Social Security pays benefits to roughly 70 million Americans every month, and almost every one of them is operating on at least one piece of bad information about how it works.

That’s not a small problem. The myths floating around dinner tables, news segments, and social feeds drive real decisions about when people file, how much they save, and whether they bother saving at all.

A retiree who believes the program is about to collapse claims early and locks in a 30% benefit cut for life. A worker who assumes Social Security will replace their paycheck quits saving and walks into retirement with a 40% income shortfall.

Both of those are six-figure mistakes built on something that simply isn’t true.

Below are ten of the most persistent Social Security myths — the ones that cost people money, the ones that fuel needless panic about bankruptcy, and the ones that politicians keep alive because the confusion is useful. Some you’ve almost certainly heard. One or two you may have repeated.

10. Undocumented Immigrants

This is a controversial myth, but it is an important one that is very relevant today. The belief is that undocumented immigrants are “raiding” the Social Security fund and taking money away from American citizens who should be receiving the money.

Supporting The Program

If you dig a little beneath the surface of this myth, you will discover that undocumented workers actually help the Social Security program. In 2022 alone, undocumented immigrants contributed $25.7 billion to the program, according to a July 2024 report.

9. Government Raids

This myth has been perpetuated for far too long, and while it’s primarily political, it’s still regularly featured on mainstream media programs. As it stands today, the Social Security program is centered around two trust funds that pay benefits, and the myth is that these trusts are often “raided” to pay for other government programs.

Kind Of True

Surpluses are loaned to the Treasury in exchange for securities; redeeming them requires the Treasury to raise cash (taxes/borrowing/cuts elsewhere).

8. Only For Retirement

Today, there is a very popular myth that Social Security only exists to help out the retired. While Social Security does make up the lion’s share of the benefits issued by the Social Security Administration, it’s not the only people being helped.

A Safety Net

If you are disabled or the spouse of a deceased Social Security beneficiary recipient, you also qualify for benefits. Disability benefits are a major component of the program and an often overlooked piece of the Social Security pie to provide financial support to anyone having trouble returning to the workforce.

7. No Taxes Required

A major misconception about the Social Security program is that you don’t or won’t need to pay taxes on any money you receive. Part of the reason this myth feels so widespread is that it was true, at least until 1984, when Ronald Reagan overhauled the tax provision for the program.

Yes, You Pay Taxes

As of early 2026, eight states still tax Social Security. While it is true that you won’t pay state taxes if you live outside of one of these states, federal taxes are another story. Currently, you pay taxes on 50% of your combined/provisional income if it is between $25,000 and $34,000 as an individual and $32,000 to $44,000 for a married, jointly filed couple. Anyone who exceeds this income threshold will pay taxes on up to 85% of the income you receive from the program. Your actual tax level is based on your total earnings and associated tax bracket.

6. Won’t Replace Your Income

There is a current belief that Social Security can and will replace the entirety of your income during retirement. The hope is that if you don’t have savings or a 401(k), Social Security will provide enough income to pay all of your bills.

Part Of Your Income

As the Social Security program stands today, the numbers indicate it should provide you with around 40% of beneficiaries’ pre-retirement earnings. The hope is that this is enough to help lower-wage workers, but there is no scenario in which Social Security should replace 100% of pre-retirement earnings.

5. Cost of Living Increases

Since 1975, the Social Security Administration has been trying to keep up with the rising cost of living in the United States. This increase is calculated based on a federal index of prices, which will show if the cost of living is increasing. However, the myth is that these increases are guaranteed.

No Adjustment Required

The reality is that since 1975, there have been only three years without cost-of-living increases: 2009, 2010, and 2015. This is all the evidence you need to show that any myth about a guaranteed cost-of-living increase is false.

4. Bumped Up Payments

There is a common misconception that anyone who takes their payments early, potentially when they turn 62, can “bump up” their earnings once they hit Full Retirement Age at 67. Unfortunately, this is inaccurate, and the truth is complicated.

Cancel and Restart

The real-world requirement to receive higher benefits is to cancel your current Social Security claim within the first 12 months, repay everything you have received, and then wait until you are re-eligible to file and receive larger payments. There’s also a separate concept of suspending benefits at full retirement age to earn delayed credits, but that doesn’t erase the early-claim reduction; it just increases from that point forward.

3. 35 Years of Earnings

The Social Security program determines how much money you will receive based on your highest 35 years of earnings in your lifetime. However, the myth is that your Social Security benefit is calculated only on income you earned before you turned 65, which isn’t accurate.

Any Age Works

In the case of anyone still working after they turn 65, you can use any of the years you earned as part of the top 35 years of earnings. As long as any earnings after 65 are high enough to be part of your earnings, they would be included in the calculated amount of money you would receive from Social Security.

