Personal Finance

I'm 47 with $4.6 million in the bank and I still tend bar once a week - how much cash should I keep on-hand?

Published:

Last Updated:

Key Points from 24/7:

Once you’re financially independent, the question of how to manage your cash becomes the name of the game. One Redditor was wondering how much emergency cash she should have on hand in the case of an emergency.

With $4.6 million in investable assets, no mortgage, and annual expenses of $100,000, this 47-year-old FIRE retiree keeps a mix of cold hard cash, checking account reserves, and available credit to ensure financial flexibility. However, she was wondering if anyone has a specific strategy, as her plan is a bit haphazard.

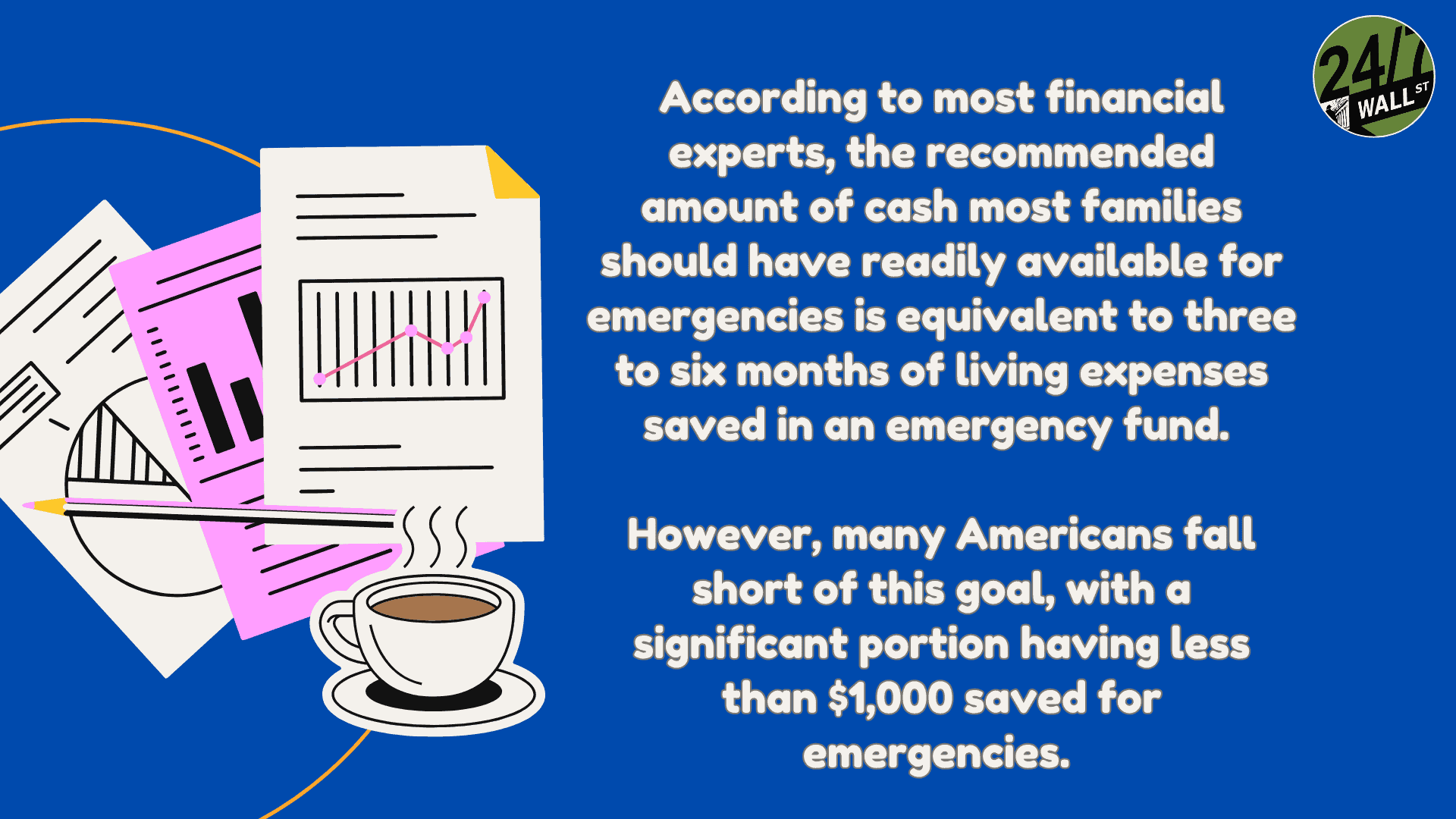

Let’s take a look at how much cash someone should have on hand. Of course, this will vary from person to person, depending on your expenses.

Here are some key considerations you need to keep in mind when building your own short-notice cash reserves:

All of that said, there are other accounts that can be successfully utilized for emergency cash. These may work alongside the options above, though we don’t recommend using them in place of physical cash and a checking account.

Organizing your emergency cash is a balancing act between accessibility and opportunity costs. Keeping a large amount of cash uninvested creates an opportunity cost. It could be earning money as an investment. However, you don’t want to have zero cash on hand, either. Here’s our suggestion:

If you’re one of the over 4 Million Americans set to retire this year, you may want to pay attention.

Finding a financial advisor who puts your interest first can be the difference between a rich retirement and barely getting by, and today it’s easier than ever. SmartAsset’s free tool matches you with up to three fiduciary financial advisors that serve your area in minutes. Each advisor has been carefully vetted, and must act in your best interests. Start your search now.

Don’t waste another minute; get started right here and help your retirement dreams become a retirement reality.

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

Our expert who first called NVIDIA in 2009 is predicting 2025 will see a historic AI breakthrough.

You can follow him investing $500,000 of his own money on our top AI stocks for free.