Personal Finance

I'm 54 in great health and have $3 million saved for retirement - should I still consider long-term care insurance?

Published:

Last Updated:

There are some pretty big decisions that people will need to make before they finally wind down and retire. Indeed, for many, such decisions can be stressful. Make the wrong move, and one could really pay for it, either with their lifestyle, health, or financial well-being.

In any case, the whole retirement planning process does not need to be so stressful as long as you’ve got a good support network and a financial advisor (or wealth planner) who’s on your side. Indeed, not having such a financial-planning professional in your corner as you gear up for retirement can be as ill-advised as not having a coach in your corner in the middle of a 12-round boxing match.

Sure, you can make things work if you have talent and the conditioning. However, you’ll probably get markedly better results with someone on your end before, during, and hopefully not after your expected retirement date.

A rather wealthy soon-to-be retiree, 54 at the time of the posting made close to three years ago, took to Reddit in search of advice about whether they should get long-term care insurance.

With around $3 million saved up for retirement, the poster has quite the sizeable nest egg and could, in theory, retire anytime they’d like. They were shooting to exit their work at the age of 58, however, likely around four years before they’d be eligible to collect social security benefits.

Given the hefty sum saved up in the poster’s career and the likelihood they’ve had a lengthy career, I’d argue their social security payments could have the potential to be greater than the average, even with the early retirement considered.

Undoubtedly, $3 million is a lot of money that could support a chubby FIRE (Financial Independence, Retire Early) lifestyle that entails a pretty high standard of living unless, of course, one is living in a downtown New York City penthouse!

Either way, I’m going to assume that the poster is closer to the average. And that they have no plans to upgrade their lifestyle from Chubby FIRE to Fat FIRE (higher living expenses) in the midst of their golden years.

Given the Reddit post was close to three years ago, the poster is probably a year or less away from their expected retirement date. And they probably have a bit more than $3 million saved up, given the impressive market gains since the time of the posting.

