Personal Finance

We're in our 40s with nearly $10 million - what type of financial advisor should we use to avoid getting ripped off?

Published:

Last Updated:

This post is coming from the subreddit r/fatFire (Retire with a fat stash). The title is: “At $10M NW, should we use a fee-only financial advisor, a robo-advisor, or manage ourselves? How did you decide?” I am definitely not a professional financial advisor, so I decided to take a look. The original poster (OP) shares that he and his wife live in a high-cost-of-living area, earn about $1 million annually, and break even after taxes. They have $10 million in liquid assets, $4 million in real estate, and some private equity investments (value not mentioned). He states that they are financially literate, stick to a budget, and plan tightly for retirement.

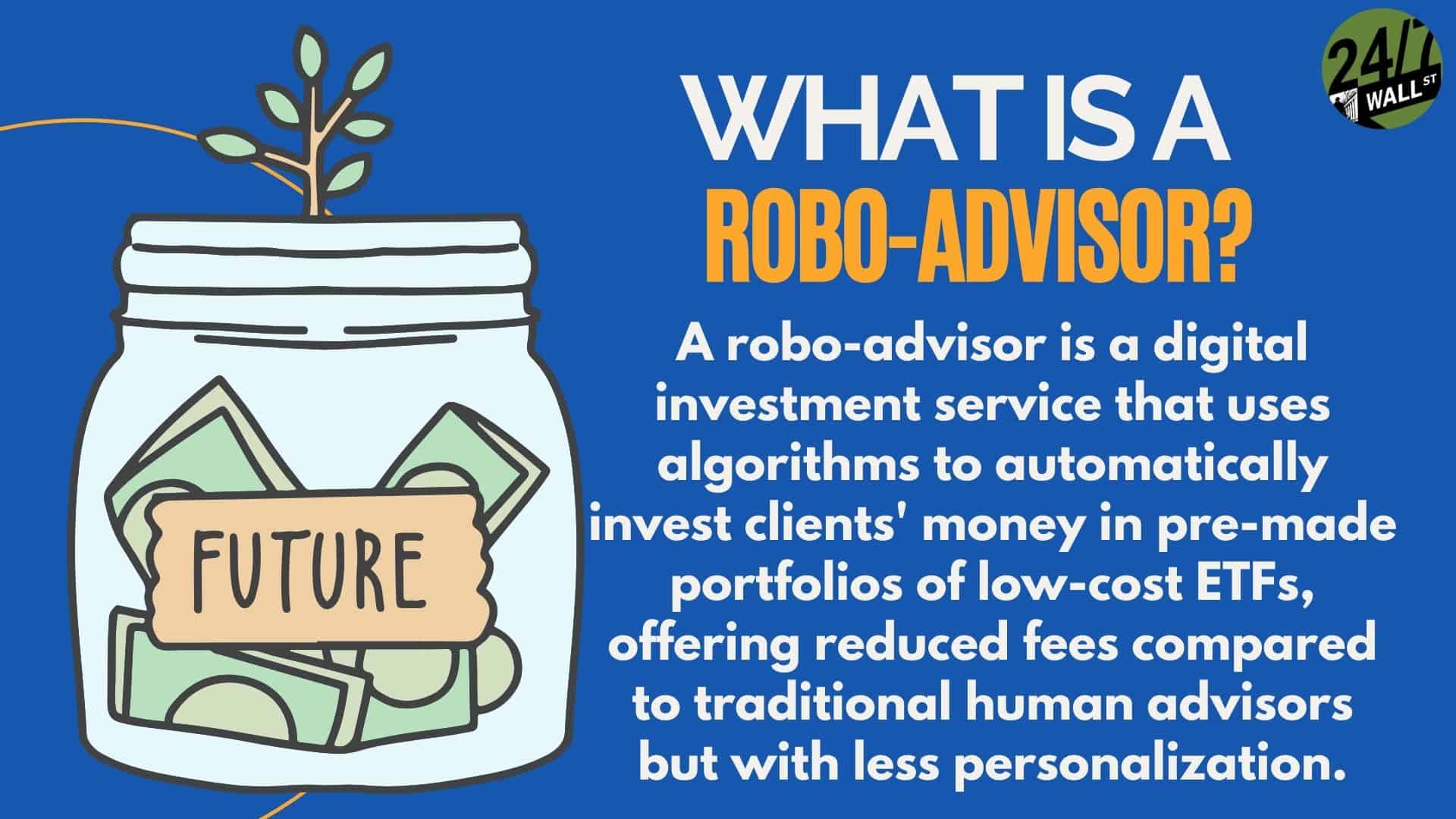

A robo-advisor is a brokerage account that automates the investment process and all services are almost completely digital. Humans are still involved, but only as much as necessary. Robo-advisors can be appealing because they often charge lower fees. After all, your money gets invested in template-like portfolios that are made up of low-fee exchange-traded funds, and aren’t customized or personalized specifically to your unique lifestyle or financial goals.

OP is wondering how to manage their financial advising. Three years prior, they started using a fee-only fiduciary financial advisor, and they are fine with the experience so far. Their advisor manages administration, tax loss harvesting, and rebalancing. Although the financial advisor is responsible and pleasant, OP was expecting more value out of what he is paying for. They pay $50,000 for the first $10 million and 0.1% annually on amounts above that. OP feels that his planning models are more rigorous, he still has to do copious amounts of research when making a decision, and he still has to pay other professionals on top of the fees for things like estate planning, mortgage loans, and taxes.

OP worries that he is losing out or harming his future retirement fund by sticking with this financial advisor. He asks commenters if he should work with a robo-advisor and an hourly fee-only advisor for any questions he couldn’t find answers to himself.

Out of the opinions in the commenters, there seem to be a few common answers. The first is a few people tell OP that his only real goal should just be to “not f*ck up.” One commenter points out that he has enough money to live the rest of his life on, and the investment strategy should just be to earn more, and if not, that’s OK. Just don’t lose anything.

Another consensus, as a commenter points out, is that at a net worth of $10 million, the “value” of this decision isn’t that important. The most important thing is the value of his time. Does OP enjoy doing all of this research and side-managing to double-check his financial advisor? Or, would OP rather just let go of most of the control and get another hobby? OP does admit that he enjoys building spreadsheet models and being financially literate. He feels that $10 million is an amount he is comfortable managing on his own. Many commenters say that OP is more equipped to handle his own money than anyone else, and just occasionally having someone “check his work,” would be enough for an outside party to do.

A lot of commenters say that having a competent third party available to bounce ideas off of that you trust, understands your family situation, your financial goal, and risk tolerances. Most people with this opinion have a few hourly-fee advisors who they run the same decisions by and compare responses.

Most people on this thread agree that all of the advisor options are beneficial in their own ways, but that OP would probably be happier just managing his own money. A frequent caution mentioned is that whatever the OP chooses, his spouse needs to understand the financial plans, and decisions, and understand what’s going on in case one of them passes away. Without outside management, it’s important to be on the same page as your life partner.

Retirement planning doesn’t have to feel overwhelming. The key is finding expert guidance—and SmartAsset’s simple quiz makes it easier than ever for you to connect with a vetted financial advisor.

Here’s how it works:

Why wait? Start building the retirement you’ve always dreamed of. Click here to get started today!

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

Our expert who first called NVIDIA in 2009 is predicting 2025 will see a historic AI breakthrough.

You can follow him investing $500,000 of his own money on our top AI stocks for free.