Live: Here’s Why Hims & Hers (HIMS) Is Down 10% After Earnings

Key Points

-

The moment Hims & Hers reports we’ll have live updates with news and analysis updating below. You don’t have to do anything, just leave this page open and new updates will appear directly below.

-

Here are the key figures to watch the moment earnings hit.

Wall Street expects:

- Revenue: $552.05 million

- Adjusted EPS: $.23

-

Management raised FY guidance in Q1; upside to EBITDA or member growth could re-rate valuation further

Live Updates

Conference Cal Starts in 10 Minutes

We’ll post a summary of the call later. Simply leave this page open and if you check later a new update with our thoughts will appear after the call!

Looks Like Hims & Hers Will Be Down About 9%

Hims & Hers is trading down 9% pretty consistently for the past 20 minutes.

Will that change before tomorrow morning? There are two big factors:

1.) What will Wall Street say?

2.) What will the company say on its earnings call?

Their call begins at 5 p.m. ET and you can listen in here.

Here's Everything Hims & Hers Reported

HIMS | Hims & Hers Q2’25 Earnings Highlights:

- Adj. EPS: $0.17 ✅; UP +183% YoY

- Revenue: $545M [✅]; UP +73% YoY

- Net Income: $43M [✅]; UP +220% YoY

- Adj. EBITDA: $82M [✅]; UP +109% YoY

- Subscribers: 2.4M [✅]; UP +31% YoY

- Monthly Online Revenue per Avg. Subscriber: $74 [✅]; UP +30% YoY

Outlook:

- Revenue: $2.3B to $2.4B [✅]

- The company expects to leverage its specialty-specific marketing efforts to drive growth in both new and tenured categories.

- Continued investment in automation and pharmacy infrastructure is anticipated to support operational efficiency.

Q2 Segment Performance:

- Online Revenue: $537M [✅]; UP +75% YoY

- Wholesale Revenue: $8M [❌]; DOWN -10% YoY

Other Key Q2 Metrics:

- Adj. Operating Income: $26.7M [✅]; UP +142% YoY

- Adj. Operating Expenses: $389.5M [✅]; UP +58% YoY

- Free Cash Flow: $(69)M; DOWN -244% YoY

- Effective Tax Rate: 29.4% (vs. -0.9% YoY)

- Gross Margin: 76% [✅]; DOWN -500 bps YoY

CEO Commentary:

- Andrew Dudum: “Our second quarter results marked healthy progress against making personalized healthcare experiences a reality for millions of customers. We ended the quarter with over 2.4 million subscribers, a year-over-year increase of 31%. This steady adoption allowed us to drive revenue growth of more than 70% while also more than doubling Adjusted EBITDA relative to the prior year.”

Strategic Updates:

- The company is entering the next phase of its platform, moving beyond simply connecting customers to providers, to delivering access to truly personalized care.

- Recent acquisition of ZAVA Global expands Hims & Hers’ presence in Europe, with plans to drive at least $50 million of revenue from ZAVA through the remainder of the year.

- New capabilities like lab testing are expected to enhance the platform’s offerings and improve customer experience.