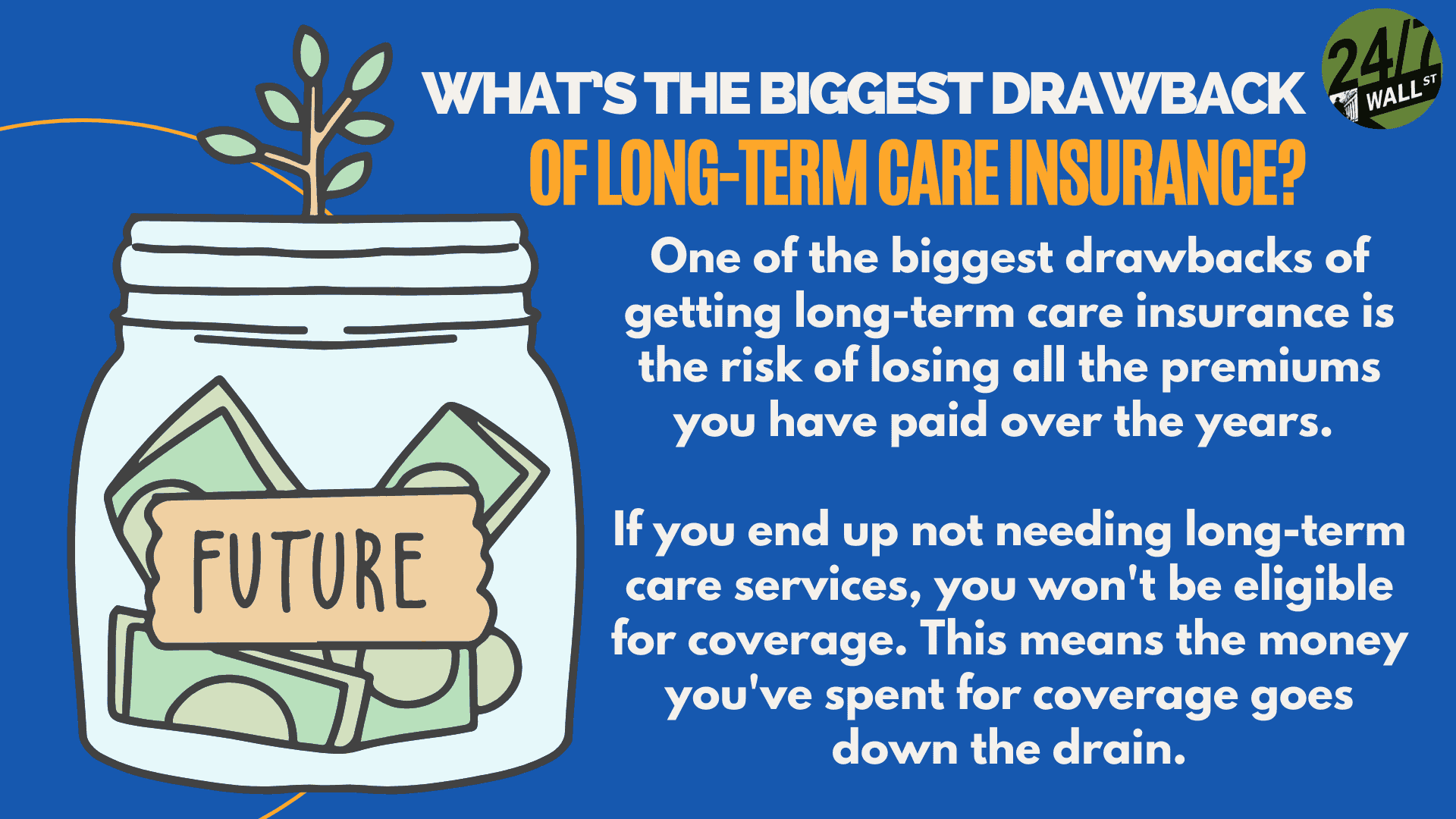

Either way, the big question is whether it’s a good idea to pick up life insurance in one’s mid-50s, even with a fat sum that I believe is more than enough to cover the nursing home bills as they come along.

Long-term care insurance premiums can be rather hefty. But if you’re keen on getting a policy, it’s far better to get one in your 50s than your 70s, especially if you have a family history of ailments that require the need for care and you don’t want to be a burden to your children at some point down the road.

At the end of the day, you have information that should give you a good gauge of the odds of whether you’ll be in need of hefty costs later in life. Nursing homes are not cheap. In fact, they can cost north of $100,000 in some pricier localities. Further, the peace of mind by having a policy in place sooner rather than later can give you peace of mind as you enjoy the early days of your retirement.

Indeed, nasty surprises can happen. And it’s better to have such an expensive obligation covered so that you can truly enjoy the retirement time you’ve worked so hard for.

If you’re worried about medical conditions (let’s say Alzheimer’s or Parkinsons) hitting you later in life or if you’ve got a family history that puts you at greater risk, getting a care insurance plan earlier can save you a ton of cash. Just because you’ve got enough savings to meet the high costs of care does not mean you shouldn’t take the moves to best protect your nest egg.

Though I’d advise such a poster to consult with a wealth planner before meeting with an insurance representative, I do think that the poster sounds rather concerned about long-term care obligations crushing the $3 million nest egg.

If one is to purchase care insurance, it’s better to do so sooner rather than later. If you’re relatively young and in great health today, you’ll get a great value on insurance.

Even if you’re in a similar financial position and unsure about the exact amount of coverage needed, it’s always wise to get a quote and explore your options.

A quick, no-obligation quote can provide valuable insight into what’s available and what might best suit your family’s needs. With affordable rates and customizable policies, life insurance is a simple step you can take today to help secure peace of mind for your loved ones tomorrow.

Click here to learn how you can get a quote in just a few minutes.

Start by taking a quick retirement quiz from SmartAsset that will match you with up to 3 financial advisors that serve your area and beyond in 5 minutes, or less.

Each advisor has been vetted by SmartAsset and is held to a fiduciary standard to act in your best interests.

Here’s how it works:

1. Answer SmartAsset advisor match quiz

2. Review your pre-screened matches at your leisure. Check out the advisors’ profiles.

3. Speak with advisors at no cost to you. Have an introductory call on the phone or introduction in person and choose whom to work with in the future

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

Our expert who first called NVIDIA in 2009 is predicting 2025 will see a historic AI breakthrough.

You can follow him investing $500,000 of his own money on our top AI stocks for free.