Baby Boomers are stepping into retirement, but for many, it may not be the peaceful chapter they imagined. Too many Boomers are falling into financial habits that can quietly snowball into big trouble down the road.

These are three major pitfalls that could leave retirees facing a painful financial disaster later in life.

1. Their work plans aren’t realistic

A major mistake many Boomers are making is assuming they will be able to work far longer than most people actually do.

The Transamerica Center for Retirement Studies reports that 56 percent of Boomers expect to stay on the job until at least age 70 or skip retirement entirely. It sounds like a smart strategy in theory, but real life often tells a different story.

Empower data shows that the average retirement age is 65 for men and 63 for women. In many cases, people exit the workforce earlier than they planned because they have no choice. Health problems, a family member who needs care, or an unexpected job loss can all force someone out of work long before they hoped.

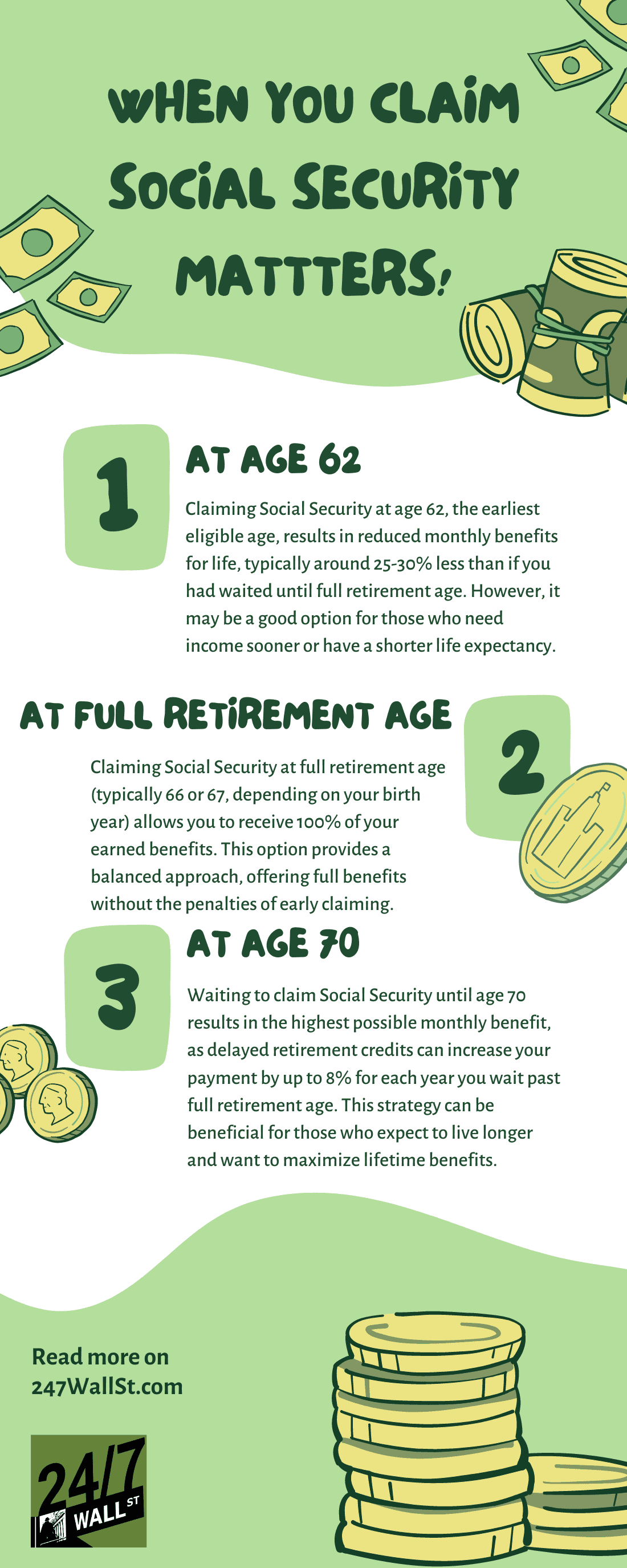

When you plan for income until 70 but retire years earlier, the impact on your finances can be severe. Your savings may not have time to grow and you may feel pressure to claim Social Security early, which permanently reduces your benefit.

2. They’re anticipating over-relying on Social Security

Another major issue for Boomers is their overly optimistic view of what Social Security can actually cover.

According to the Transamerica study, 43 percent of Boomers expect Social Security to be their primary income source once they retire. That is a problem, because the average retiree needs to replace 80 to 90 percent of their former income. Social Security provides roughly 40 percent for most people, and the percentage drops even lower for high earners.

If you want a comfortable retirement, you need more than government benefits. Savings, pensions, or other income sources must fill the gap, because relying only on Social Security will likely lead to a tight financial future.

3. They aren’t saving enough

Finally, the last big issue is that Boomers simply do not have enough money saved to support them, even with Social Security to help. The median retirement savings for members of this generation is $194,000. And they don’t have a lot of time left to build up this balance.

If you go into retirement with a $194,000 nest egg, that is going to produce around $7,760 in annual income. That’s assuming you follow the 4% rule, which says limiting withdrawals to 4% of your account balance should allow you to preserve your wealth. It may produce less, as some experts now suggest you should take out just 3.7% to avoid draining your account too fast as projected future returns are lower.

The bottom line is, the typical Boomer simply does not have the funds to have the retirement they deserve. That’s going to become a big problem if they can’t keep working or they realize too late that Social Security isn’t enough.

If you’re a member of this generation and you have savings near the median, it’s time to realize these harsh truths and get aggressive about investing for your future. Otherwise, you could be left with big regrets.