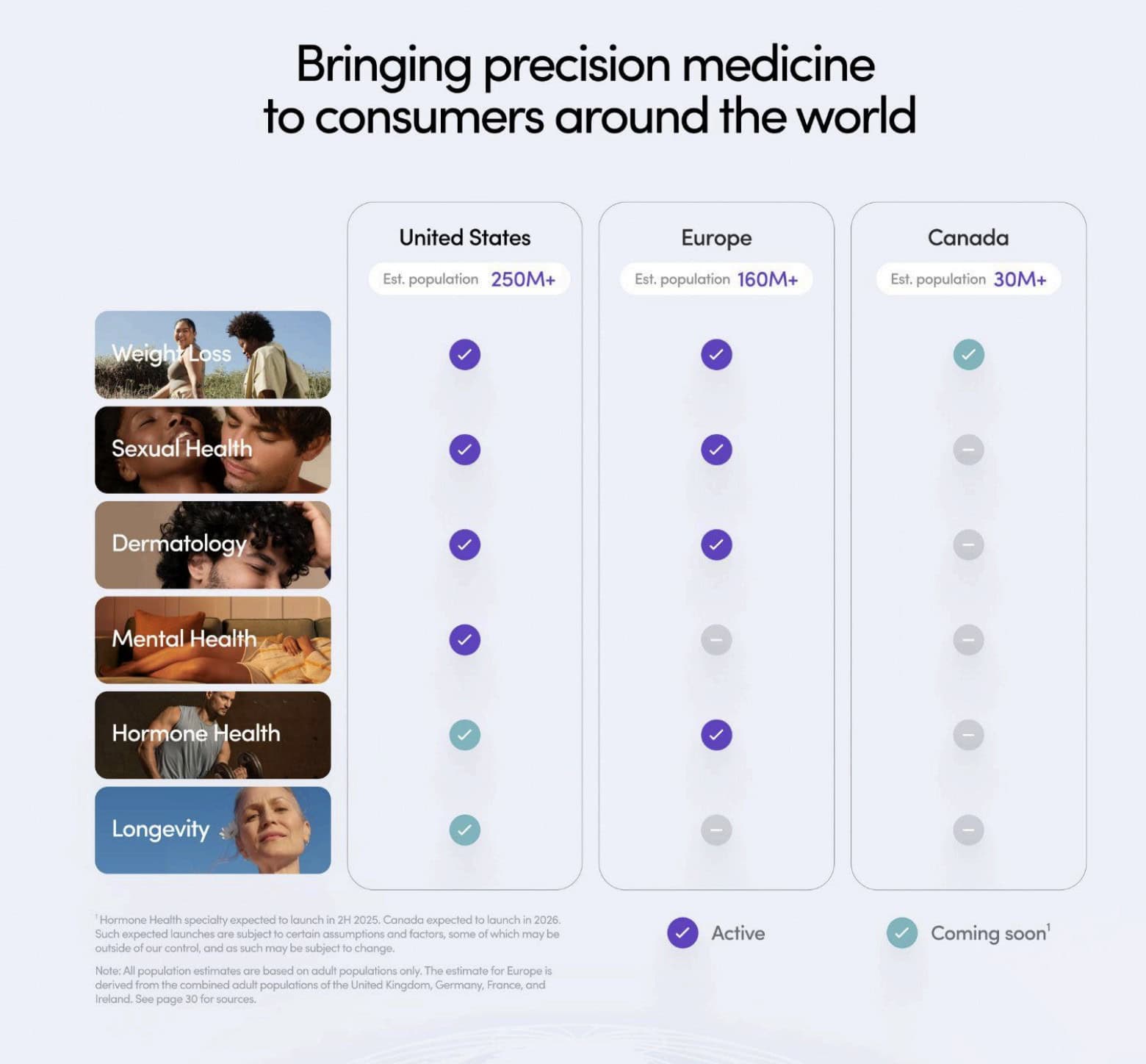

Looking Ahead

Here are some upcoming catalysts for Hims & Hers to continue seeing strong revenue growth in the coming quarters:

- Longevity and hormone health products listed as coming to the United States soon

- Weight loss listed as coming to Canada soon.

Shares are Now Down 9.25%

We are now 8 minutes past Hims & Hers earnings being released and shares have rebounded slightly, but are still down 9.25%

Forward Guidance

Here’s what Hims & Hers had to say about forward guidance:

For the third quarter 2025, we expect:

- Revenue of $570 million to $590 million.

- Adjusted EBITDA of $60 million to $70 million, reflecting an Adjusted EBITDA margin of 11% to 12%.

For the full year 2025, we expect:

- Revenue of $2.3 billion to $2.4 billion.

- Adjusted EBITDA of $295 million to $335 million, reflecting an Adjusted EBITDA margin of 13% to 14%.

The b0ttom line: At the midpoint that’s $580 million and Wall Street expected $584 million next quarter. Also, there was no raise of full year revenue.

