The last 30 years have seen tremendous innovations, discoveries, creations, and strides made in medicine, technology, finance, and communications. The Baby Boomer generation has endured 4 major wars, the creation of satellites and space travel, the only foreign terrorist attack to kill thousands of Americans on US soil, social upheaval, and an ever-changing cultural society. They have also seen the creation of television, the internet, mobile phones, cancer drugs, prosthetics, and all other types of wonders that were only considered science fiction during the post-WWII era when many Baby Boomers spent their childhoods and adolescence.

As we near the start of the 21st Century’s second quarter, we can assess how assumptions and attitudes have had to change. A number of long-held beliefs that have been debunked, such as the safety of tobacco smoking and the food pyramid advocating a heavier carbohydrate ratio over protein to reduce obesity, have forced millions to revise their lifestyle health habits. This has led other industries to re-examine and alter their own policies and practices accordingly.

Old Dogs and New Tricks For Retirement

Baby Boomers whose retirement savings are being managed under assumptions developed during the Reagan, Bush or even Clinton administration years may find themseves in a shortfall in the modern era, due to inflation, longer lifespans, and government agency insolvency.

There are several retirement shibboleths that far too many Baby Boomers on the edge of retirement still believe, much to their own detriment. Inflation, market volatility, taxes, and a panoply of other factors have changed both the playing field and the rulebook, but many Boomers and their advisors still haven’t read it.

Old Dogs:

Here are a few former principles that are no longer valid in today’s economic climate.

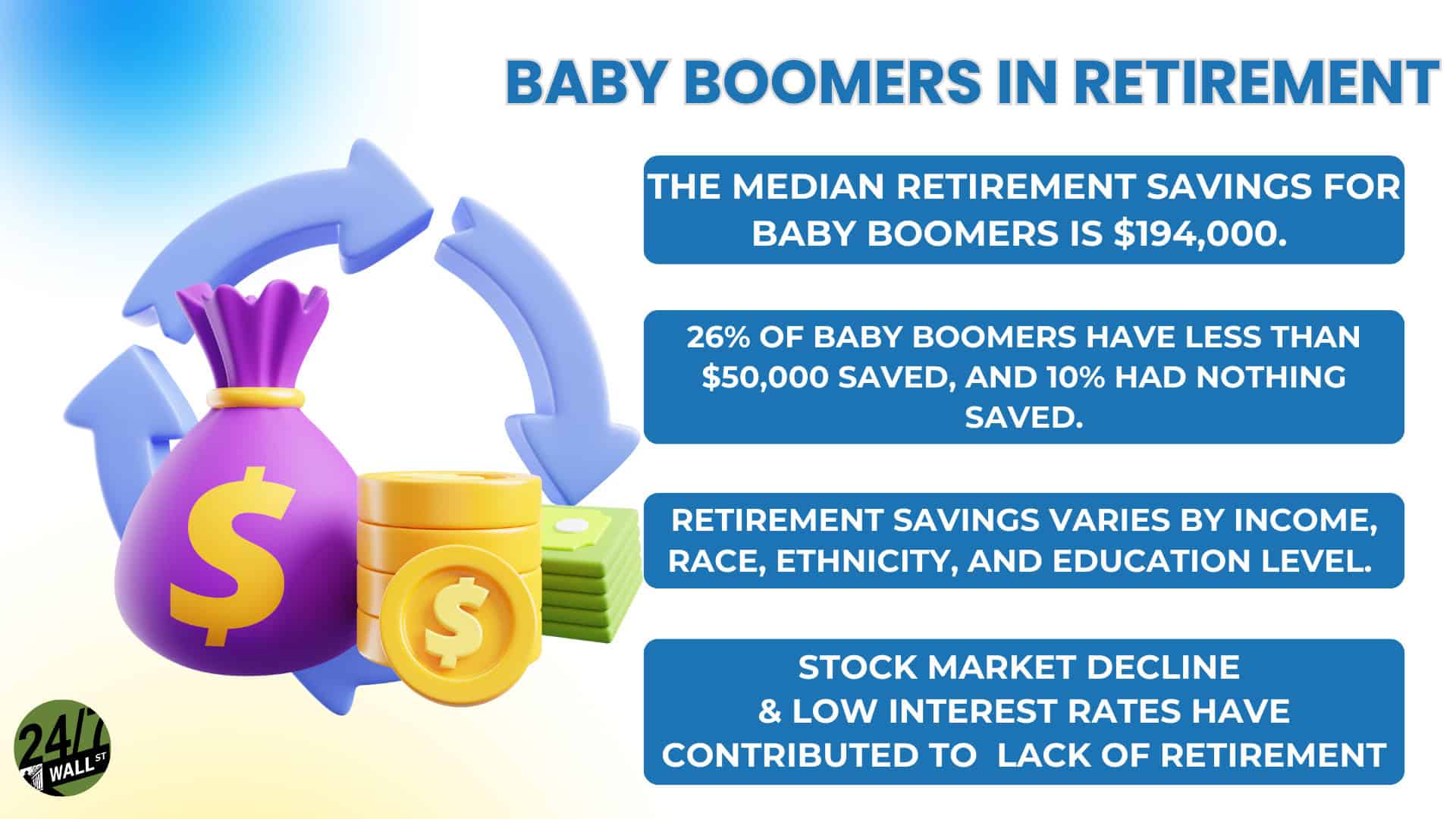

The 4% Retirement Rule – This notion came about as a result of the Reagan low tax growth period during the 1980s. It assumed a 30-year retirement and that the inflation of the Carter years would never return. It also did not anticipate the trillions of dollars of national debt that would be accrued in the subsequent decades. Baby boomers are now often living well past their 80s. Inflation came back ferociously during the Biden administration, and the volatility of both the stock and bond markets under the 4% rule left a lot of shortfalls for many retirement portfolios.

