Personal Finance

"I have had a high stress job all my life and I want to get healthy": Couple with $2.7 million saved wonders if they can finally pull back

Published:

Last Updated:

24/7 Wall St. Key Points:

In the world of Reddit finance, the question “Can I retire next year?” seems to pop up all the time. However, one Reddit post I recently encountered highlighted an unusual part of retirement: what do you do afterward?

The couple posting has a solid financial foundation, with over $2.7 million in their portfolio. That said, they’re contemplating what retirement will look like for them.

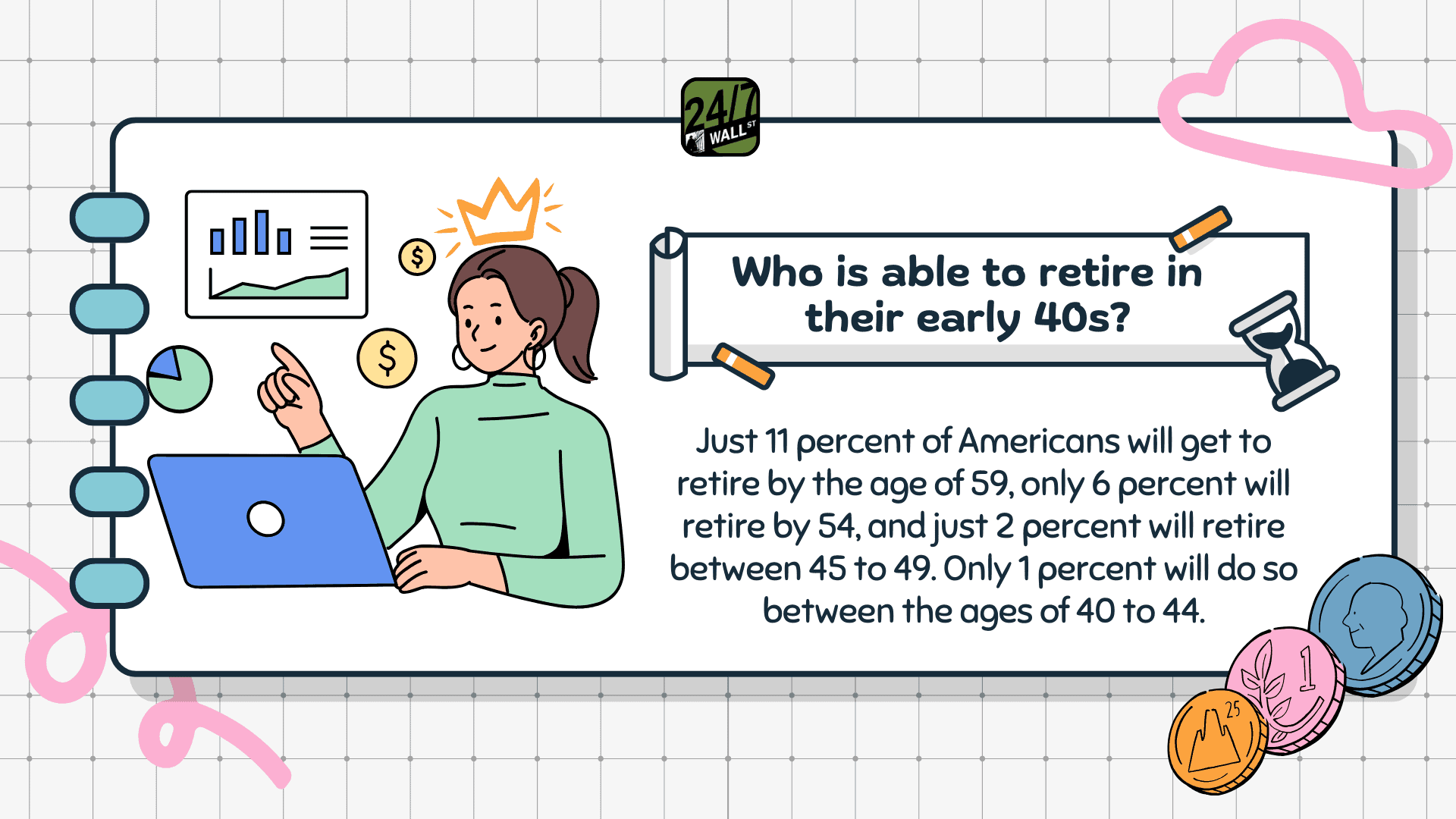

The couple consists of a 42-year-old husband and a 40-year-old wife. They live in a high-cost-of-living area and have significant assets, including a home valued at $1.3 million and a mortgage under 3%. Their current expenses total about $120,000 annually, supported by a high household income that fluctuates between $350,000 and $450,000.

While their math works out to retire, they’re working out what life would look like afterward – a problem that’s very common among retirees.

Retiring is just as mental as it is financial. Below, I’ll look at how to navigate the complex world of after retirement. Remember, this is just my opinion and not financial advice.

The key to retiring confidently lies partially in the finances, but it also relies heavily on the mental and emotional aspects of retirement:

Many people take their purpose from their jobs. The poster expresses a desire to retire and focus on health and family. After years in a high-stress job, he recognizes the importance of personal fulfillment over accumulating additional wealth.

On the other hand, his wife enjoys her job and plans to work until she can secure a pension. This difference in motivation can lead to tension, especially if the wife feels annoyed by her husband’s early retirement.

There is a mismatch of goals here.

Part of retiring early is retirement. With $1.7 million pretax and $1 million post-tax, this poster has a solid financial cushion. However, the husband is concerned about the Sequence of Returns Risk and whether their lifestyle can be sustained long-term. His retirement income will drop down to $85,000 per year, making this even more worrisome.

There are many future costs he needs to anticipate, too. For instance, he needs to send his children to college in a decade or so.

While the finances do work out on paper, that doesn’t mean they work out in the real world.

One place where this couple may really benefit is lifestyle adjustments. They should consider whether to pay off the mortgage to reduce yearly expenses. However, in some cases, it makes more sense to invest the income than it does to pay off your mortgage.

The couple may also want to consider the idea of “coastfire,” where they work in lower-stress roles with more time off. These flexible jobs can help them “retire” without fully retiring.

The couple has anticipated changes in their financial situation, such as the potential for inheritance and the pension that the wife will receive in 20 years. Just about everyone who retires early will experience some changes over their retirement that may affect their expenses. These changes need to be accounted for.

Other essentials like health and caregiving need to be considered. Unexpected expenses and caregiving for parents can take big chunks out of your retirement fund.

Planning for retirement isn’t just about math. It’s about the mental and relationship aspects of retirement, too.

It’s important to create a comprehensive approach to life after work with your spouse and whoever else is affected by your decision. Having honest discussions is how you work out a plan that contributes to everyone’s success and goals.

Working with a financial advisor is also highly recommended. Even if it all works out on paper now, it’s important to consider future income streams and expenses on top of taxes. It’s important to avoid common tax mistakes.

Retirement planning doesn’t have to feel overwhelming. The key is finding expert guidance—and SmartAsset’s simple quiz makes it easier than ever for you to connect with a vetted financial advisor.

Here’s how it works:

Why wait? Start building the retirement you’ve always dreamed of. Click here to get started today!

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

Our expert who first called NVIDIA in 2009 is predicting 2025 will see a historic AI breakthrough.

You can follow him investing $500,000 of his own money on our top AI stocks for free.