Personal Finance

I'm 56 and suddenly have $5 million in my 401(k) - how should I think about retirement?

Published:

Last Updated:

24/7 Wall St. Key Takeaways:

Managing the taxes on a growing 401(k) as you approach retirement can be daunting, especially if you’re seeing a large amount of growth. For one Reddit user, a $5 million 401(k) is projected to grow to $8-9 million by age 62, and they’re looking for smart ways to handle the potential tax burden.

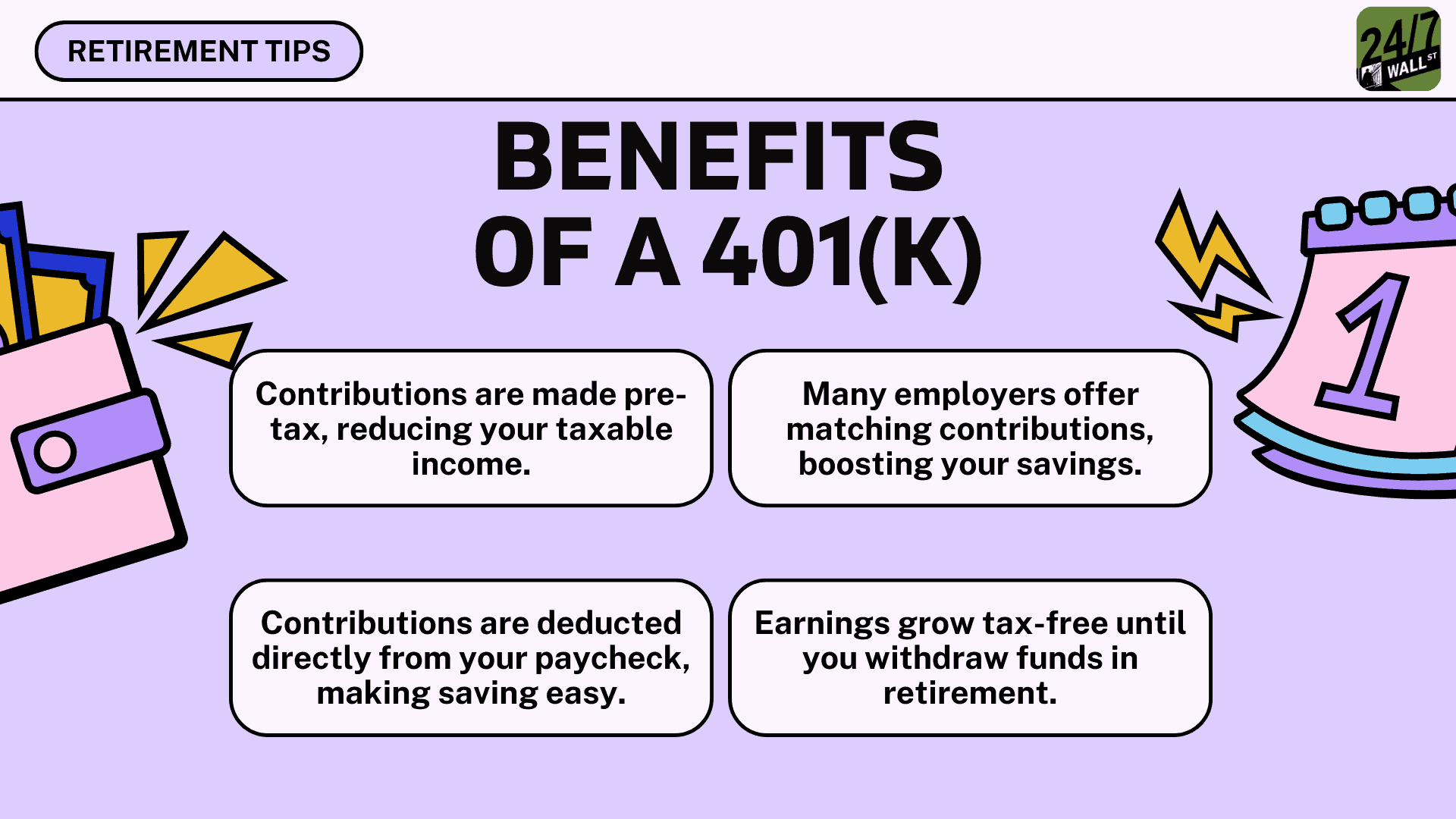

With the company’s stock swelling in value, strategic tax planning is essential to ensure that this portfolio remains beneficial without being eaten up by a high tax rate. Several options, like diversification and Roth conversion, can help reduce this tax liability.

In this article, we’ll explore the potential ways to manage the taxes on this growing retirement portfolio.

When it comes to finance, learning from others’ situations is one of the best ways to develop a wise financial plan. According to a recent study by Vanguard, the average 401(k) balance for Americans between the ages of 55 and 64 is $244,750. So, while you might not be in this exact situation yourself, you never know when some wisdom gleaned from another’s situation will help yours. And if $5 million seems like an unattainable amount, remember… Just $600 contributed per month for 40 years, at a 11.50% rate of return (the nominal annualized total of the S&P 500 from 1983 to 2023) would have grown to around $5 million today!

Seeing someone’s 401(k) perform so well is amazing, especially with the continued growth that’s expected. Approaching retirement with $5 million, and potentially $8-9 million, is a fantastic position to be in! However, there are several suggestions we’d recommend keeping in mind to help manage taxes at retirement:

There are several potential approaches the poster could take:

Lastly, this individual could benefit significantly from working with a financial advisor due to the complexities of managing a rapidly growing 401(k) heavily invested in company stock. A financial advisor can help diversify the portfolio to mitigate risks associated with overconcentration. They can also provide strategic tax planning, such as exploring Net Unrealized Appreciation (NUA) strategies and Roth conversions, to reduce tax liabilities upon withdrawal.

With potential large distributions that may push them into higher tax brackets and required minimum distributions to consider, professional guidance is crucial to optimize their retirement funds and ensure long-term financial security.

Start by taking a quick retirement quiz from SmartAsset that will match you with up to 3 financial advisors that serve your area and beyond in 5 minutes, or less.

Each advisor has been vetted by SmartAsset and is held to a fiduciary standard to act in your best interests.

Here’s how it works:

1. Answer SmartAsset advisor match quiz

2. Review your pre-screened matches at your leisure. Check out the advisors’ profiles.

3. Speak with advisors at no cost to you. Have an introductory call on the phone or introduction in person and choose whom to work with in the future

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

Our expert who first called NVIDIA in 2009 is predicting 2025 will see a historic AI breakthrough.

You can follow him investing $500,000 of his own money on our top AI stocks for free.