Benjamin Franklin is famous for many things, including the following quote: Our new Constitution is now established, and has an appearance that promises permanency; but in this world nothing can be said to be certain, except death and taxes.

Death and taxes are two dreaded topics that are closely aligned. Their confiscatory premise is a continual source of perceived injustice and strategic planning to find a workaround or loophole to give more to family members without government pilferage. Gift taxes were created by Congress and the IRS to serve as a deterrent to those seeking to give funds to family before their demise, when estate taxes (i.e., Death Taxes), would apply to the existing estate’s total worth.

Dave Ramsey is the host of a syndicated radio show about financial advice. He recently addressed the topic of gifting when a caller wanted to give a large sum to his son-in-law for growing his business without triggering gift taxes.

The Caller’s Dilemma

Dave Ramsey’s syndicated radio show regularly gives financial tips to listeners seeking guidance.

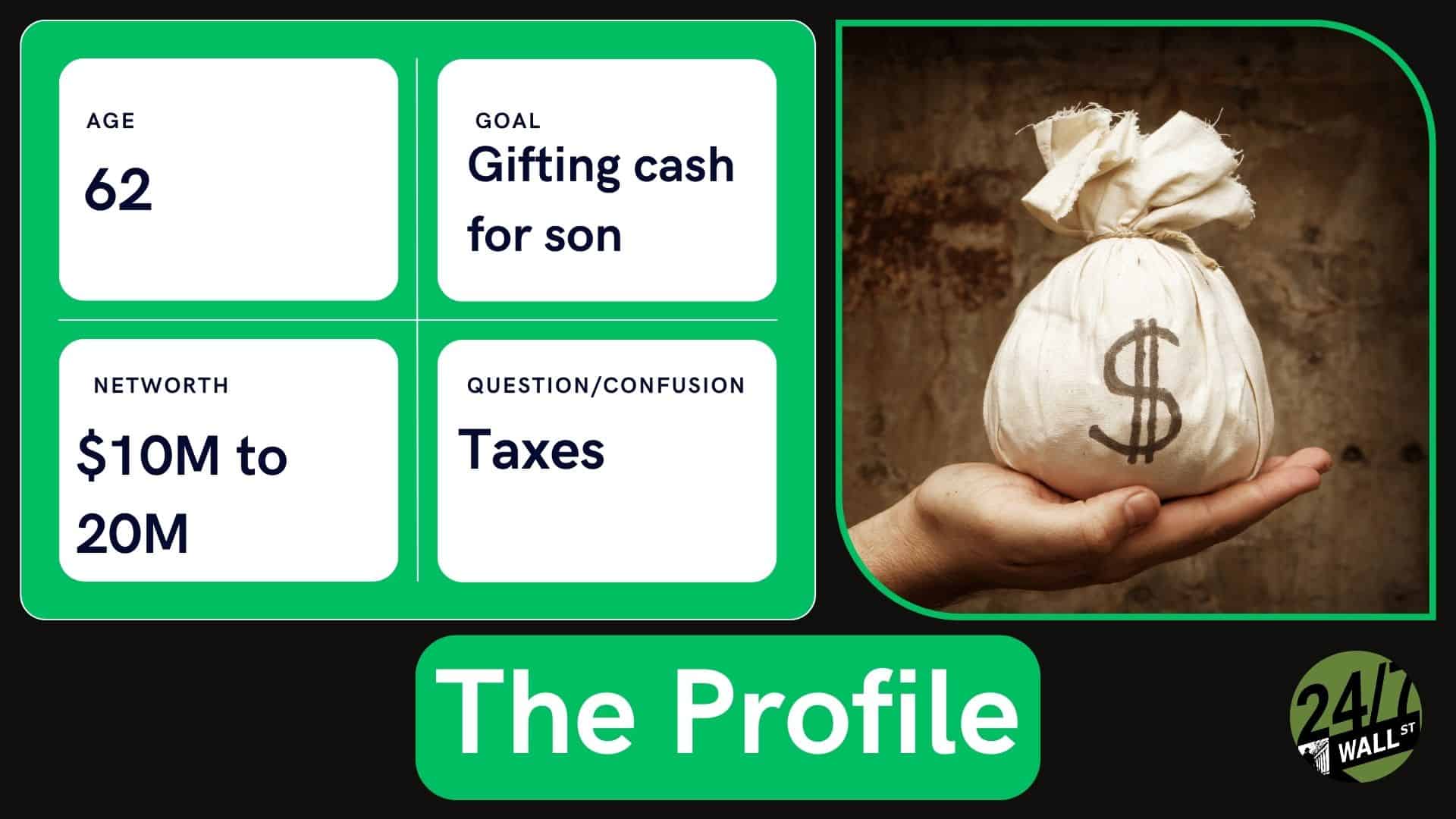

62 year-old with net worth of $10-12 million wishes to gift money to his son-in-law for his musical instrument repair business,

He proposed treating the initial funds (roughly $300,000) as a property or mortgage loan note for the son-in-law to purchase or rent a larger workshop space.

Subsequent cash gifts under the $18,000 threshold could be used by the son-in-law to pay off the loan by installments, thus avoiding the gift tax.

Ramsey’s Advice

Ramsey concurred with and preferred the caller’s plan. As an alternative choice, he suggested the following:

