Personal Finance

The $500,000 Retirement Blueprint for 60-Year-Olds

Published:

Last Updated:

Key Points from 24/7:

According to research from Smart Asset, the median savings for someone in their 60s in $185,000. If you’ve made it here and have $500,000 or more, take a moment and appreciate what an achievement that is.

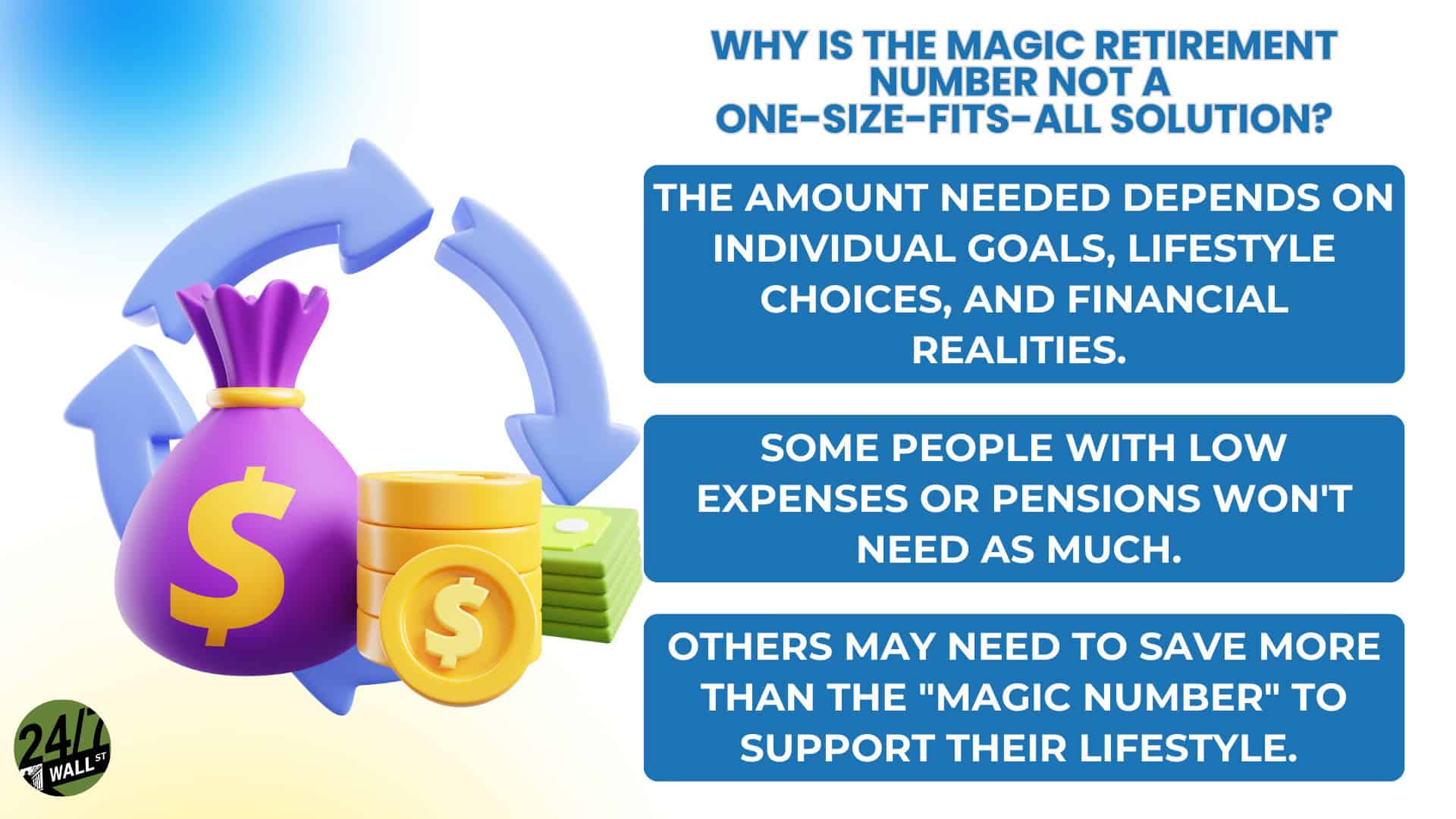

But many Americans just like you have made it here without a game plan for what happens next. You might be wondering whether that’s enough to actually retire, and if not how much more you’ll need to save. And once you hit ‘the magic number’, how do you responsibly manage what you’ve earned to make sure it lasts?

You need a retirement blueprint, and it doesn’t need to be complicated.

Here is the quick four-step formula to making that $500,000 portfolio last.

Before you retire you must understand what your annual income needs are. This number is perhaps more important than your nest egg itself, because it tells you how much you need to have saved, and how long it will last.

On average, retirees need 70-80% of their pre-retirement income to maintain their lifestyle. So if you’re used to living on $100,000 a year, you should budget for $75,000 – $80,000 a year in withdrawals from your nest egg. Better to be a little conservative here and err on the high end.

And consider that you’ll need this income for anywhere from 20-30 years. It’s not as straight forward as just multiplying the annual income by 20 or 30 though, because you’ll have to account for assumed investment returns. For this, it’s best to speak with an advisor.

While a $500,000 nest egg is meaningful, it may not be sufficient for a rich retirement. The good news is, supplementing this with additional income from Social Security (or other sources), can dramatically extend the life of your savings.

While you can start receiving Social Security payments as early as 62 years old, waiting a few years (even pushing as far as 70) often significantly increases your monthly payments. If you have the ability to earn extra income from rental properties, side gigs, or other part time work this can also extend your runway for that $500k portfolio.

Speak with an advisor to determine whether 62, 65, or 70 is the best age for you to claim Social Security in retirement.

How you spend your money is as important as how you save it. ‘The 4% rule’ has gained popularity in recent decades as a reliable rule of thumb. It states that, on average, you should be able to spend 4% of your portfolio per year and have the money last through retirement.

For a $500,000 portfolio that means spending $20,000 per year. That certainly doesn’t seem like much, but when augmenting with income from step 2 above, that $20,000 can more than double to as much as $48,000 per year. Combined with some additional income from a part time job and that number can grow to $60,000 or more per year without too much effort.

We recommend a flexible 3-5% withdrawal rate per year, drawing down less when your portfolio is down in value, and more after a good year.

The most important step in a $500,000 retirement blueprint is to put all of these factors on the table next to each other and make decisions with everything considered. For this, speaking with a financial advisor is the best next step.

An advisor can tell you if you’re on track, or behind on your savings. They will give you the guidance on how much more to save, and help you calculate ‘the magic number’. They’ll answer important questions like determining the best age to withdraw social security, because everyone’s situation is unique.

You can speak to an advisor today and get started, totally free. Simply click here now to get started.

Retirement can be daunting, but it doesn’t need to be.

Imagine having an expert in your corner to help you with your financial goals. Someone to help you determine if you’re ahead, behind, or right on track. With SmartAsset, that’s not just a dream—it’s reality. This free tool connects you with pre-screened financial advisors who work in your best interests. It’s quick, it’s easy, so take the leap today and start planning smarter!

Don’t waste another minute; get started right here and help your retirement dreams become a retirement reality.

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

Our expert who first called NVIDIA in 2009 is predicting 2025 will see a historic AI breakthrough.

You can follow him investing $500,000 of his own money on our top AI stocks for free.