Personal Finance

We're 50 with $1 million in a IRA and want to convert it to a Roth - should we do it now or wait until 65?

Published:

Last Updated:

24/7 Wall St. Key Takeaways:

As you approach retirement, decisions about tax-efficient strategies suddenly become very important. I discovered a recent Reddit post in which a user shared their experience with a Roth conversion tool, which revealed contributing insights about when they should convert IRA funds to a Roth account.

Conventional wisdom suggests waiting until the age of 65 to 70 to take advantage of the lower tax bracket. However, the poster found recommendations advocating for conversions within their current 24% tax bracket.

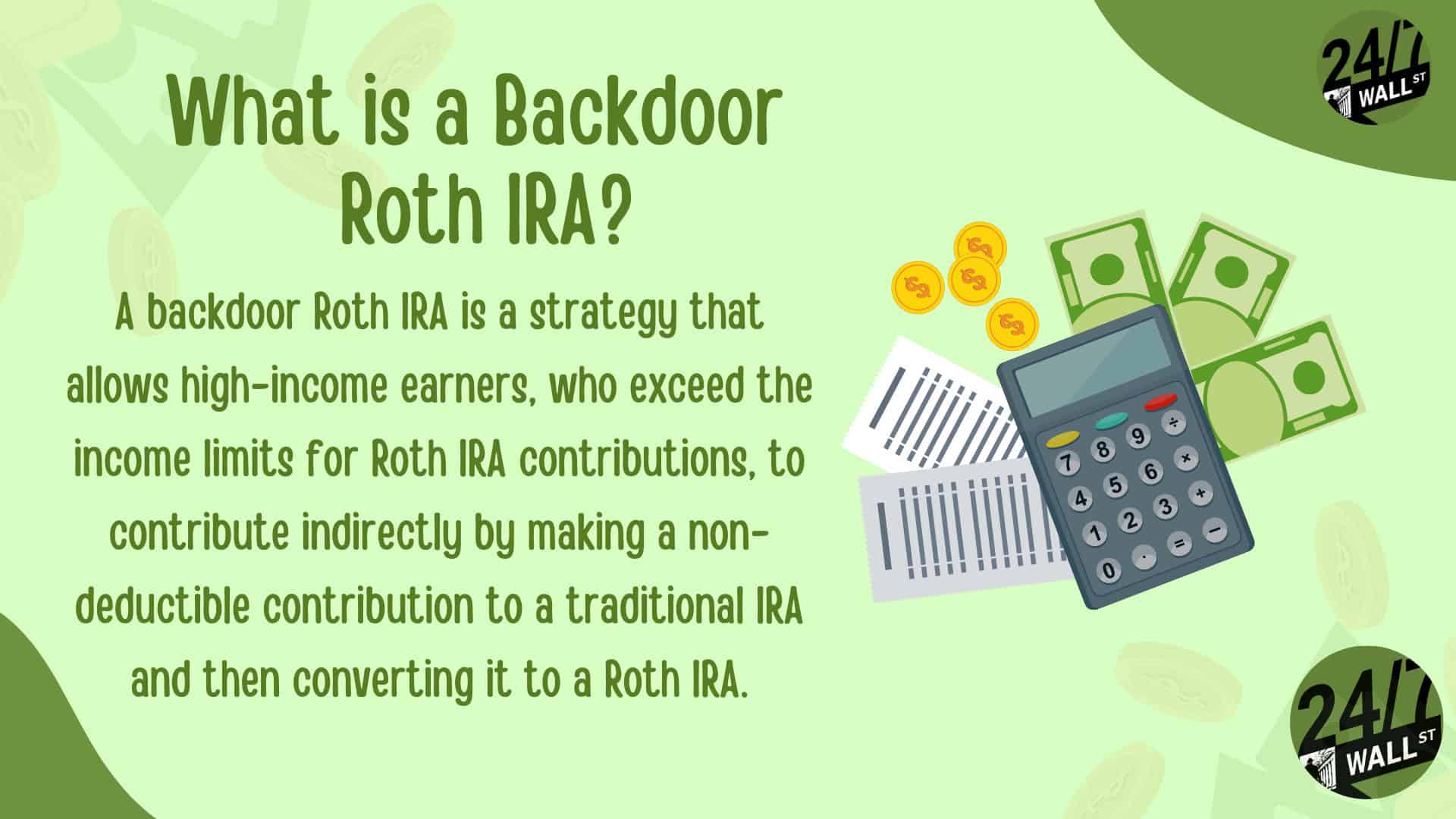

(I’ve also covered backdoor Roth IRAs, if you’re interested in reading more about this tax strategy.)

With tax implications looming, this discussion prompted my interest in how to maximize retirement savings and minimize tax burdens. Let’s explore key considerations that can help you navigate this critical decision and enhance your financial strategy as you approach retirement.

The common wisdom of converting between ages 65 and 70 is largely due to tax brackets. During these years, you’re likely making less, so the money will be taxed at a lower tax bracket.

However, there is also an argument for converting to the top of the 24% bracket, as there is a potential for tax hikes in the future. You have to consider that future taxes may be more than 24%, even after retirement.

Most Roth conversion tools (including the one mentioned in the post) emphasize maximizing estate value, which considers how tax-efficient your assets will be when your heirs inherit. Converting now can reduce the tax burden on your beneficiaries, who would otherwise face potential taxes on a large IRA balance upon your passing.

This proactive approach can outweigh the conventional wisdom of waiting until you’re closer to retirement, especially if you have declining health.

By converting your traditional IRA funds to Roth accounts sooner rather than later, you allow those assets to grow tax-free for a longer period. This can be a huge advantage if your investments are expected to grow substantially in the years leading up to retirement.

Having a healthy balance in Roth accounts provides flexibility when it comes time to pull the money out of your accounts. This allows you to manage your income in retirement strategically in a way that lowers your taxes.

By depleting your traditional IRA first through conversions, you can potentially keep your taxable income lower during your retirement years.

Maintaining a mix of tax-deferred (traditional IRA) and tax-free (Roth) accounts can be a solid strategy. This diversification allows you to optimize your tax situation annually. You could adapt to changes in tax laws or your income needs.

Given the complexities of tax strategies, it’s wise to consult a tax professional or financial advisor before making a decision. Your specific financial situation is unique, and you need a personalized plan that considers your local laws and future needs.

Retirement planning doesn’t have to feel overwhelming. The key is finding expert guidance—and SmartAsset’s simple quiz makes it easier than ever for you to connect with a vetted financial advisor.

Here’s how it works:

Why wait? Start building the retirement you’ve always dreamed of. Click here to get started today!

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

Our expert who first called NVIDIA in 2009 is predicting 2025 will see a historic AI breakthrough.

You can follow him investing $500,000 of his own money on our top AI stocks for free.