It’s safe to say that everyone hopes to have a nice savings and retirement account by the time they turn 45. The dream should always be to retire early enough to still enjoy one’s golden years. If you can set aside $1 million by this age, it begs the question of whether you should and can retire early.

If you are part of the FIRE movement, which focuses on financial independence and early retirement, any question about early retirement will focus on several factors. Specifically, with $1 million, it’ll be helpful to think about lifestyle, cost of living, and how much you can spend every year.

How Much Can You Spend?

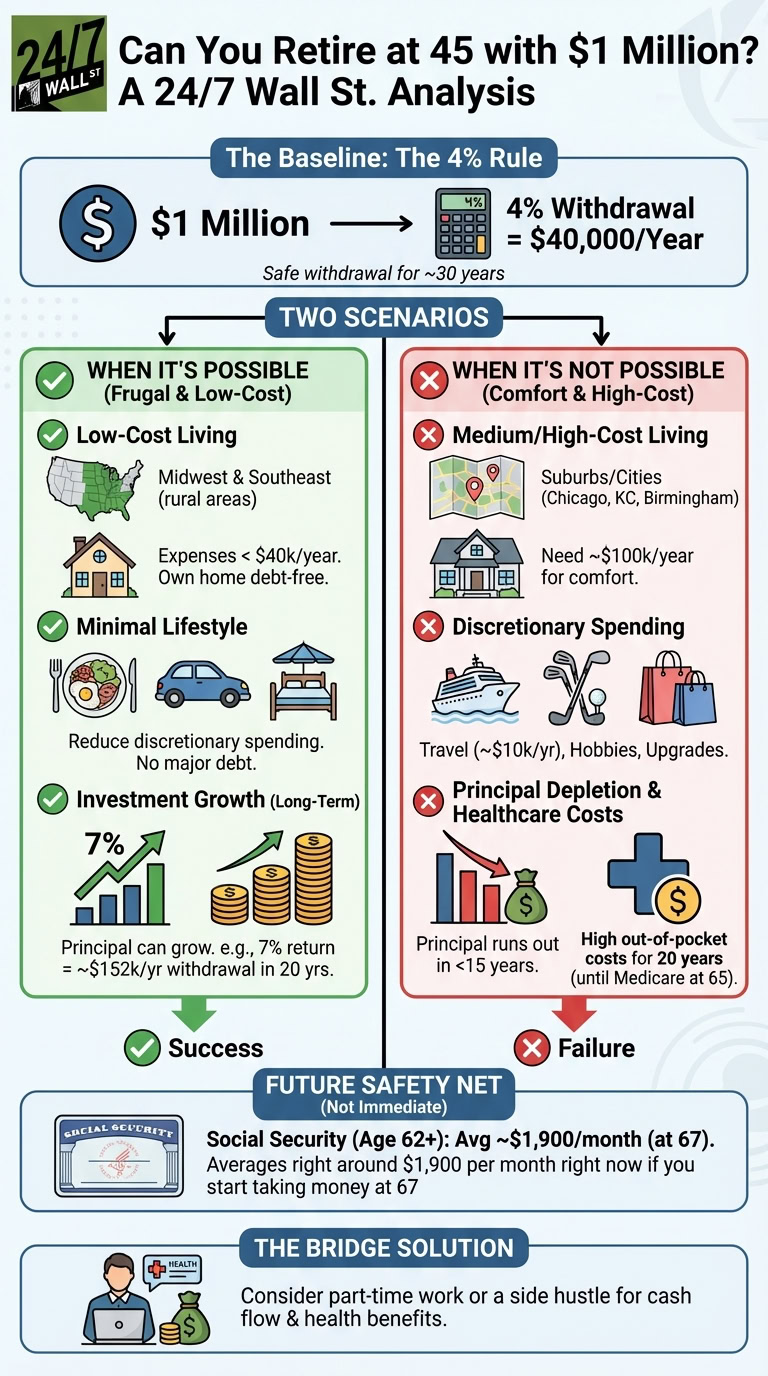

Traditionally, most people looking to retire early look at the 4% safe withdrawal rule as the baseline for whether or not it’s affordable to quit. If you take $1 million at a 4% withdrawal yearly, you are talking about $40,000 per year, for roughly the next 30 years.

This doesn’t feel all that long considering life expectancy, but you also have to remember that you can withdraw Social Security starting at age 62, which averages right around $1,900 per month right now if you start taking money at 67, otherwise known as Full Retirement Age.

Knowing that you only have around $40,000 to spend annually ahead of Social Security might make you think twice about where and how this money would allow you to retire.

How It’s Possible To Retire

First and foremost, if you want to retire on just $40,000 per year, you must consider finding a low-cost state and a low-cost-of-living area in that state. Typically, the Midwest and the Southeast, save for South Florida, have been good choices for this type of budget.

It’s not uncommon in certain places of Kansas, Iowa, and Illinois, outside of the big cities, where you can live with annual expenses of less than $40,000. The good news is that your $1 million principal is hopefully invested, so it should grow even as you withdraw. The hope is that you are making more than 4% with your investment, so as your principal grows, more money might be available.

For example, at a 7% return, $1 million can grow to just under $4 million in the next 20 years, which means you’d have around $152,000 for your retirement.

Of course, this is thinking down the road, so you want to focus on the now and reduce your lifestyle so it’s just minimal discretionary spending. This likely means you’ll be giving up on dinners out regularly, more than one vacation, and even things like a new car might be something to reconsider. You also can’t have any major outstanding debts, credit cards, or otherwise. In fact, owning your home at 45 with a $1 million nest egg will give you the best possible chance of retirement success.

When It’s Not Possible to Retire

Unfortunately, $40,000 at the 4% SWR doesn’t give you much wiggle room to upgrade from a low-cost-of-living area to even a medium-cost-of-living location. Even the suburbs of big cities like outside of Chicago, Kansas City, or even Birmingham, Alabama, are going to make it challenging to live comfortably on just $40,000 per year.

Depending on which of these cities you choose, you’re likely looking closer to $100,000 annually that you’d want to be able to withdraw to live a comfortable lifestyle. The hard truth is that if you choose this path, you’d likely run out of your $1 million in no more than 15 years, which means there is no more principal to keep growing as you spend.

Don’t forget that healthcare costs only go up as you get older, so if you have 20 years between 45 and 65 before you can apply for Medicare, you are paying out of pocket. This means over the course of 20 years, it’s not impossible to think you could be paying hundreds of thousands of dollars for private medical care.

In addition, $1 million isn’t going to be enough if you like to travel, want to have hobbies like golfing, or even just want the ability to make some comfort purchases every now and again. Annual travel can cost around $10,000 per year, which is 25% of your available safe withdrawal rate before you consider any living expenses.

If anything, you could consider part-time work or a side hustle that could help provide some additional cash flow each month and maybe even receive some health benefits.