Economy

How Consumers Look Today as Recession Risks Become More Prominent

Published:

Last Updated:

With the endless media calls for a recession, one would think most Americans would at least be preparing for a downturn. Either the public thinks the media’s use of the term is as misused as “decimated” or the public is just sticking its head in the sand. Many issues create a solid debate about just how real a recession is and about how deep it would be, but there is still no overwhelming consensus among economists and market-watchers that a recession is already inescapable. That said, there are concerns that the public is not very well prepared for the next recession.

It takes many things to occur for people to start preparing for a recession. They have to start saving money and they have to stop or slow their spending. This then automatically sets the stage for a recession to become inevitable. With Gross domestic product (GDP) having close to 70% of its weight tied to consumer spending activities of some sort, consumers’ efforts to build up as much cash suddenly competes with the dollars used for spending.

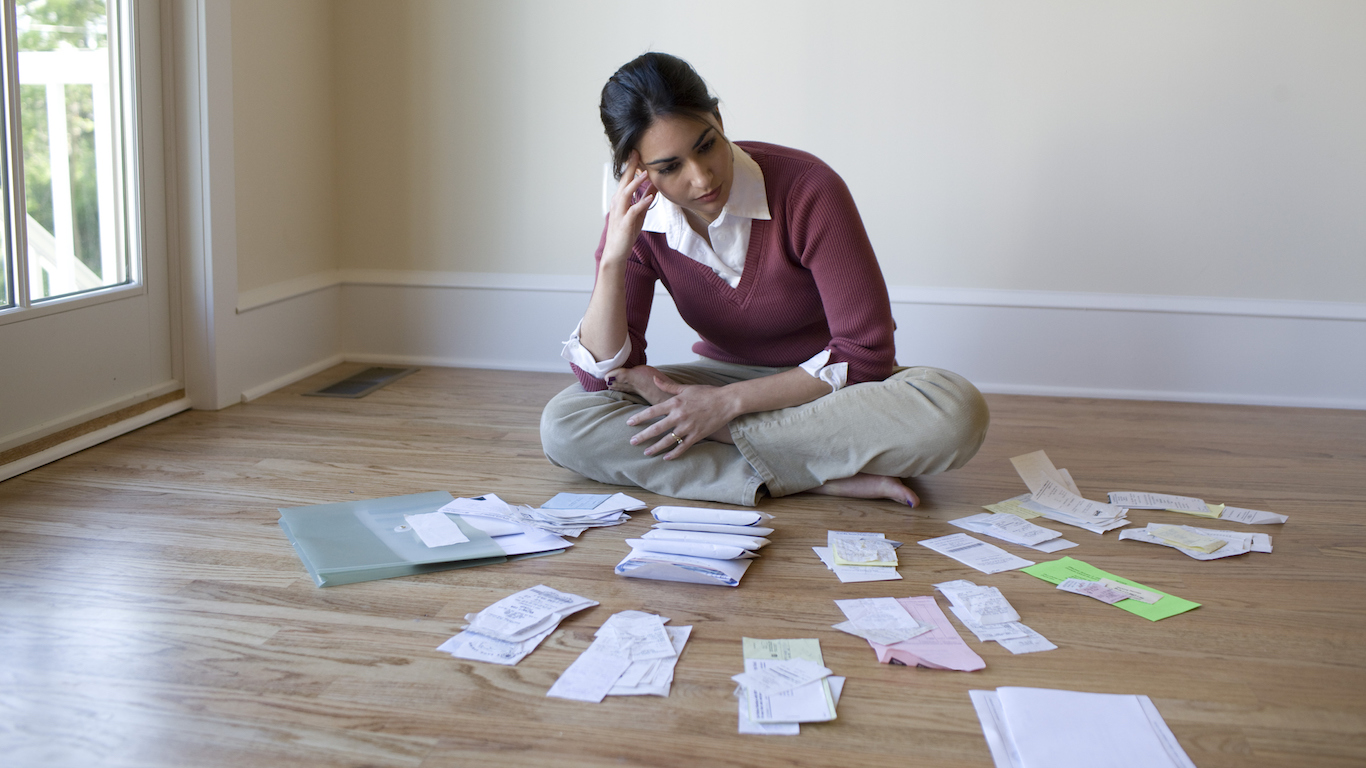

One figure frequently used is that most consumers are stretched to come with $500 to $1,000 easily. While the public is rarely able to get through even a mild recession easily, there is a concern that Joe Public might not even be that well prepared for a small economic hiccup.

24/7 Wall St. has maintained that a recession is not unavoidable at this point. While the media keeps touting “recession” headlines, the aggregate statistics about the consumer remain strong. Unemployment is exceptionally low at 3.7%, wages have risen and investments and retirement plans should be very strong at this time. Consumers remain very confident. While homeownership could be stronger, it just doesn’t look or feel like the base level of the housing market is all that stretched.

Let’s move beyond generalities and just assume that a recession is lurking and is unavoidable. At one point, no one will care if it was avoidable. They will just care that they are in the middle of it, and their spending habits will adjust whether or not it is desirable.

GDP has been shrinking, and there are views that GDP is likely to contract for the remainder of 2019. The 3.1% GDP growth in the first quarter of 2019 went down to 2.0% in the second quarter, and the Federal Reserve Bank of New York’s Nowcast was lowered to GDP growth of 1.55% for the third quarter of 2019 and that GDP growth in the fourth quarter would likely run at 1.08% (versus 1.57% just a week earlier).

A summer survey from Bankrate.com indicated that 23% of Americans (a whopping 47 million of them) who were adults when the Great Recession hit said that their overall financial situation is still worse than when the recession hit. This seems hard to imagine, but that’s their reporting. Another one in four surveyed said that they were doing roughly the same now versus at the start of the last recession. Some 51% of that same group said their financial situation is better now than it was before the recession.

