Personal Finance

This Is Exactly How the IRS Determines Your RMD

Published:

Last Updated:

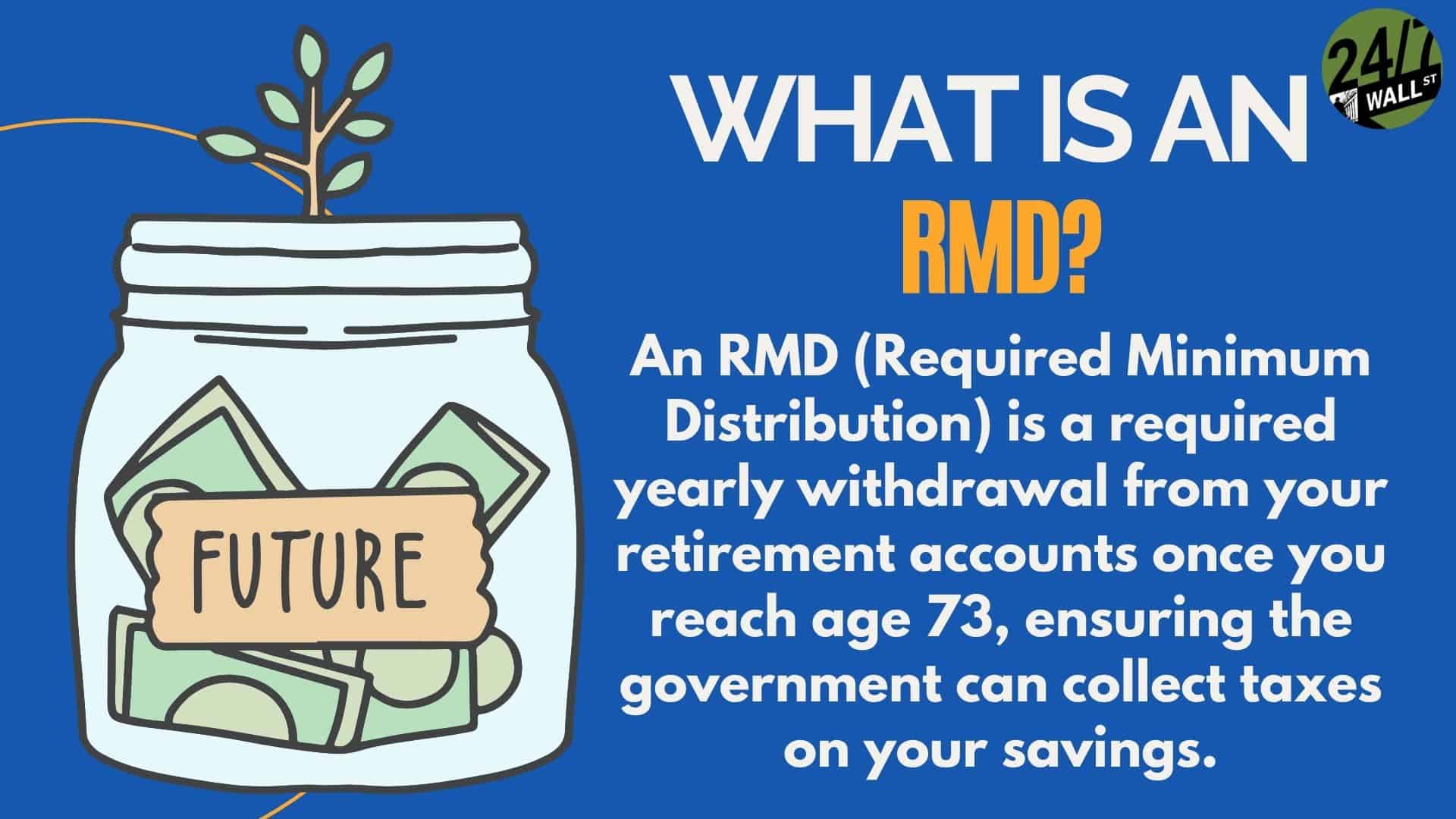

Once you reach the age of 73, you’re legally required to take your Required Minimum Distributions (RMDs), ensuring the government can collect taxes on your money.

If you’re already above 73, or are nearing that age, it’s very important to know how to calculate your required minimum distribution – which you should also review with a financial advisor.

To calculate your RMD, the IRS will use a formula that includes your total account balances, your age, your life expectancy, and your beneficiary life expectancies.

The IRS then divides the total balance by your life expectancy factor. That’s the age to which you’re expected to live until. For an example of how that works, here’s a link to the IRS Uniform Lifetime Table.

Let’s say you’re 73 years old. You would have a Life Expectancy Factor of 26.5. If you have an account balance of $250,000 as of December 31 of last year, you would divide $250,000 by 26.5, which would give you an RMD distribution amount of $9,433.96.

According to the IRS, “The RMD rules apply to all employer-sponsored retirement plans, including profit-sharing plans, 401(k) plans, 403(b) plans, and 457(b) plans. The RMD rules also apply to traditional IRAs and IRA-based plans such as SEPs, SARSEPs, and SIMPLE IRAs. The RMD rules do not apply to Roth IRAs or Designated Roth accounts while the owner is alive. However, RMD rules do apply to the beneficiaries of Roth IRA and Designated Roth accounts.”

With an IRA, you must calculate RMD for each IRA separately. You can combine the RMDs for all of your IRAs and withdraw the total amount from a single IRA.

With a defined contribution plan, such as a 401(k), you are required to take separate RMDs for each plan. With a Roth IRA, you do not have to take RMDs if you are the original account holder. However, beneficiaries of a Roth IRA are subject to RMDs.

In addition, if you have a spouse who is 10 years younger than you, and is listed as a 100% beneficiary of your RMD, you need to calculate your RMD using a Joint Life Expectancy Table. The calculation includes your age and your spouse’s age, which can result in longer life expectancy, which can also reduce your required RMD. It’s another way for the IRS to make your life even more fun.

One, at 73, you are required to take your RMD. That will go up to 75 by 2033.

Two, there is a required beginning date, which is April 1 of the year after the year when you turn 73. So, if I turn 73 in 2025, I would have until April 1, 2026 to take my first RMD, which would cover my RMD for 2025. I would also have to take another RMD by year-end to account for my 2026 RMD as well.

Three, if you do not take your RMD in time, you could see penalties of up to 25% of the outstanding RMD you had to take. It was once as high as 50%.

It ensures the IRS gets its money one way or another.

Four, make sure you don’t get caught up in an RMD pitfall. For example, make sure you’re using the correct account balance. The wrong balance can lead to an RMD that’s too low. You also want to make sure you’re using the correct life expectancy factor, as we noted a moment ago. And you want to make sure that you’re accounting for all retirement accounts.

Five, before you start with an RMD, visit with your financial advisor.

The last thing you want to do is calculate the RMD incorrectly, use the wrong life expectancy factor, or take a lower RMD than expected. All can lead to unnecessary calls from the IRS.

Retirement planning doesn’t have to feel overwhelming. The key is finding expert guidance—and SmartAsset’s simple quiz makes it easier than ever for you to connect with a vetted financial advisor.

Here’s how it works:

Why wait? Start building the retirement you’ve always dreamed of. Click here to get started today!

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

Our expert who first called NVIDIA in 2009 is predicting 2025 will see a historic AI breakthrough.

You can follow him investing $500,000 of his own money on our top AI stocks for free.