Personal Finance

The Typical American Can’t Answer These Simple Retirement Questions

Published:

Last Updated:

Are you worried about retirement? Stressed about your retirement savings? Do you have questions about retirement? You’re not alone. We found some of the most common questions that potential retirees struggle to answer. Here are the top 20.

You can retire whenever you want, but the measure people use to decide when to retire is how much they have in their savings account. If you have enough money saved to live on for the rest of your life, the decision of when to retire is entirely up to you.

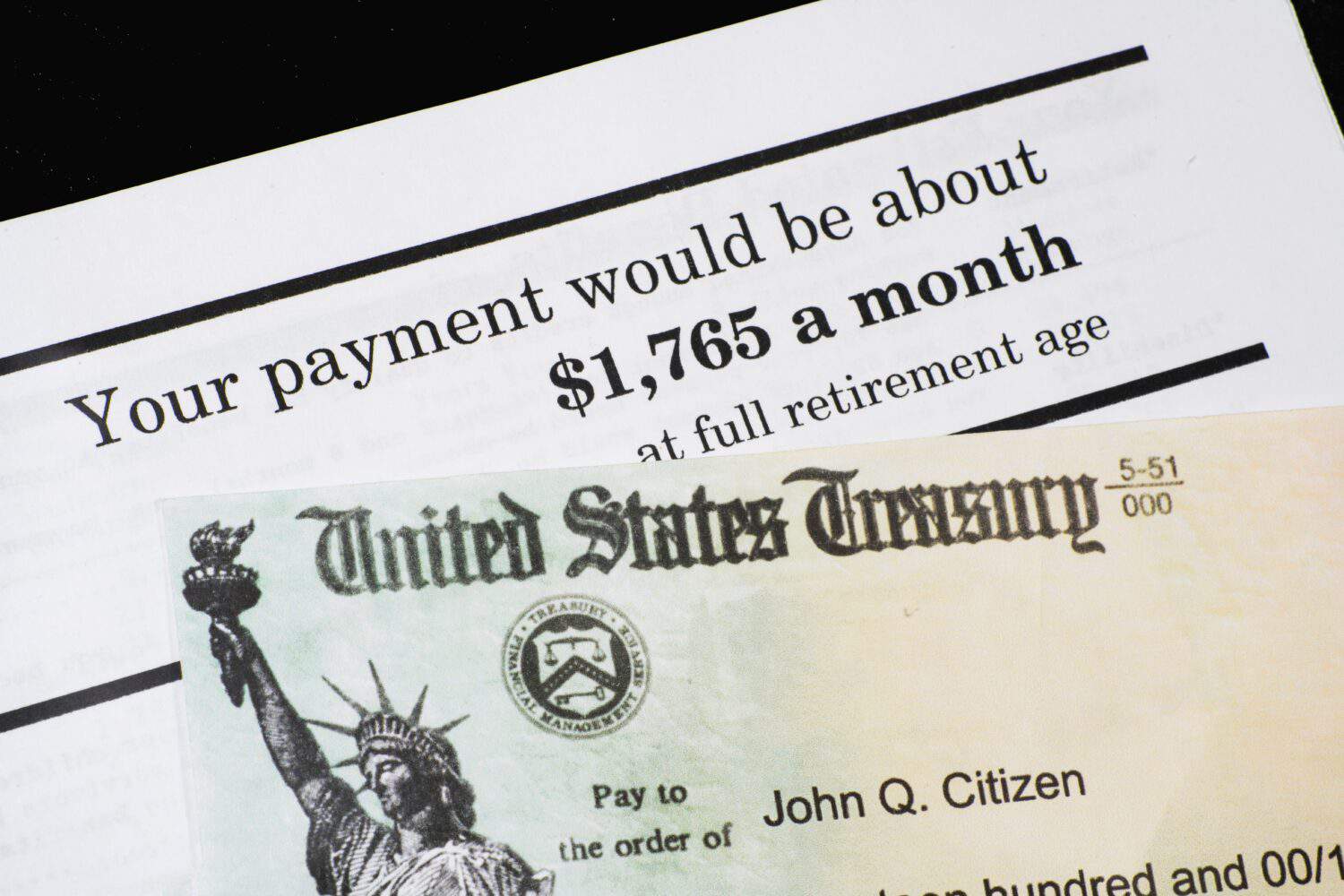

Your monthly Social Security benefits depend on a number of factors including the age at which you retire, how much you earned during your ten most productive years, the current laws regarding Social Security, and more. Thankfully, there are a number of online tools that can help you estimate how much you will receive.

Filing for retirement is as simple as talking to the HR representative at your company who can file the documents for you. Or, if you are self-employed, all you have to do is submit a form yourself to the government.