Small business confidence is showing a mixed bag in overall confidence, and it is the small business segment that can add the most jobs at any given time. Two readings on this are shown below.

The National Federation of Independent Business (NFIB) Small Business Optimism index fell by 1.6 points to 103.1 in August. While still a very strong reading, fewer owners expect better business conditions and real sales volumes in the coming months, even as job creation accelerated, positive earnings trends improved and quarter-on-quarter sales gains remained strong. The report does note that the endless number of recession predictions is driving more uncertainty:

In spite of the success we continue to see on Main Street, the manic predictions of recession are having a psychological effect and creating uncertainty for small business owners throughout the country. Small business owners continue to invest, grow, and hire at historically high levels, and we see no indication of a coming recession.

MetLife recently issued its 17th annual U.S. Employee Benefit Trends Study (2019), which was given a subtitle of Thriving in the New Work-Life World. The top five sources of financial stress of employees in its survey were as follows:

While these all matter, it’s the 67% of workers who are concerned about having enough money to pay bills if someone loses their job that matters if a recession is really coming. The report said:

Nearly 2 in 3 people say they are confident in their finances, but half say they are living paycheck to paycheck, many have dipped into retirement savings, and an increasingly large group says they will have to delay their retirement because of finances.

Among IT workers, generally deemed to be in a high-paying yet somewhat economically sensitive position, 59% of those workers were said to be living off their most recent paycheck, and 69% of respondents reported that they were already planning a postponement to their retirement because of a dire financial situation.

The Federal Reserve released its most recent consumer credit trends report on September 9, showing that consumer borrowing rose by $23.3 billion in July after having risen $13.8 billion in June. This was said to be the largest monthly gain since the $29 billion increase from November of 2017 and the category covering auto loans and student loans also rose handily along with a $10 billion gain in credit card debt to $1.08 trillion.

Fresh data from the Census covering income, poverty and health insurance coverage had some ill omens in the report, but in fairness it was looking back at 2018 versus 2017. It had some data that is not dire but definitely not strong either. The median U.S. household income of $63,179 was not statistically different (up 0.88%) from the 2017 median of $62,626, even as the official poverty rate of 11.8% was a decrease of 0.5 percentage points from 2017. The rate and number of people without health insurance increased from 7.9%, or 25.6 million, in 2017 to 8.5%, or 27.5 million, in 2018.

The Census data from 2018 might be challenged by other reports that have come in since. The monthly Bureau of Economic Analysis (BEA) data showed that personal income increased by 4.5% in all of 2018, versus an increase of 4.4% in 2017. That said, the measurement of personal income also includes gains in personal dividend income, employee compensation and even farm proprietors’ income.

While 2018 numbers are looking backward, the Census also reported that the percentage of people with health insurance coverage for all or part of 2018 was 91.5%, versus the 92.1% rate in 2017. Between 2017 and 2018, the percentage of people with public coverage decreased 0.4 percentage points and the percentage of those with private coverage did not statistically change.

The most recent data on personal income and spending was released on August 30, and it measured July of 2019. That report indicated that total employee compensation was already up over 3.7% in July from the end of 2018, and the wages and salaries were also up 3.9% from the end of 2018. The BEA also showed that the personal saving rate, which is personal saving as a percentage of disposable personal income, was 7.7% in July.

On September 10, CoreLogic’s monthly Loan Performance Insights Report showed that 4% of mortgages on a national basis were in some stage of delinquency (30 days and higher, including those in foreclosure) in June 2019. While this may be higher than the trough, it is a 0.3 percentage-point drop from the 4.3% rate in June 2018, but the rate of early-stage delinquencies (30 to 59 days past due) at 2.1% was up from the 2.0% rate in June 2018. Measuring early-stage delinquency rates is important for analyzing the health of the mortgage market. Still, June’s serious delinquency rate of 1.3% was said to be the lowest for the month of June since 2005.

One issue that has to be tracked is auto loan delinquencies. A September 11, 2019, report from Credit Union Insight suggests that auto loan delinquencies are the highest level in the past decade. Along with the “peak auto” trends of 2017 to 2018, the report showed that 2018 was a year loaded with high levels of newly originated auto loans and leases (some $584 billion), and by the end of 2018 there were over 7 million Americans who were at 90 days or more in loan delinquencies. In car loans, Experian noted on September 5 that a record percentage of prime borrowers are choosing used vehicles as loan terms have reached a new high and new vehicle loan amounts remain above $32,000.

Overall, consumer credit scores are running at all-time highs. A FICO report from September showed that the all-time high of 706 is 20 points higher than the peak in the last decade. FICO data also showed that credit card account delinquencies of 90 or more days was down by 62% and overall credit card utilization is down by 28%.

Student loan debt has continued to rise in America. This competes directly with an ability to save, as well as competing with an ability to spend. The Federal Reserve data showed that student loan debt was $1.606 trillion as of June 2019. That’s up from $1.568 trillion at the end of 2018 and from $1.49 trillion at the end of 2017. In 2014, it was just $1.236 trillion.

Credit card companies are handing out rewards and benefits to win the best customers. A good cash back card can be worth thousands of dollars a year in free money, not to mention other perks like travel, insurance, and access to fancy lounges. See our top picks for the best credit cards today. You won’t want to miss some of these offers.

Flywheel Publishing has partnered with CardRatings for our coverage of credit card products. Flywheel Publishing and CardRatings may receive a commission from card issuers.

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.

24/7 Wall St.

24/7 Wall St. 24/7 Wall St.

24/7 Wall St.