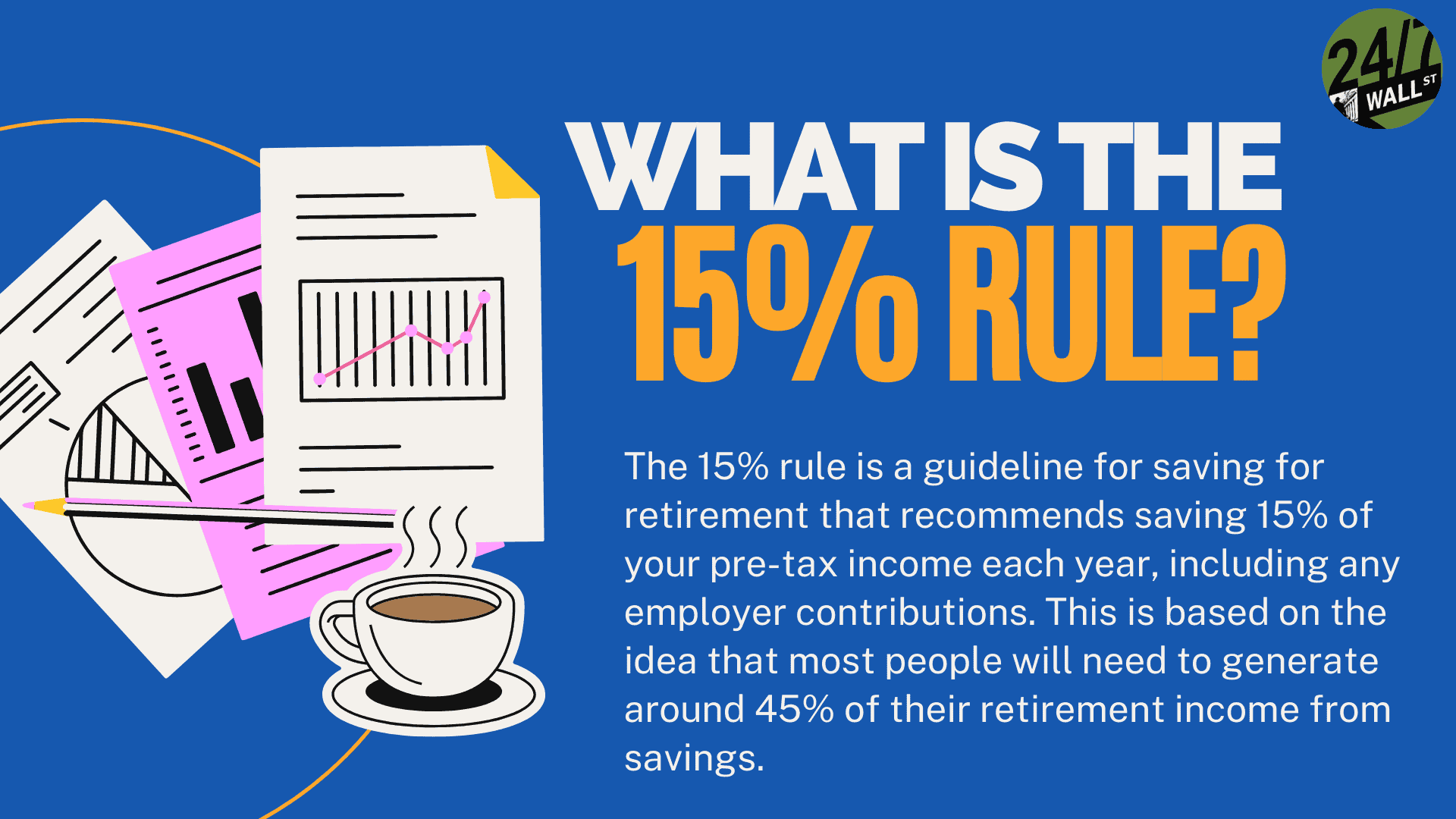

These numbers are based on the 15% rule, meaning that 15% of your gross income should be enough to sustain you through retirement. It also assumes that you want to maintain your current lifestyle and current level of monthly spending, you are planning on retiring at the age of 65, and you will live until you are the age of 92.

Are you behind or ahead? If you are behind these benchmark numbers, there are things that you can do to catch up.

Reevaluating your end goal has a large benefit if you are 50, because retirement is sooner, and you have a more realistic goal that you need to save. You can adjust the percentage you are saving, and know what lifestyle expense cuts to make if you need to increase your percentage.

Hiring a financial planner may seem like an unnecessary expense, but they have a wealth of knowledge about retirement savings, social security payments, the stock market, IRAs, etc. They might be able to offer you options that you don’t realize you have. With all the different types of retirement savings accounts, you simply just might not know how to navigate the retirement landscape.

A financial planner can also help you evaluate your monthly spending patterns and see where you can cut back, establish a better budget, etc.

Delaying retirement as long as you can after age 62 up until age 70 will get you a larger monthly payout the longer you delay it. Not only will your monthly payment increase by 8% per year you delay, but your COLA (cost-of-living adjustment) increases will be larger as well. This also means that you will have a guaranteed larger lifetime stream of income. You would want this because you won’t leave that money on the table if you can live off of your savings until you are 70.

Some job benefits include a “401(k) Match Plan.” That means that your employer will match a certain percentage of what you are contributing to your retirement savings plan. So, if your employer’s plan is 20%, pay as much as you can so you can get that free 20% added to your account. If you don’t take advantage of that, you are missing out on free money.

Usually, you can only contribute a certain amount of money per year to your retirement savings account. As soon as the calendar year of your 50th birthday comes around, you can make catch-up payments especially if you weren’t able to save as much as you needed to before turning 50. So, start saving where you are, and contribute what you can.

If you are ahead of the game, there are some things you can do to maximize your retirement lifestyle.

If you are easily meeting your savings goal and reaching the limit of what you are allowed to put into your 401(k), you can open another retirement savings account, particularly an IRA (Individual Retirement Account). There are two different types, a Roth IRA and a traditional IRA. The kind you should utilize depends on your workplace circumstances. Either way, it allows you to contribute more money to your savings and opens up more options for investing.

This article is a generalized overview of retirement savings plan benchmarks. If you really want to evaluate, overhaul, or gain comfort over your finances, consulting a financial planner is going to be your safest option. Your financial planner’s job is to help you plan for retirement, analyze your finances, give investment advice, and do estate planning. All of those tasks can be daunting for lay folk. Having a guide to help you maximize your money is always a good idea.

Are you ready for retirement? Planning for retirement can be overwhelming, that’s why it could be a good idea to speak to a fiduciary financial advisor about your goals today.

Start by taking this retirement quiz right here from SmartAsset that will match you with up to 3 financial advisors that serve your area and beyond in 5 minutes. Smart Asset is now matching over 50,000 people a month.

Click here now to get started.

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.