Personal Finance

I'm 61 and planning to live off my portfolio until I turn 70 and can claim the maximum Social Security - is this too risky?

Published:

Last Updated:

One of the most discussed subjects in retirement planning is Social Security benefits and the age at which one should start receiving them.

While you can elect to take them as early as 62, most financial planning experts suggest that it’s more advantageous — assuming you’re in good health and don’t need them to live on — to wait for your full retirement age of 67 (all those born in 1960 or later) or even to 70.

In this case, you are 61 years old, which makes 67 your full retirement age because you were born in 1960 or later. You’ve decided that the benefits of waiting to 70 outweigh any disadvantages of delaying receiving Social Security.

You plan to live off your investment portfolio until you turn 70. While everyone’s situation is different based on annual living expenses and lifestyle, the pros and cons of doing this are relatively straightforward and not necessarily risky.

Here’s why.

Financial services firm Corebridge Financial hired Morning Consult in May 2023 to survey 2,284 American adults between the ages of 22 and 75 with household income and assets of $35,000 each about their retirement expectations and longevity.

Morning Consult for the Longevity Project conducted a second survey in April 2022, asking 2,202 adult Americans about their thoughts on retirement, longevity, and the future of work. These respondents were between the ages of 25 and 75, had household incomes of at least $25,000, and had $50,000 in investments.

One of the questions asked survey respondents was whether it was their goal to live to 100. Approximately 54% said it was. If you are 61 and this is your goal, 39 years of living expenses need to be provided for.

According to the Bureau of Labor Statistics (BLS), the average annual retirement expense for someone between 65 and 74 was $58,440. For those aged 75 or older, it was $45,756, 28% lower.

Suppose your annual living expenses are similar to those in the former category at $58,440. You must withdraw at least this much from your investments to cover your expenses.