Maybe. Both major political parties have been complicit in raising the retirement age and voicing concern about the future utility and availability of Social Security. However, the Republican party has made consistent and worrying progress toward reducing social security and other retirement benefits. In 2024 alone, they have proposed budget cuts to Medicare, Social Security, the Affordable Care Act, and price increases to drugs, energy, and housing. It is safe to say that a republican majority will probably reduce any benefits for future retirees.

Politicians love to spread fear about Social Security during election season, but there is currently no risk of retirees running out of Social Security. Today, there is a risk that future retirees will only receive around 83% of today’s benefits unless Congress acts, however.

It depends. If you have a more expensive lifestyle or plan to maintain your level of expenses then you are going to need more to retire than someone who has a frugal and common-sense lifestyle or plans on reducing their expenses after retirement. A professional financial planner or online calculator can help you decide if you have enough to retire.

You can maximize your social security by delaying your retirement until age 70 which will raise the amount of money you will receive based on how many years you didn’t retire after age 62. You can also make sure you work for at least 35 years, include family and dependents, minimize any taxes that will be deducted from your payments, claim any spousal payments, and a few other minor adjustments.

Other factors like work history and earnings are a little bit outside your control.

Yes. Social Security is a federal program so you can move to a different state or even live outside the United States permanently and still receive your Social Security payments.

Retirement is a personal choice. If you have enough money to retire and absolutely do not want to work, then you can definitely retire, but there is no “should” or “shouldn’t” when it comes to when and why to retire. If you enjoy working, you can work forever and never retire, if you want. But too many people are being forced to work low-paying jobs well into retirement age, and for them, the choice of whether to retire is one they will never be able to answer.

This is a fantastic question and one that many people don’t really ask themselves. Are you retiring because you want to, or because it’s simply what you’re supposed to do? In an ideal world, everyone would be able to enjoy their later years without the worry of finances or the fear of losing their home. But we don’t live in an ideal world, and retirees are often at risk of becoming homeless or unable to pay for medical help.

Whatever you want! Golf every day like someone with no imagination, make up for lost time, and try to rekindle a relationship with your grown children after you neglected them for thirty years. The world is your oyster!

You have a few options if you crunch the numbers and realize you don’t have enough money to survive during retirement. First, you can consider not retiring. You can continue to sell your time and life to earn just enough to survive and continue working. This will probably lead to an earlier death and a multitude of emotional and mental problems. Second, you can consider ways to reduce your expenses and make your savings and Social Security last longer. Some ways to do this include moving to a cheaper area, moving in with family, selling vehicles, using only one car (or living in a place that doesn’t require a car at all), or living a less expensive lifestyle.

That depends on what your most productive working years looked like. Social Security only takes your most productive working years into account, not the average of your entire life. As long as you have at least ten years of high salary, then your Social Security should be fine. Also, as long as you continue to contribute to your retirement savings account(s) and don’t withdraw from it early, it won’t be going anywhere.

Many people don’t know that retirement doesn’t have to be permanent, and you can begin working again whenever you want. Some people do this because they get too bored during retirement and want to keep busy, others run out of money and have to return to a job in order to survive.

Yes. If you are above the retirement age at the time of your second retirement, you can retire whenever you like. If you retired early the first time and then returned to work, you can’t retire early again and have to wait until retirement age to retire a second time.

You’re on your own when it comes to your health during retirement. Medicare is the only retiree-specific benefit for medical care available in the United States and only pays for some of the cost of a few common procedures and medications. Some companies offer special plans for retirees, but it is still private insurance that you will have to purchase yourself.

As the population ages and the replacement rate in the United States drops, people fear that Social Security might go bankrupt. The truth is Social Security will continue to work even if it begins to face budget shortages. The first of these shortages will probably begin in 2035 but can be avoided with policy changes and new legislation.

Not really. The vast majority of Americans don’t have enough money or enough assets to justify hiring a financial planner. Online guides and resources should be enough to guide you in how to manage your money and plan for retirement.

That depends. All the different types of retirement and savings accounts have the same goal: save money for retirement, but they all differ in how they do it and why. What kinds of accounts you invest in or contribute to depend on your life plans, financial goals, and current financial situation. While we definitely recommend you contribute to one or both or more if you can, don’t feel pressured to do anything with your money if you’re not comfortable with it.

This is an interesting generational question with answers that have equally fascinating answers depending on when you were born.

According to studies, the Baby Boomer and Gen X populations are much more likely to have sufficient savings for retirement that last beyond their death, but are also more willing to spend all that money before they die and less likely to want to leave money behind for family. When these generations approach death, they are more likely to spend frivolously so they can use all the money before death.

The Millennial generation, however, is much more likely to fall short of retirement savings goals, but are also more willing to leave money behind for family or charitable causes. They are more likely to save money so they have something to leave behind, if possible.

If you do outlive your savings, we would recommend you leave it to those who might need it or could use it.

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.