Personal Finance

We're in our 50s with $3.4 million saved for retirement - is it realistic that we can live off of just the interest?

Published:

Last Updated:

For those with sizeable or rapidly growing retirement nest eggs, it can make sense to stay invested in markets as one seeks to live off the interest or dividend payments. Undoubtedly, living off the cash flow your investment portfolios produce instead of the invested principal will ensure you do not run out of money in retirement. Further, it may also help your nest egg gain continue to grow in your golden years. Indeed, it is possible to keep making money while you sleep once you’re retired and no longer produce an employment income.

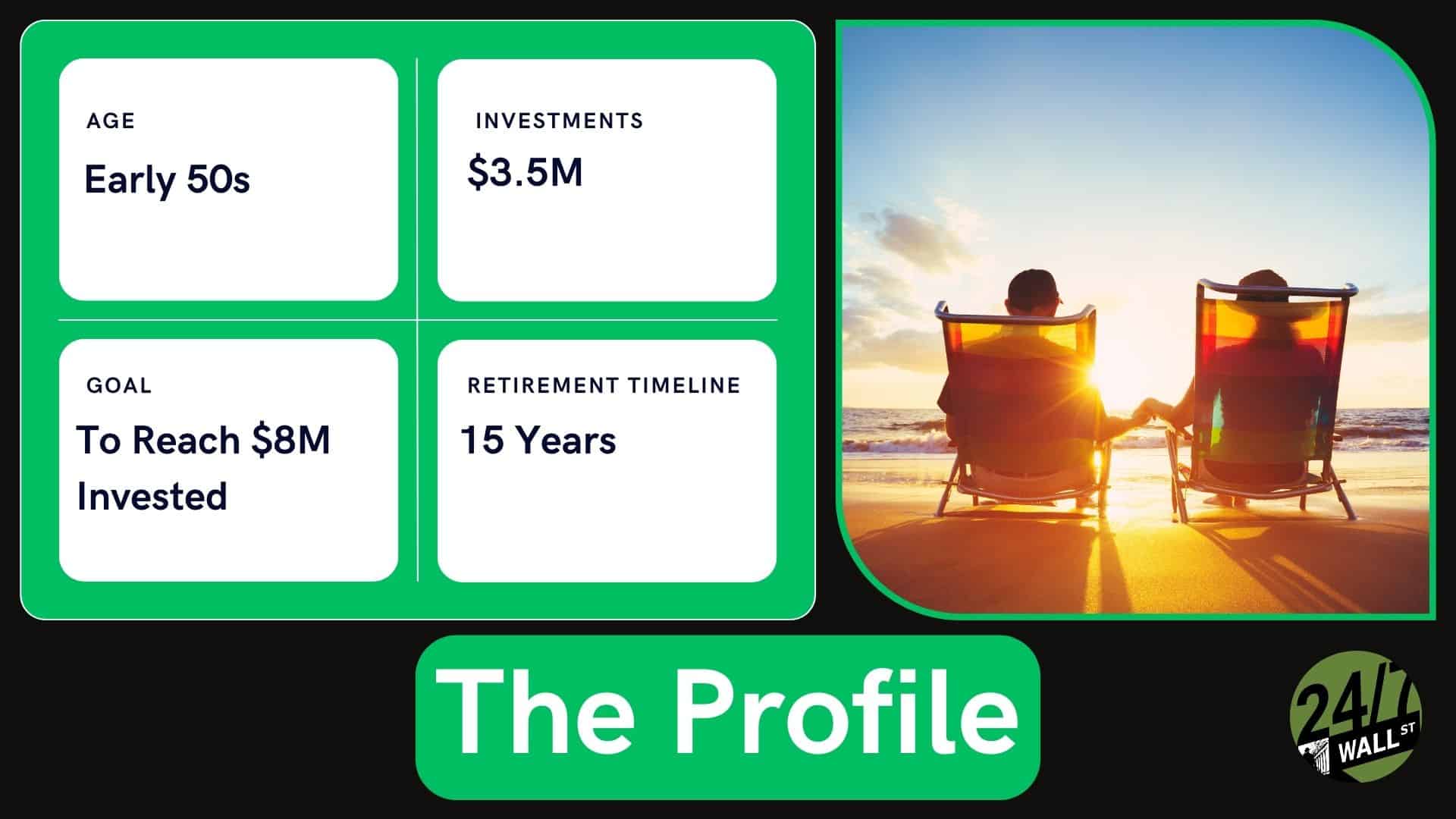

In this piece, we’ll check in with a couple in their early 50s (worth $3.4 million) who’s continuing to drive forward with the ambition to save $8 million in the final 15 years in the workforce. Undoubtedly, anyone with a few million in the bank would likely be slowing down towards the latter decade and a half of their career. But not this couple. They’re ready to sprint towards a finish line that may very well enable them to live off interest while potentially allowing them to leave behind a jumbo-sized nest egg for others when the time comes.

The multi-million-dollar question remains: is it realistic to live off just interest without having to nibble away at the principal? Let’s dig deeper.