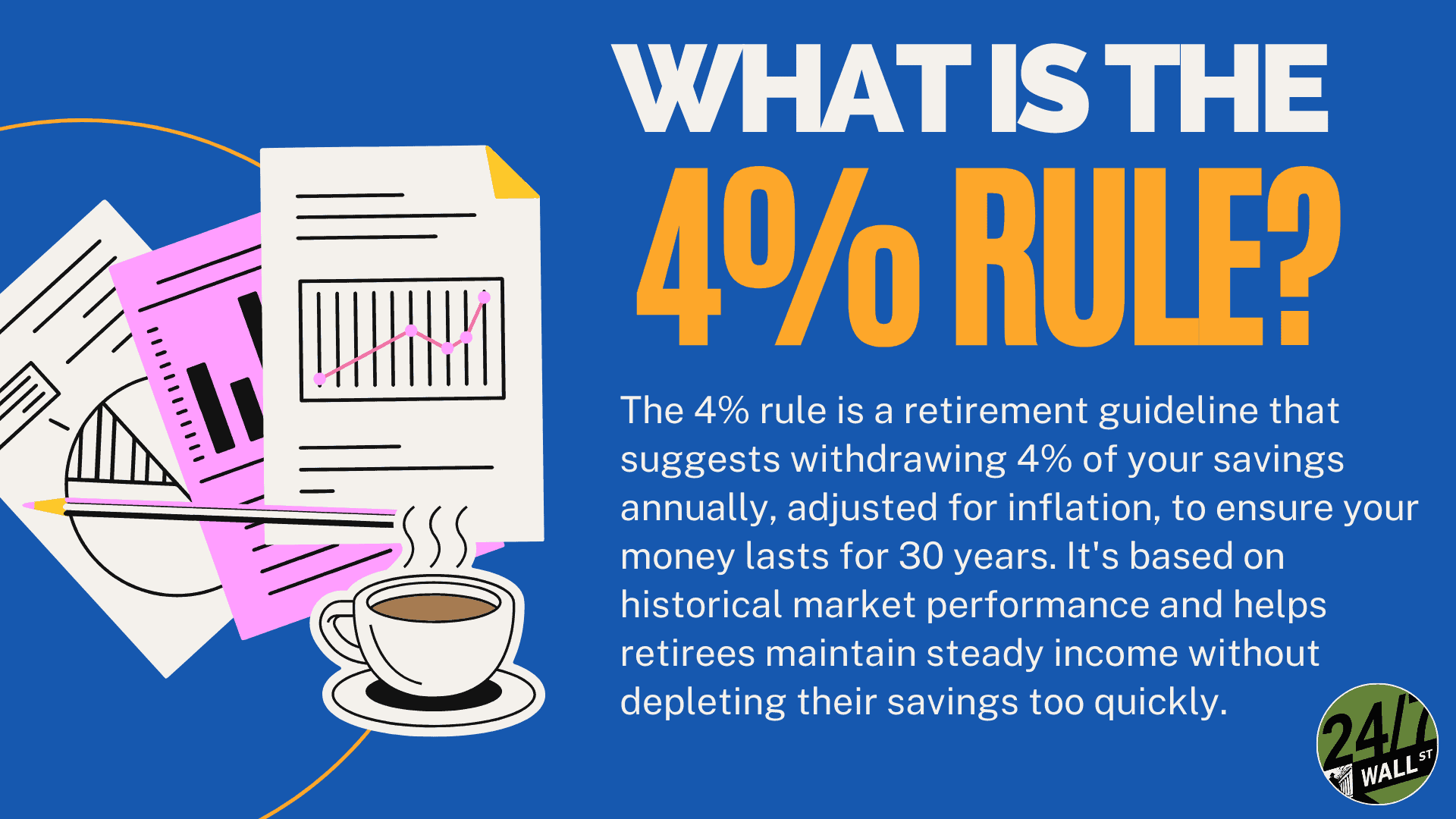

When you first consider the annual income needed to live comfortably, it can be overwhelming. That’s why some retirement experts suggest you use the 4% rule to understand how much you will need in investment assets to meet this target.

The 4% rule means you can comfortably live off 4% of your investment portfolio in your first year of retirement. Each year after that, you would adjust the 4% up or down depending on inflation. The premise is that you could use your investment portfolio to cover your expenses for 30 years.

Due to concerns about longevity and lower Social Security payments in the future, some financial experts have dialed that back to between 3.3% and 3.8% to be safe. You also might want to add $5,000 annually for unexpected expenses.

You then calculate the size of your investment portfolio to meet the 4% rule over the next 30 years. In this case, it would be $63,440 divided by 0.04, which equals $1.59 million.

If you’re 61 now and have this much invested, you should, under normal circumstances, have plenty to cover your expenses until age 91.

The critical thing to understand about the 4% rule is that it doesn’t consider your Social Security benefits. You’ve chosen to hold off receiving them until you’re 70 in nine years.

So, we’ll calculate the estimated Social Security benefits you’ll receive in 2033 at age 70 to understand why you don’t necessarily need $1.59 million in your investment portfolio to cover your annual expenses for the next 30 years.

Using SmartAsset’s Social Security Calculator, your 2033 Social Security benefit would be $51,194, based on $90,000 in current income. That would increase yearly by the inflation rate to $83,990 in 2058.

There are a few assumptions made to calculate your benefit. These are right from the SmartAsset website.

Based on the $51,994 in Social Security benefits you would receive at age 70 in 2033, the value of those payments in today’s dollars is $33,000, 52% of your annual expenses estimate of $63,440 from earlier.

This means that for the next nine years (61-70), you will need to withdraw $63,440 annually, adjusting for inflation, from your investments. For 25 years after that, you’ll only have to withdraw approximately $33,440, adjusting for inflation.

The bottom line: Given you will receive Social Security benefits starting in 2033 at age 70, you shouldn’t need $1.59 million in your investment portfolio to cover 30 years of living expenses. Based on 3% inflation, it would be more like $745,000.

However, it is always advisable to seek advice from a qualified financial planner or other suitable financial advisory professional.

Are you ahead, or behind on retirement? For families with more than $500,000 saved for retirement, finding a financial advisor who puts your interest first can be the difference, and today it’s easier than ever. SmartAsset’s free tool matches you with up to three fiduciary financial advisors who serve your area in minutes. Each advisor has been carefully vetted and must act in your best interests. Start your search now.

If you’ve saved and built a substantial nest egg for you and your family, don’t delay; get started right here and help your retirement dreams become a retirement reality.

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

Our expert who first called NVIDIA in 2009 is predicting 2025 will see a historic AI breakthrough.

You can follow him investing $500,000 of his own money on our top AI stocks for free.