Well, the beloved inflation rates aren’t yet going through the roof if you trust the FOMC and the closely watched CPI. The Fed gave a stable inflationary outlook for 2008, along with a slower GDP and slightly higher unemployment. Of course, if you pay for healthcare, gasoline, food, and anything else volatile you will wonder about this even if you look how low the nominal CPI is before the ex-food and ex-energy Core CPI is reported.

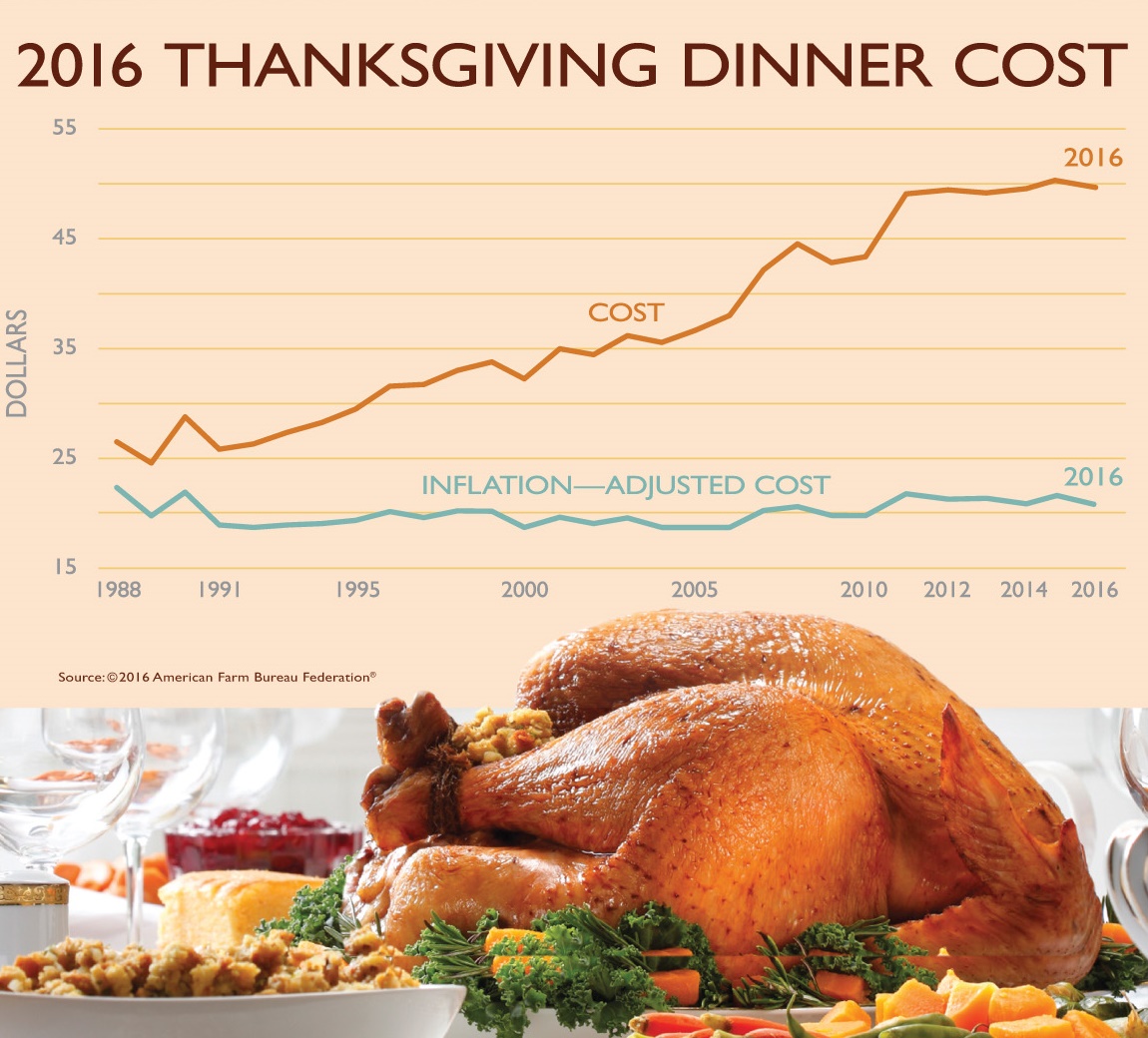

If you noticed your grocery bill while taking care of your Thanksgiving food list being significantly higher this year, you aren’t just imagining things. Thanksgiving this year is going to see a record price increase (at least recently) compared to the prior year with an estimated 11% price jump compared to last year. We started looking for some of our own calculations, but then the figures from the American Farm Bureau were readily available.

Their forecast for an average Thanksgiving meal will run $42.26 and the average price per person will cost a bit more than $4.00 per head. 24/7 Wall St. wonders how they get such a small number, but this crosses all regions and all reasonable stores from all income brackets. That is still pretty cheap, but food isn’t a one-time item. Most of us eat twice or thrice daily. High energy costs in freezing and transportation costs plus feed higher prices are all to blame. The estimated cost for a turkey is up to $1.10 per pound, $0.12 higher than in 2006. Milk, dairy, cranberries, veggies, and almost everything is higher, with the exceptions being a package of filling, relish trays, and a few other items. We don’t expect the FOMC to act on food prices alone. It isn’t even fair for the FOMC to be the savior of over-extended credit.

The Fed is in a true conundrum. Rates need to come down significantly to assist those whose mortgages are going to reset. Credit card balances are massive. But the credit squeeze negates that affect, and the truth is that the economy is in a credit bind that lower rates alone won’t cure. To top it off, if rates come down too far we are going to teeter on a true dollar crisis. A lower dollar puts the risk that U.S. will pay significantly more for imported goods. So when you see some of the economic pundits coming on the television screen calling for actually HIGHER rates, don’t be too surprised.

If you really believe the CPI numbers, well it’s Turkey Day regardless of when you read this. Cheaper credit just might not be the answer. But the conclusion here makes you want to think twice about investing in the consumer discretionary spending sector. If the house can’t be used as an equity and liquidity generator and if income isn’t going to suddenly rise rapidly rise in 2008, we’re all going to have spend less in 2008 to get out from under debt.

If you believe the latest FOMC forecasting for 2008 and beyond then you will be able to sleep well knowing that the factors at hand aren’t going to take a more major turn for the worse.

Maybe 2008 will be the year for those pesky and persistent defensive stocks. As long as the R-Word isn’t too big of an R…….

Jon C. Ogg

November 20, 2007