Earnings Beat / Revenue Misses

EPS of $.17 beats Wall Street expectations of $.16 but revenue of $544.9 million is below expectations of $552 million.

Hims & Hers Earnings Are Out

It’s an earnings miss – shares are down 11%.

Revenue was below expectations. We’ll keep updating.

Here's the Guidance Hims & Hers Provided Last Quarter

Here’s the guidance Hims & Hers issued in their first quarter earnings:

For the second quarter 2025, we expect:

- Revenue of $530 million to $550 million.

- Adjusted EBITDA of $65 million to $75 million, reflecting an Adjusted EBITDA margin of 12% to 14%.

For the full year 2025, we expect:

- Revenue of $2.3 billion to $2.4 billion.

- Adjusted EBITDA of $295 million to $335 million, reflecting an Adjusted EBITDA margin of 13% to 14%.

Wall Street expects Him & Hers to reprot earnings better than the top end of this guidance with expectations of $552 million in second quarter revenue.

For the third quarter, Wall Street expects Him & Hers to guide toward $584 million in revenue.

How HIMS Performed After Recent Earnings

HIMS has delivered four consecutive post-earnings rallies, averaging +20.8% over 7 days — one of the most consistent momentum profiles in small-cap health tech.

| Quarter | Earnings Date | 1-Day Move | 7-Day Move | 14-Day Move |

|---|---|---|---|---|

| Q1 2025 | May 5, 2025 | +16.39% | +27.66% | +33.56% |

| Q4 2024 | Feb 24, 2025 | +11.78% | +15.81% | +26.91% |

| Q3 2024 | Nov 4, 2024 | +14.89% | +22.56% | +30.71% |

| Q2 2024 | Aug 5, 2024 | +6.98% | +15.36% | +22.23% |

Hims & Hers (NYSE: HIMS) reports Q2 2025 earnings after the market closes, following a strong Q1 marked by elevated demand for personalized health services and early traction in its weight loss category. The stock has been among the best small-cap performers YTD, fueled by narrative tailwinds around GLP-1 access and AI-driven telehealth platforms. In Q1, the company raised full-year guidance and reiterated its goal of positive adjusted EBITDA.

What to Expect

– Revenue: $278.66 million

– EPS (Normalized): $0.04

– FY 2025 Revenue: $1.14 billion

– FY 2025 EPS: $0.16

Revenue is expected to grow nearly 40% YoY, slightly above Q1’s growth rate. EPS is modest but consistent with the company’s transition from breakeven into profitability territory. FY guidance implies low- to mid-teens margin for the year.

Key Areas to Watch

Weight Loss Program Ramp

Management announced a weight loss program in Q1 built around GLP-1 prescriptions, behavior coaching, and diagnostics. The company said demand was strong and positioned the offering as central to future growth.

Active Subscribers & Attach Rate

Investors will watch growth in monthly subscribers and attach rates on personalized products — both metrics were key drivers of the company’s outperformance last quarter.

Profitability Path & Expense Mix

HIMS has turned adjusted EBITDA positive, but investors are focused on whether growth can scale without proportional increases in customer acquisition costs. Commentary on R&D and marketing efficiency will be closely tracked.

Gross Margin Stability

Gross margin remained above 75% in Q1 — a strong result given the cost of GLP-1s and personalized care delivery. Guidance here will shape expectations for sustainable margin profile.

AI and Care Experience Enhancements

CEO Andrew Dudum said the company is integrating AI to improve asynchronous care and diagnostics. Any proof points on automation or patient outcomes could extend the current bullish narrative.

Joel South covers large-cap stocks, dividend investing, and major market trends, with a focus on earnings analysis, valuation, and turning complex data into actionable insights for investors.

He brings more than 15 years of experience as an investor and financial journalist, including 12 years at The Motley Fool, where he served as an investment analyst, Bureau Chief, and later led the Fool.com investing news desk. He has also co-hosted an investing podcast and appeared across TV and radio discussing market trends.

© 24/7 Wall Street