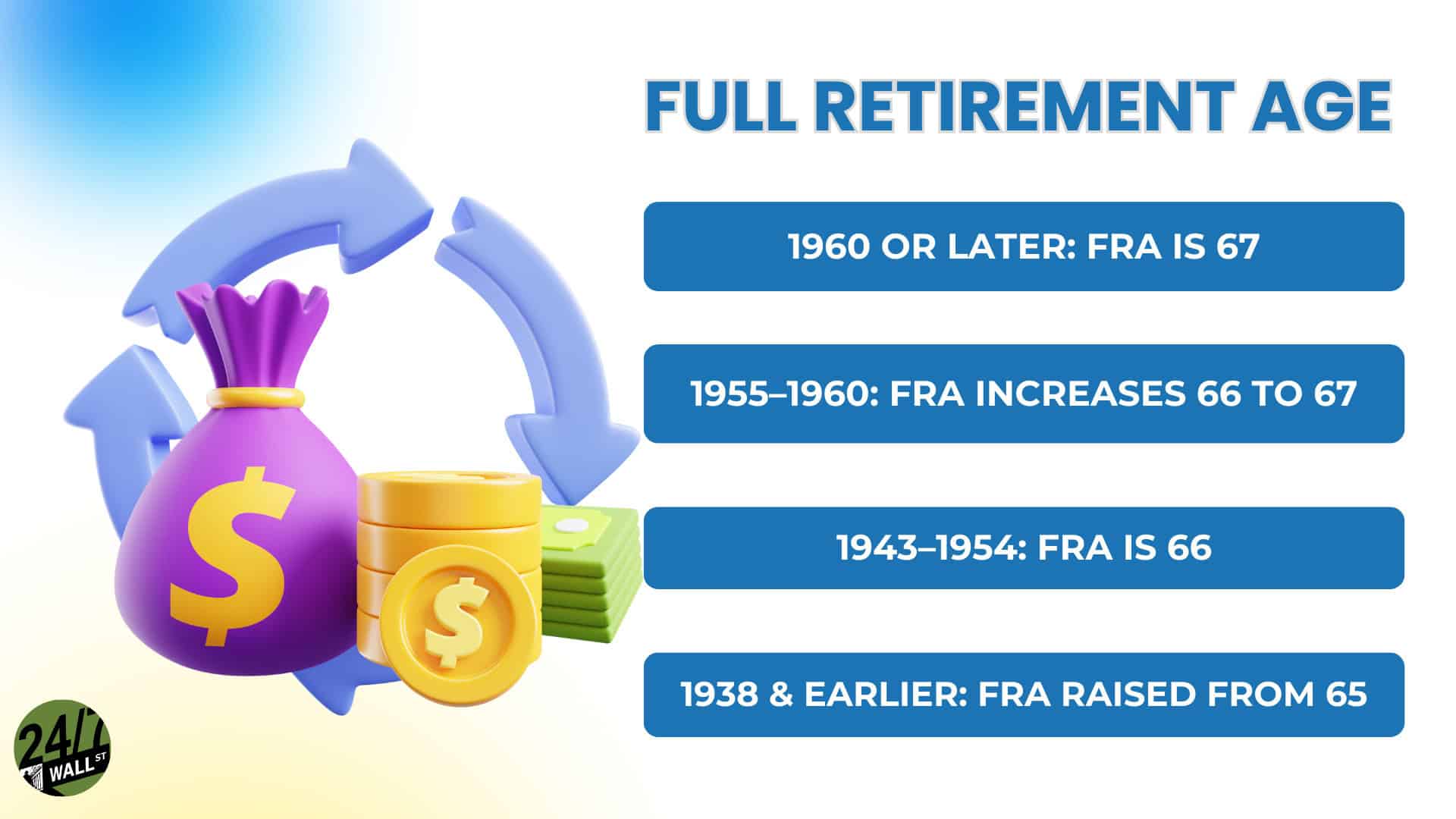

2. Benefit Claims At 62

A common misunderstanding about the Social Security program is that you must start taking benefits at age 62. Thankfully, this is a definite myth. The truth is that 62 is the earliest age you can begin drawing benefits, but it is not the only age you can start taking your benefits.

Full Retirement Age

When drawing your benefits, it should be emphasized again that 62 is the earliest age, but 67 is the recommended age. Known as Full Retirement Age, 67 is the first age you can begin taking your benefits at 100% payout, whereas taking your benefits at 62 would reduce your overall payout/income by 30%.

1. Social Security Bankruptcy

The biggest myth about Social Security is that the program is on the verge of bankruptcy. According to reports from the Social Security Administration, at 100% benefit levels, the program can only sustain its current payouts until 2035 before reducing payment benefits, potentially leaving some people without full payments.

The Financial Reality

The bottom line is that as long as people work in the United States and pay taxes to the Social Security Administration, the program will continue to be funded. The 2035 timeline and 100% benefit funding are true, but the idea that the program will be bankrupt and shut down is entirely false.