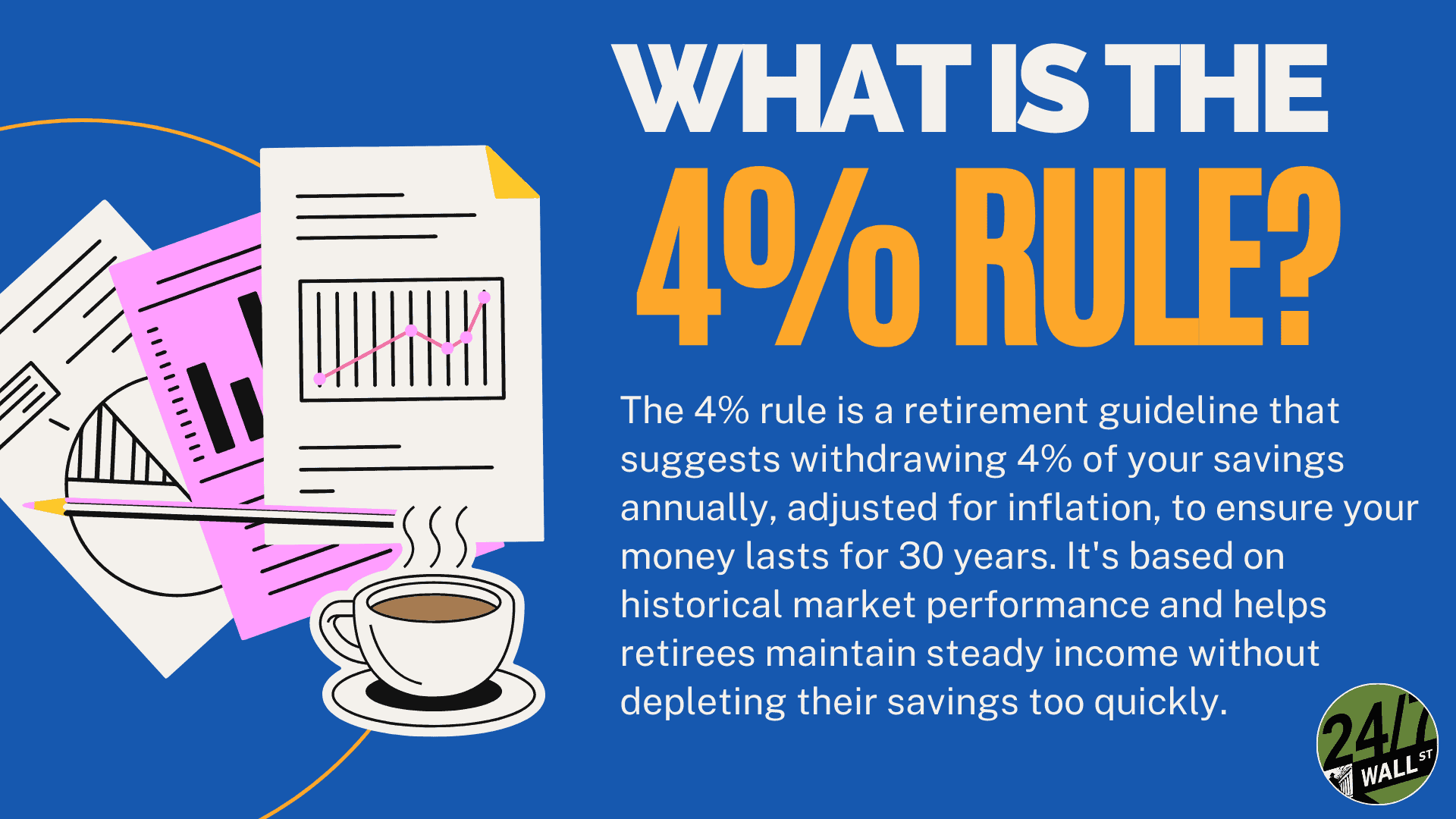

It’s a very difficult task to live solely off the interest of one’s retirement funds. That said, the couple has a plan, and they seem as motivated as ever to achieve it. If they can hit the $8 million target in 15 years, I have no doubt they can live off dividends, interest, and passive income in their retirement years. The 4% rule of thumb would grant them $320,000 in annual income, which is actually quite a “chubby” retirement.

Heck, even averaging a 2% yield from their nest egg would yield more than enough to cover a fairly comfortable lifestyle ($160,000) for most. As the couple eventually moves from their early (so-called “go-go” years) and eventually into their “slow-go” and “no-go” years, which entails less spending later in one’s life, perhaps there’s flexibility to reinvest any interest and dividends the couple doesn’t end up spending. Additionally, spoiling loved ones with extra cash is also an option worth thinking about.

Either way, I would say the couple is well on their way to achieving their ambitious dream of living off passive income (interest and dividends) without having to touch the principal. As always, though, one should consult a financial planner to ensure they stay on the right track, as the stock market is bound to take some really big hits to the chin over the next 15 years.

In the case of this couple, it’s entirely realistic that they can retire at around 65 with a nest egg that’s sizeable enough to allow them to live off the interest. Arguably, if they’re invested wisely, I wouldn’t be surprised if they could achieve the $8 million milestone a bit before their expected retirement date.

Either way, the couple should be aware of potential setbacks in retirement that may require them to tap into the principal at some point. Notably, health- and care-related expenses can be a thorn in the side of many retirees going into the latter half of one’s retirement.

To mitigate such risks, insurance products may be worth consideration. At the same time, I believe there’s no harm in taking some principal off the table in an emergency scenario, especially if one’s nest egg could be worth close to $10 million (or more) by the time the couple’s in their 80s or 90s.

In short, the couple is in great shape as they look to enter their last 15 years in the workforce. If they achieve a $8 million sum by their retirement dates, I believe they’ll have more than enough to live off just the interest (or dividends).

If you’re one of the over 4 Million Americans set to retire this year, you may want to pay attention.

Finding a financial advisor who puts your interest first can be the difference between a rich retirement and barely getting by, and today it’s easier than ever. SmartAsset’s free tool matches you with up to three fiduciary financial advisors that serve your area in minutes. Each advisor has been carefully vetted, and must act in your best interests. Start your search now.

Don’t waste another minute; get started right here and help your retirement dreams become a retirement reality.

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

Our expert who first called NVIDIA in 2009 is predicting 2025 will see a historic AI breakthrough.

You can follow him investing $500,000 of his own money on our top AI stocks for free.