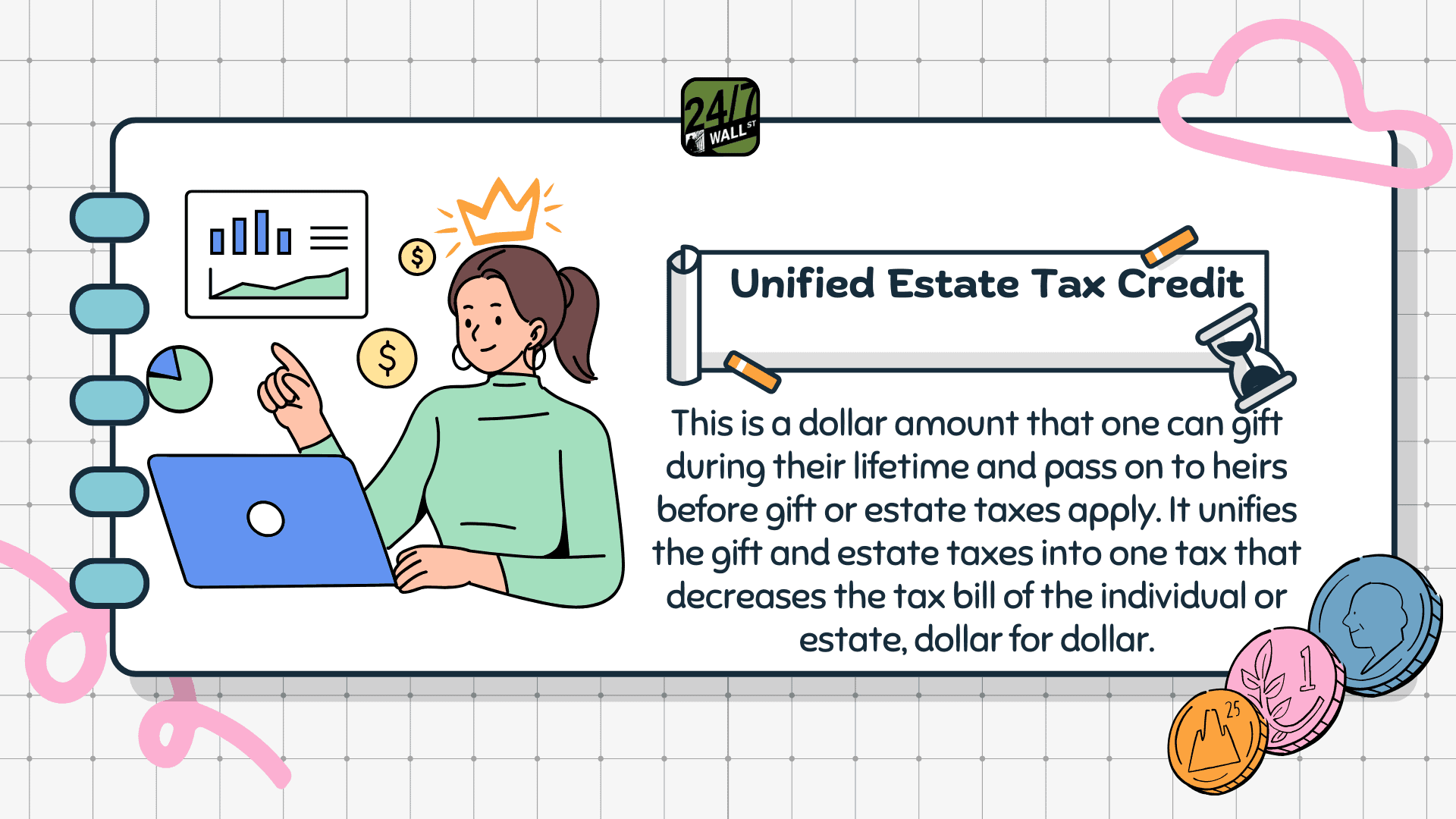

Using part of the Federal estate tax exemption and declaring the $300,000 as part of the exemption ($23 million as of 2024).

Use of the Unified Estate Tax Credit while alive reduces the exemption after one’s demise.

Noting that the caller was still relatively young at age 62, his estate would probably continue to grow to possibly exceed the estate tax exemption cutoff, so taking the credit earlier might result in a larger tax liability later on.

Ramsey noted that the estate tax threshold could be higher or that the tax itself could possibly be eliminated under a Trump presidency, as that was a campaign issue.

Under the caller’s plan, he might also take advantage of the higher bracket trend of gift tax triggers, which have gone from $14,000 to $18,000, and may reach $20,000 if the trend continues in the near future.

Ramsey also added that loan forgiveness, which is also non-taxable, could be a component of the caller’s will document.

The loan note could just be a one page record that is updated by hand and initialed each year, as acceptable to the IRS.

Takeaways and 24/7 Key Points:

My personal experience in small business finance concurs with both the caller’s and Ramsey’s plans and comments. Perhaps the only additional consideration to add might be to structure the deal like a venture capital financing if the son-in-law’s expansion plans involve taking on future investors or a buyout offer from a larger competitor down the road. The caveat, however, is that the payments would trigger a 1099 tax for the caller. This would be the following:

If the father-in-law is a shareholder rather than a creditor of record, the company’s balance sheet looks stronger, since the gifts being paid off can be counted as dividends instead of debt, per se. This is more attractive to both outside investors and acquisition minded larger entities.

As a passive shareholder, the son-in-law would still have decision making power, and the father-in-law would just share any sale of the company on a pari-passu basis.

The father-in-law would then get to have the dividends taxed as passive income instead of any earned income at a higher rate, assuming he is still working. Conversely, the repayments from a loan would be tax free until accrued interest exceeded the principal amount of the loan.

This article is intended to be strictly informative and opinion-based only, and not construed to be tax or financial advice. It is advised that professional tax and financial counseling be sought before undertaking any steps in that field.

Take Charge of Your Retirement In Just A Few Minutes (Sponsor)

Retirement planning doesn’t have to feel overwhelming. The key is finding expert guidance—and SmartAsset’s simple quiz makes it easier than ever for you to connect with a vetted financial advisor.

Get Matched with Vetted Advisors Our smart tool matches you with up to three pre-screened, vetted advisors who serve your area and are held to a fiduciary standard to act in your best interests. Click here to begin

Choose Your Fit Review their profiles, schedule an introductory call (or meet in person), and select the advisor who feel is right for you.