Personal Finance

I'm about to turn 60 and have socked away $800k in my 401(k) - is it safe to move my targeted retirement date up by a few years?

Published:

Last Updated:

I recently read a Reddit post written by a hopeful retiree who was nearing his 60th birthday. His 401K was approaching the $800K mark, but he was beginning to take a fresh look at his retirement strategy and goals.

This post is a great example of how retirement goals and strategies change. And that’s okay! It’s completely okay to change your goals and strategies, but you must do so purposefully.

Let’s use this Reddit post to look at how retirement plans can change and how to adjust to these changes:

The Reddit poster originally planned to retire at 70. However, he is now thinking about moving it up to 67. That’s a very reasonable adjustment for those planning on traveling during retirement. In fact, it’s one of the reasons we don’t recommend retiring at 70.

If you decide to retire too early, there may be some distinct disadvantages, such as penalties for drawing from your 401(k) too early. However, our poster is still planning to retire at full retirement age, so this isn’t an issue.

This should cause you to rethink your retirement horizon, though. It can be challenging to stretch the same amount of money over three extra years. You’ll need to revisit your strategy to ensure your savings last.

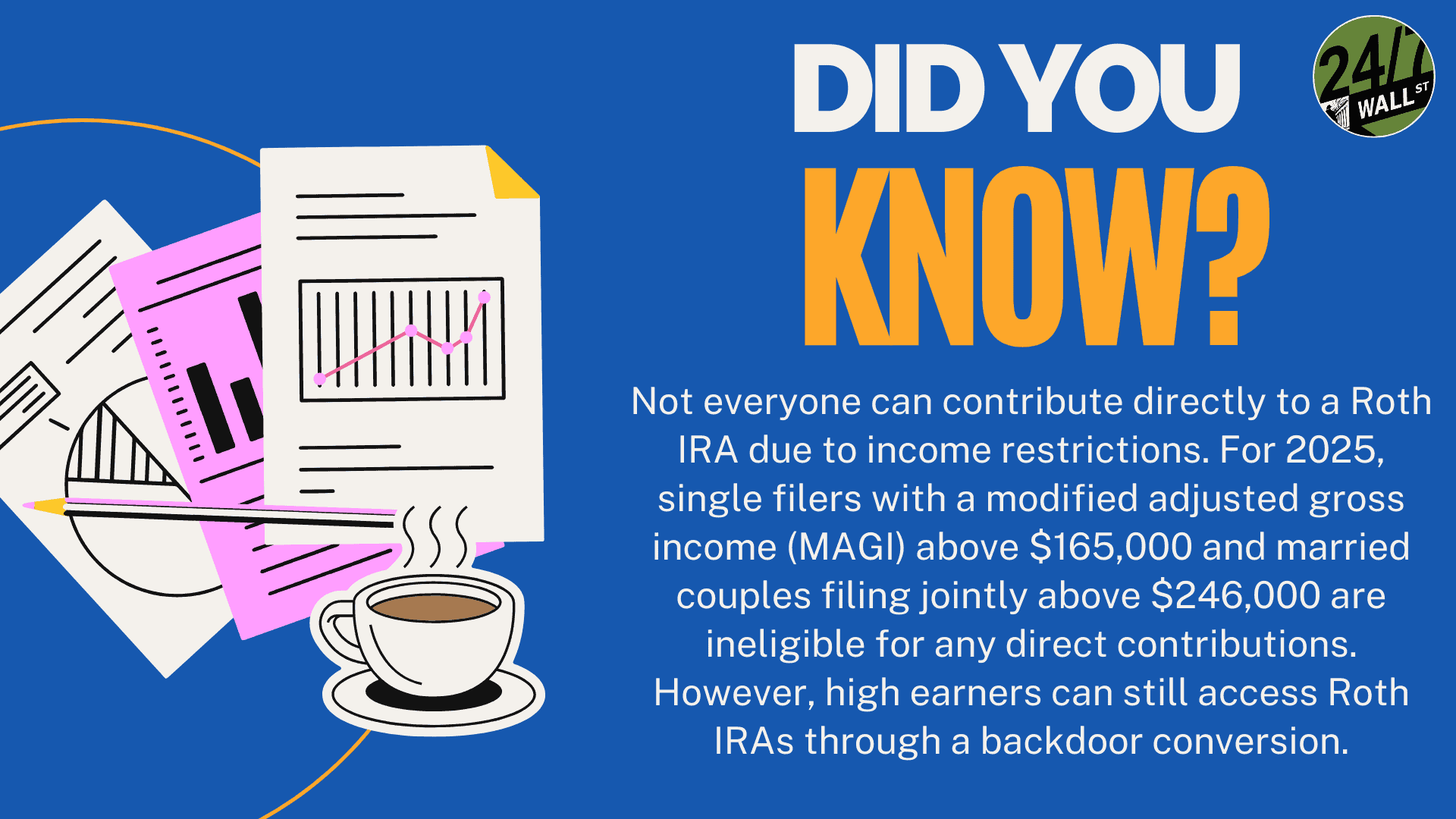

The Redditor also mentioned rolling his Roth IRA into his 401(k), which can simplify his retirement accounts. However, I wouldn’t recommend this because:

The poster has a relatively low interest rate on his mortgage, which puts him in a good position. He’s considering using his $200K lump sum pension to help pay down his $300K mortgage.

