Personal Finance

I'm 52 and I just hit the $5 million mark in saving - how can I start to generate income to live off of?

Published:

Last Updated:

While scrolling through Reddit, I recently came across a post by Amazing_Bobcat8560, who had just hit $5 million in retirement savings. While this was a huge milestone, he is beginning to see that living off of his $5 million is more complicated than he first considered. How can you live off of it without risking depletion?

Having a structured financial plan is vital not only to generate income but also to keep you from running out of money prematurely.

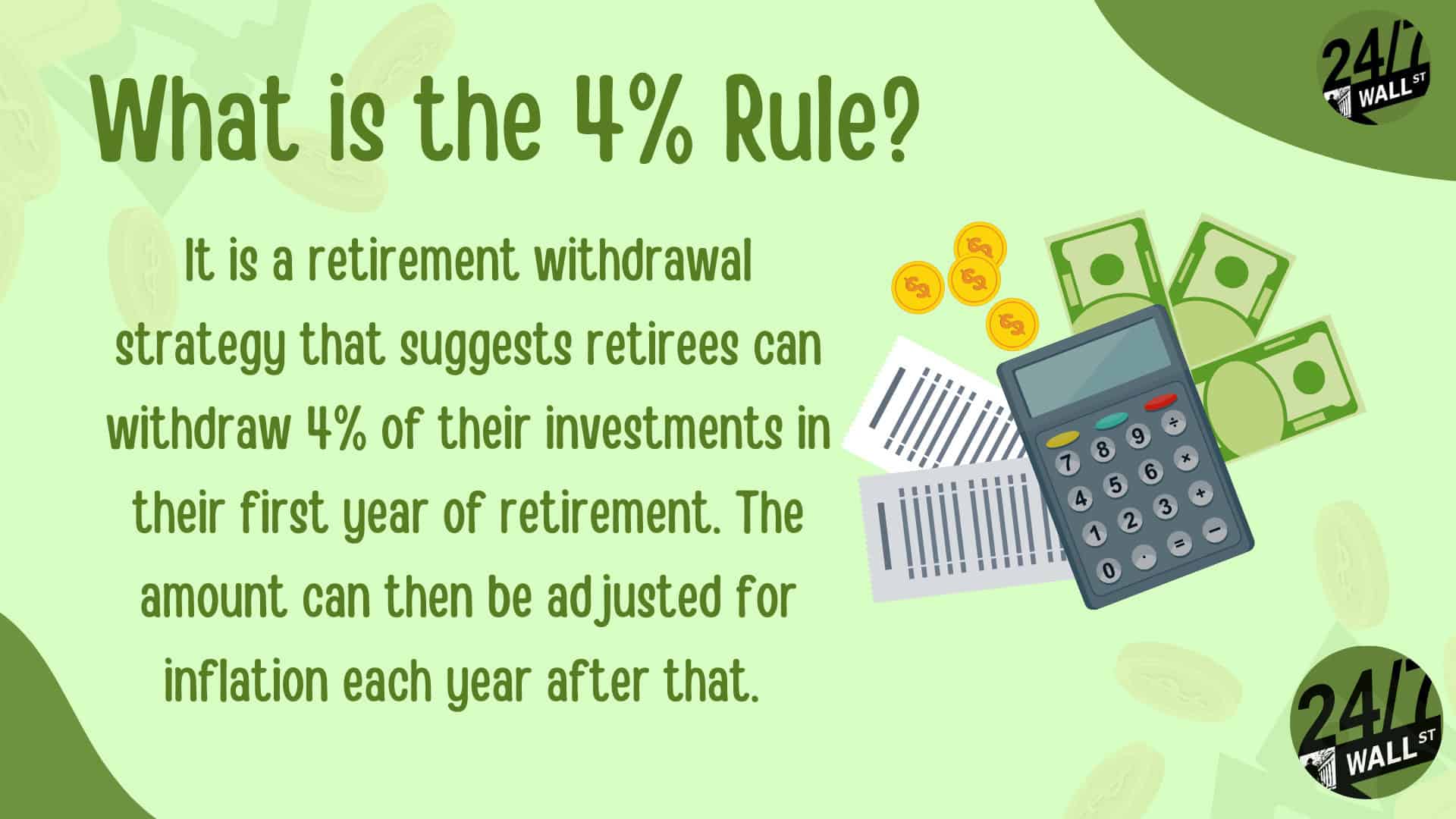

When you hit your financial independence number, it’s important to realize that how you generate your income is just as important as how much you withdraw each year. Our poster did mention the 4% rule, but how you implement that could mean all sorts of things – dividends, capital gains, or a mix of assets.

(That said, the 4% retirement rule may be dead.)

Let’s dive into my recommendations. These thoughts are just my opinion and shouldn’t be considered financial advice:

I would never recommend relying on one income stream. It’s wise to diversify. A balanced approach might look like using dividend-payings stocks while strategically selling equities to capture capital gains.

Rental properties can be another source of passive income, but it’s important to remember that they carry their own risks. You should never try to live solely off of rental income in retirement.

A common mistake that can seriously hurt your wealth is panic selling when the market drops. Yes, you want to avoid losing your hard-earned savings, but it’s important to stick to your investment plan.

A cash buffer of a year or two of living expenses can help keep you from selling off investments at the wrong time.

Taxes play a big role in how long your $5M lasts, too. Dividend income can be taxed at a higher rate than capital gains, for instance. You may benefit from a blend of both, but the tax question should drive some of your financial decisions.

| Taxable Income Range | Income Tax Rate | Long-Term Capital Gains Tax Rate |

|---|---|---|

| $0 to $23,200 | 10% | 0% |

| $23,201 to $94,300 | 12% | 0% |

| $94,301 to $201,050 | 22% | 15% |

| $201,051 to $383,900 | 24% | 15% |

| $383,901 to $487,450 | 32% | 15% |

| $487,451 to $731,200 | 35% | 15% |

| $731,201 and above | 37% | 20% |

I recommend working with a tax professional to optimize your withdrawals for tax efficiency.

Retirement planning doesn’t have to feel overwhelming. The key is finding expert guidance—and SmartAsset’s simple quiz makes it easier than ever for you to connect with a vetted financial advisor.

Here’s how it works:

Why wait? Start building the retirement you’ve always dreamed of. Click here to get started today!

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

Our expert who first called NVIDIA in 2009 is predicting 2025 will see a historic AI breakthrough.

You can follow him investing $500,000 of his own money on our top AI stocks for free.