Personal Finance

Forget the 4% Rule. Here's the Withdrawal Rate I'm Planning On

Published:

The 4% rule has long been the gold standard for retirement plan withdrawals.

The rule fell out of favor for a while but is more valid in today’s interest rate environment.

The rule is not only a big aggressive for me, but flawed in other ways.

The right cash back credit card can earn you hundreds, or thousands of dollars a year for free. Our top pick pays up to 5% cash back, a $200 bonus on top, and $0 annual fee. Click here to apply now (Sponsor)

I’m working hard to build retirement savings for a few reasons. First, I’m well aware that Social Security might have to cut benefits in about a decade’s time. Secondly, I know that even if Social Security doesn’t implement cuts, those benefits might only replace 40% of my paychecks or less.

After working hard my entire life, I don’t want to be pinching pennies in retirement. So I’m willing to make certain lifestyle sacrifices in the near term to build myself some savings.

But I also don’t want to blow through my savings too quickly once I decide to stop working. So to that end, I’ll need a withdrawal strategy.

However, I’m not planning to use the famous 4% rule. And you may not want to, either.

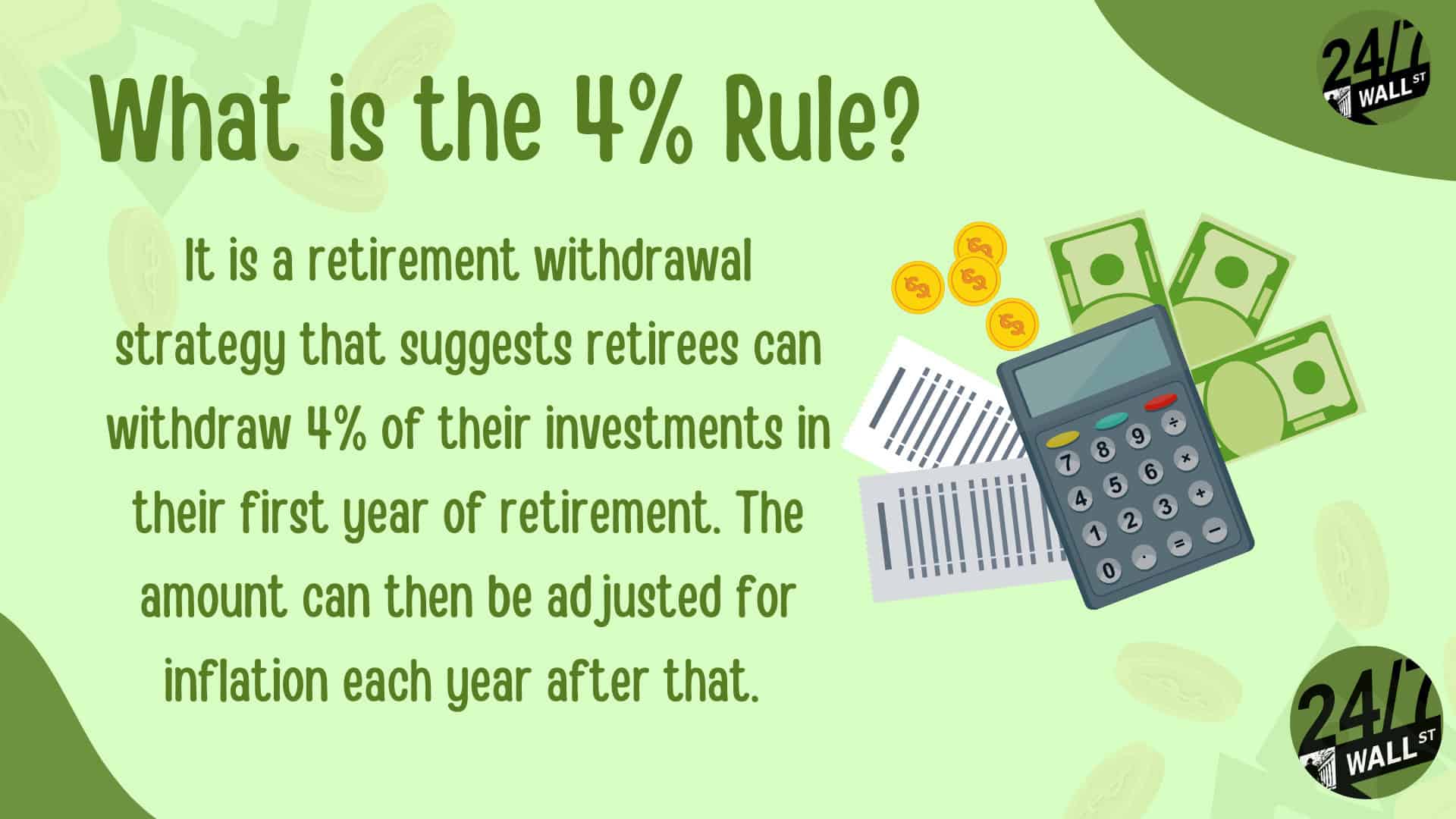

The 4% rule says that if you remove 4% of your portfolio balance your first year of retirement and then adjust future withdrawals to account for inflation, there’s a good chance your savings will last for 30 years.

But I have some big issues with the 4% rule.

First, it assumes a fairly equal mix of stocks and bonds, which you may not have in your portfolio. Secondly, it assumes your spending in retirement is fairly steady, which it may not be. And finally, it relies on generous bond yields that may or may not be available, depending on the interest rate environment at the time.

In fact, because of low interest rates, in recent years, financial experts had moved away from the 4% rule. Now, it’s back in favor because interest rates are higher. But we don’t know what the future holds as far as interest rates go.

You may be wondering what withdrawal rate I plan to use for my savings. My answer? I don’t know. But I also don’t think I’ll use the same withdrawal rate each year.

Instead, I think that rate will need to be adjusted for different circumstances. Those might include how interest rates are looking at the time, what my spending needs are, and what my portfolio mix entails.

If bond yields are lower, I may start off with a 2.5% or 3% withdrawal rate and go higher or lower depending on economic conditions and my own needs. Similarly, I may decide early on in retirement to take out 5% of my portfolio for a year or two to travel.

I want the flexibility to adjust my withdrawal rate as I need to, which is why I’m not a fan of the 4% rule. It’s just too rigid.

But I also don’t want to manage my portfolio alone. To that end, I plan to use a financial advisor. It may not be the same advisor I use now. But I want someone to consult with on such an important decision. And you may want to set yourself up with a similar resource once the time comes to start drawing down your portfolio.

Retirement can be daunting, but it doesn’t need to be.

Imagine having an expert in your corner to help you with your financial goals. Someone to help you determine if you’re ahead, behind, or right on track. With SmartAsset, that’s not just a dream—it’s reality. This free tool connects you with pre-screened financial advisors who work in your best interests. It’s quick, it’s easy, so take the leap today and start planning smarter!

Don’t waste another minute; get started right here and help your retirement dreams become a retirement reality.

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

Our expert who first called NVIDIA in 2009 is predicting 2025 will see a historic AI breakthrough.

You can follow him investing $500,000 of his own money on our top AI stocks for free.