While getting out of debt is generally a good thing, mortgages are a little bit different (especially very low-interest mortgages). Often, the money can be invested elsewhere for a higher return than you would save on interest.

Paying down the mortgage also limits flexibility. Once the money is put into the mortgage, you cannot easily get it back out. In the case of unexpected expenses, it may be better to put it in a high-interest savings account.

House repairs are one of these expected costs, as the poster mentioned. But even if home repairs aren’t a concern, I wouldn’t recommend paying down a low-interest mortgage in most cases.

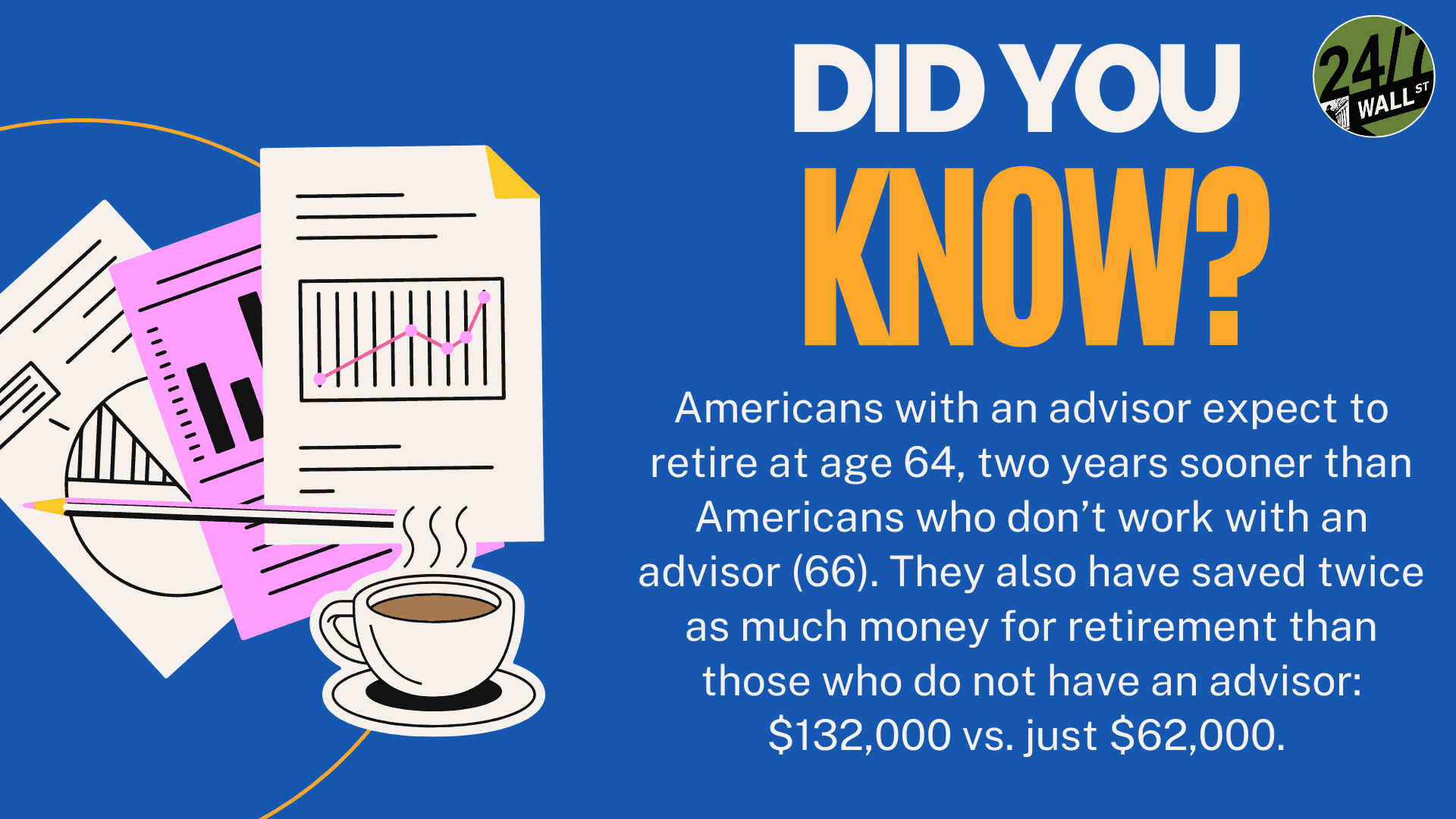

Remember, the only person who can give you financial advice is someone who knows your situation personally. In complex situations, it’s often best to invest in a financial planner who can help you:

Changing your retirement plan is never a bad thing, but you should do it with a complete understanding of how it will affect your goals.

Retirement planning doesn’t have to feel overwhelming. The key is finding expert guidance—and SmartAsset’s simple quiz makes it easier than ever for you to connect with a vetted financial advisor.

Here’s how it works:

Why wait? Start building the retirement you’ve always dreamed of. Click here to get started today!

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

Our expert who first called NVIDIA in 2009 is predicting 2025 will see a historic AI breakthrough.

You can follow him investing $500,000 of his own money on our top AI stocks for free.