The Age Calculation For Stock/Bond Portfolio Holdings – Another obsolete financial management practice was to subtract one’s age from 100 to determine the percentage of stocks vs. bonds that should be held in one’s retirement portfolio. (Ex: a 65-year-old should hold 35% stocks and 65% bonds. A 75-year-old should hold 25% stocks and 75% bonds). Again, this was a ratio predicated on the notion that the financial environment during the Regan era would not change. It also assumed a cookie-cutter approach towards risk tolerance, History has proven both of these assumptions to be way off base.

Over Reliance On Medicare and Social Security to Determine Retirement Age – many have long assumed that Medicare’s age 65 eligibility and Social Security’s age 62 eligibility minimums were inviolate and fully comprehensive. Unfortunately, rampant overspending by Congress has put the integrity and solvency of both programs into jeopardy for those planning to make claims in the next decade, and current recipients are looking at potential service and payment size cutbacks.

Retirees Must Be Completely Debt Free Before Retirement – while carrying as little debt as possible is an optimal goal, manageable debt should not be paid off with tax-deferred retirement money for a number of reasons that may involve reduced portfolio appreciation rates, tax penalties, and other downsides.

New Tricks:

There are a number of contemporary strategies that can be deployed to address the current and constantly shifting economic landscape that has some built-in flexibility for adjustments as warranted.

Health Savings Accounts – Signed into law by President Bush in 2003, the HSA is a tax-free separate savings account exclusively for long-term care needs that are outside the scope of Medicare coverage. As one cannot contribute to an HSA once they receive Medicare benefits, it behooves those who are still earning to take an additional portion of their salary to contribute to the HSA accounts. There are no capital gains or withdrawal taxes, and given the longer average lifespans, may become indispensable in the wake of potential Medicare cutbacks. Kiplinger’s advises HSA accounts and separate other emergency long-term care accounts as a major priority, due to concerns over the insufficiency of Medicare coverage and its looming insolvency.

Fixed Index Annuities – As the need for guaranteed income becomes increasingly urgent, Fixed Index Annuities (FIA) have become a useful and utilitarian tool to complement 401-Ks, IRAs, and Social Security benefits. The FIA is tied to one or more stock market indices and rides its growth trends accordingly on the upside. Income increases correspondingly. If the indices pull back, there is an Accumulated Value safety valve that prevents the FIA against market decreases. Annuity specialist Athene has a number of annuity configurations, including FIAs.

Portfolio Diversification – A great many retirement portfolio accounts are set up in a cookie-cutter manner with S&P 500 Index ETFs or Mutual Funds for equity and US Treasuries or equivalent mutual funds for the debt portion. This means that the portfolios are often missing out on opportunities available from international markets, and specific sectors, such as the tech stocks of the “Magnificent 7” (Amazon, Alphabet/Google, Apple, Microsoft, Mega/Facebook, Nvidia, and Tesla).

Inflation Hedges – Portfolios containing commodities, real estate, and precious metals have historically received solid inflation protection. The gargantuan $36 trillion and growing national debt will continue to be an inflation threat until the GDP growth and spending cut agendas under the incoming Trump administration can be implemented and take effect. ETFs, Mutual Funds, or direct stock holdings in companies that deal in commodities like oil, food, electricity, gold, and silver mining, are worth consideration as portfolio additions. Additionally, REITs can offer real estate exposure without the headaches and responsibilities of brick-and-mortar real estate property management and offer upside growth and regular rental income stream benefits.

Debt Management – while reducing credit card or other high-interest debt is important, inordinate preoccupation with debt to the extent of using retirement funds can often be to the retiree’s detriment. Early withdrawals before retirement age are subject to penalties, as well as taxation at one’s current tax bracket. Additionally, the gain that the portfolio could generate with those funds, tax-deferred, might easily outstrip the interest charged on the debt, so these are elements that should be evaluated prior to any hasty decisions.

Retirement Account Contribution Maximization – Familiarization with tax laws is essential for organizing the various retirement accounts for future retirement withdrawals. Attention should be paid to maximizing contributions in IRA, 401-K, HSA, and 529 (education) accounts by utilizing any employer-matching contributions. Switching to Roth IRA and Roth 401-K accounts entails paying tax at the time of the switch with tax-free withdrawals afterward, where additional growth would have presumably enlarged the account even more.

Tax Planning for Retirement When withdrawal time comes, it is important to try to stay in as low a tax bracket as possible to minimize tax bites. Additionally, Roth IRAs or 401-K accounts, which have already paid taxes, should be the first from which withdrawals should be targeted. Tax-deferred IRAs and 401-Ks should be allowed to continue to grow, untouched, if possible, under Required Minimum Withdrawal rules kick in at age 72.

Other Retirement Income: If the retiree has passive income from real estate rental properties or other holdings that are listed under Form 1099, making a business out of a hobby can generate additional tax deductions, which are often pooled together under 1099, unless large enough to require itemization. If the new business can create a profit in 2 out of 5 years, the IRS will continue to allow it.

It’s Your Money, Your Future—Own It (sponsor)

Retirement can be daunting, but it doesn’t need to be.

Imagine having an expert in your corner to help you with your financial goals. Someone to help you determine if you’re ahead, behind, or right on track. With SmartAsset, that’s not just a dream—it’s reality. This free tool connects you with pre-screened financial advisors who work in your best interests. It’s quick, it’s easy, so take the leap today and start planning smarter!

Don’t waste another minute; get started right here and help your retirement dreams become a retirement reality.