Personal Finance

My wife wants to leave our $5 million house for our kids to inherit - but I think it might be better to just sell it now

Published:

24/7 Wall St. Key Takeaways”:

In a recent Reddit post I came across, a 48-year-old was seeking advice on managing his $16 million net worth. I found this post interesting because he was particularly concerned about the $5.5 million tied up in his primary residence. As a father of two, living in a very high cost of living (VHCOL) area, he’s grappling with how to approach long-term housing decisions.

This situation is much more common than you might think. Many high-net-worth individuals’ wealth is tied up in housing and is non-liquid.

Let’s explore some of his key concerns and look at some strategies I recommend considering. Remember, this is just my recommendation, not financial advice.

With a net worth of $16 million, including $8.2 million in liquid assets, $2.2 million in retirement accounts, $0.5 million in 529 college savings plans, and $5.5 million in his home, one-third of the poster’s wealth is tied up in his primary residence.

The main question he’s concerned about is whether he has too much equity in his home. Does this make sense for the future, especially after the children move out?

It’s a significant issue for families living in VHCOL areas. On one hand, real estate tends to appreciate over time, as evidenced by the 7.9% annual appreciation he’s enjoyed over the past seven years. On the other hand, having too much wealth tied up in a single asset, especially one that isn’t liquid, can limit financial flexibility.

So, what should he do? Here are some things I think he should think through to make a decision:

Once the kids move out, the space will likely be far more than needed for a couple. Downsizing can free up their cash and add liquidity to their portfolio. However, as the Redditor points out, his wife wants to retain the home for the kids, as the housing market in the area is very expensive. There is also some emotional attachment to the home.

All of this makes things about much more than just emotions. Even if they decide to keep the home, how would they split it between two children?

It could also lead to pressuring the children to live nearby, which may influence their life decisions.

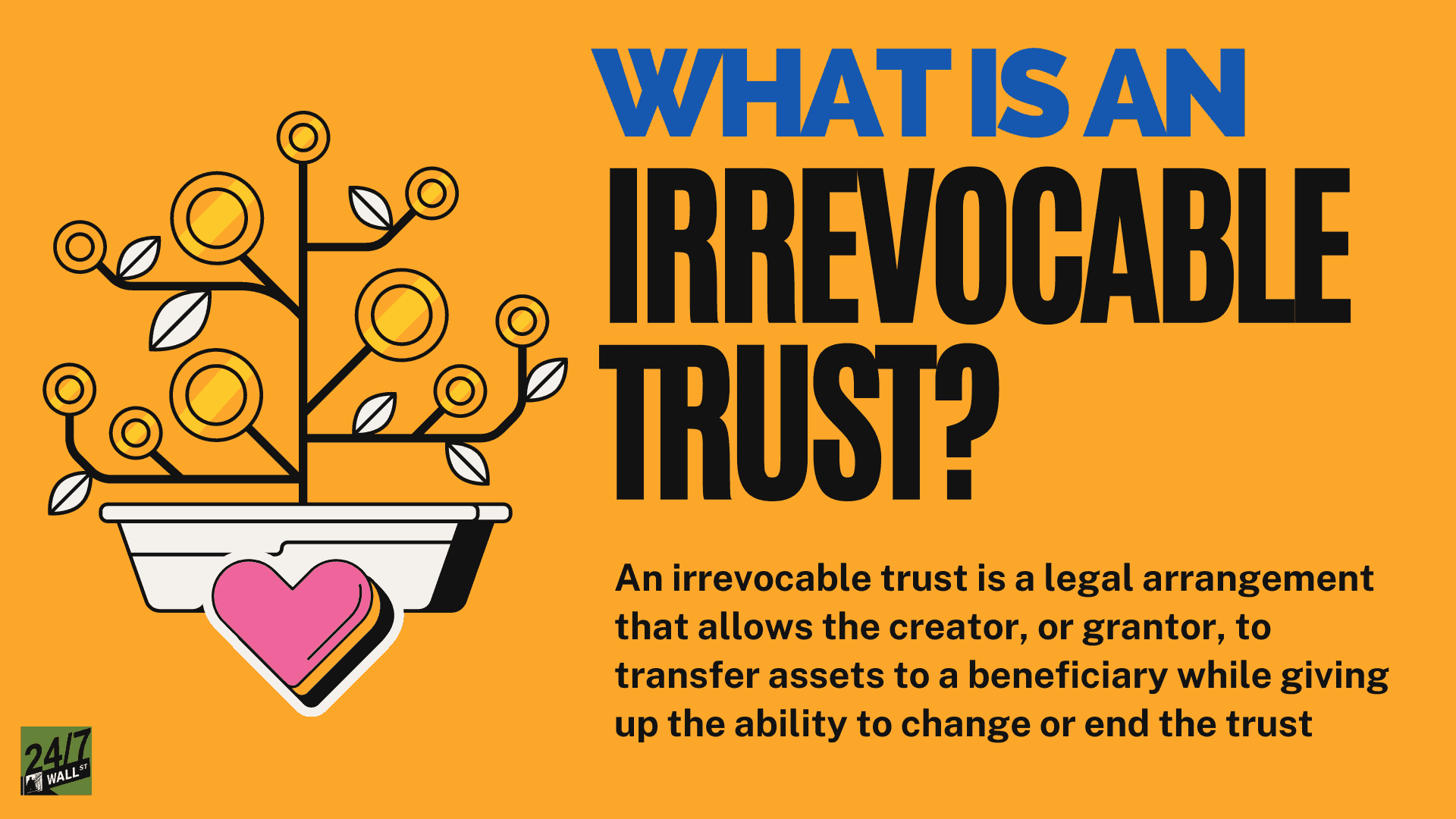

The Redditor is considering placing the home in a trust, with a plan for the kids to liquidate and divide the money later. This addresses concerns over dividing the property, but it places even more of the family’s net worth into real estate. Ultimately, this could make their financial situation less flexible, which may be an issue in the future.

Real estate is generally illiquid, and market conditions strongly control how much they can get for the home.

On the other hand, the poster could move forward with his original plan of selling the home after the kids move out. Downsizing to a smaller, more manageable property could free up capital and allow for a higher standard of living while also simplifying estate planning.

However, this would also trigger a sizeable tax bill. I highly recommend consulting a tax professional in this case, as this could be a huge factor.

In my opinion, the poster might want to consider a hybrid solution. Depending on the exact market the poster is located in, it may make sense for him to look at “gradual liquidation.” The poster may want to consider renting out the property for income while living in a smaller home. This would allow them to benefit from the appreciation of the property without locking too much of their net worth in a single asset.

If he decides that leaving the home to the kids is the best solution, it’s vital to map out a clear estate plan. A professional can help set up trusts that ensure the children’s inheritance is fair while minimizing the tax burden.

Ultimately, the decision comes down to what kind of life they want after their kids have moved on and how they want to allocate their wealth for the next generation. The couple also needs to consider their own retirement planning and how their home will work into that.

Retirement planning doesn’t have to feel overwhelming. The key is finding expert guidance—and SmartAsset’s simple quiz makes it easier than ever for you to connect with a vetted financial advisor.

Here’s how it works:

Why wait? Start building the retirement you’ve always dreamed of. Click here to get started today!

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

Our expert who first called NVIDIA in 2009 is predicting 2025 will see a historic AI breakthrough.

You can follow him investing $500,000 of his own money on our top AI stocks for free.