Live: Hims & Hers Earnings Coverage

Quick Read

-

Hims & Hers Health enters Q3 earnings following 73% YoY revenue growth and robust subscriber momentu

-

Wall Street expects another quarter of double-digit topline growth with EPS of $0.10 on $579 million revenue.

Live Updates

What We Learned From the Quarterly Conference call

The call centered around Hims & Hers’ push beyond treatment into proactive and personalized health management. Dudum confirmed plans to launch whole-body lab testing before year-end, followed by a new longevity specialty in 2026 offering peptides, coenzymes, and GLP/GIP therapies to promote long-term wellness and prevention.

“Historically, people have come to us to manage existing conditions. Soon, we’ll help them take a more proactive role in managing their health,” Dudum said.

The company also reaffirmed its commitment to democratizing access through partnerships and vertical integration. Management highlighted ongoing talks with Novo Nordisk to offer Wegovy injections and oral formulations once approved, a partnership with Marius Pharmaceuticals for an oral testosterone launch in 2026, and a strategic investment in GRAIL, whose multi-cancer early detection test aligns with Hims & Hers’ preventive care ambitions.

Weight Loss and Hormone Health Growth Engines

Weight loss remains a key growth pillar. The company recently lowered prices on compounded GLP-1 plans by up to 20% and introduced microdosing options to enhance patient experience. Dudum said these efforts are supported by expanded sterile compounding infrastructure that will exceed 1 million square feet by year-end.

At the same time, Hims & Hers is entering new verticals in hormone and women’s health. Its low-testosterone offering has seen strong initial demand, and the perimenopause/menopause program aims to close what Dudum described as “one of the biggest gaps in women’s health.” The Hers brand is now on track to surpass $1 billion in annual revenue by 2026.

Financials and Outlook

CFO Yemi Okupe outlined steady progress toward long-term targets, citing improved marketing leverage and cash generation. Marketing spend dropped to 39% of revenue, down six points year-over-year, and operating cash flow reached $149 million, with free cash flow of $79 million and over $1.1 billion in cash and investments on the balance sheet.

For Q4 2025, Hims & Hers expects $605–$625 million in revenue and $55–$65 million in adjusted EBITDA (≈10% margin). Full-year guidance calls for $2.335–$2.355 billion in revenue and $307–$317 million in adjusted EBITDA (~13% margin).

A $20–$25 million revenue headwind in Q4 is anticipated due to the migration of GLP-1 fulfillment to 503(a) sterile facilities, but management expects normalization in the second half of 2026. Longer term, Hims & Hers reiterated its 2030 goal of $6.5 billion+ in revenue and $1.3 billion in adjusted EBITDA.

Global Expansion on Deck

The company’s international push is gaining traction following its ZAVA acquisition, now enabling operations across the U.K., Germany, France, Ireland, and Spain. A Canadian launch is next, expanding its North American footprint and positioning Hims & Hers for what management sees as a $1 billion+ annual global opportunity.

HIMS Now Up 8%

Earnings call will be live shortly and will post updates on this page.

New Growth Tracks

Hormonal health and lab testing launches remain on track.

CEO Andrew Dudum framed them as the next leg of platform expansion, tapping markets like menopause, testosterone care, and at-home diagnostics worth tens of billions.

These verticals are early but strategically critical.

GLP-1

The GLP-1 weight-loss program remains a cornerstone.

Management reaffirmed $725 M FY25 revenue from the category and cited steady retention after offboarding commercial dosages.

The pivot to oral semaglutide appears to be sticking with customers.

Key Operartion Highlights

| Metric | Q3 2025 | YoY Change | Comment |

|---|---|---|---|

| Active Subscribers | ~1.9 M | +42 % | Strong recurring revenue base |

| Gross Margin | 76 % | Flat | High efficiency in fulfillment |

| Adj. EBITDA | $84 M | +25 % | Operating leverage intact |

| GLP-1 Revenue Target | $725 M FY25 | Reaffirmed | Weight-loss franchise robust |

| Cash Balance | $380 M | +10 % QoQ | No net debt |

Hims’ quarter underscored a healthy business transitioning from hyper-growth to sustainable scale. The slight revenue miss reflects mix and timing, not demand erosion, while margins and cash flow continue to expand. With AI personalization, hormonal care, and global expansion still ahead, the long-term story remains intact, even if the stock needed a pause after its 2025 rally.

Management Commentary

“We’re building a comprehensive digital care system for millions of people seeking personalized, accessible medicine.” – CEO Andrew Dudum

Dudum highlighted the company’s expansion into preventative care and biomarker-based programs while keeping gross margins above 75 %. He framed AI and lab testing as the next stage of Hims’ “health membership” strategy.

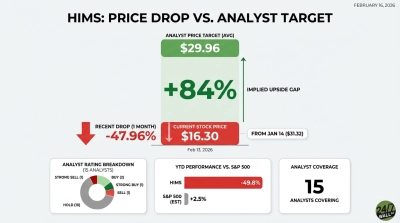

HIMS Down After Earnings

Shares are down 5.77 % after hours as investors digest a mixed print that pairs strong subscriber growth with softer-than-expected top-line momentum.

Headline results

| Metric | Estimate | Actual | Result |

|---|---|---|---|

| Revenue | $579.9 M | $573 M | Miss |

| EPS (Normalized) | $0.10 | $0.11 | Beat |

Flat guidance lookout – Management reaffirmed full-year guidance of roughly $2.35 B in revenue and $0.58 EPS, suggesting continued margin progress but a more measured topline trajectory into Q4.

HIMS delivered another profitable quarter, but the modest revenue miss relative to Street expectations took some air out of the post-earnings reaction. Growth in the weight-loss and mental-wellness categories remained robust, yet the market likely wanted stronger evidence that hormonal-health and lab-testing initiatives are already translating into incremental dollars. The reaffirmed outlook implies management is prioritizing durable margin expansion over chasing near-term revenue spikes.

Hims & Hers Health (NYSE: HIMS) reports fiscal third-quarter earnings after the close. The telehealth innovator has become one of 2025’s most closely watched growth stories as it continues scaling its precision-care platform across weight loss, sexual health, dermatology, and mental wellness.

The stock has climbed sharply this year on expectations that its next wave of growth—hormonal health, lab testing, and AI-driven personalization—will widen its addressable market well beyond virtual prescriptions. Yet with the company now operating at scale, investors will be watching whether profitability can keep pace with the surge in subscribers and new initiatives.

What to Expect

Wall Street anticipates Q3 FY2025 earnings of $0.10 per share on revenue of $579.85 million, reflecting about 44% year-over-year growth. Analysts see Q4 EPS rising to $0.13 as Hims benefits from higher daily-use adoption and international expansion.

For the full year, consensus forecasts $2.35 billion in revenue and $0.58 EPS, with FY2026 projections climbing to $2.88 billion and $0.79 EPS, respectively.

The company has consistently outperformed expectations—last quarter’s $0.17 EPS topped estimates by 6%, marking its fourth straight beat. Subscription growth and operating leverage remain core drivers, with gross margins improving to 76% and adjusted EBITDA topping $80 million last quarter.

Key Areas to Watch When Hims Reports Tonight

1. GLP-1 Retention and Weight Loss Trajectory

Hims’ personalized weight-loss program remains a major growth engine, though management has been offboarding customers from commercial GLP-1 dosages. The company reaffirmed its $725 million weight-loss revenue target for 2025, suggesting resilient demand and rising oral semaglutide adoption.

2. Hormonal Health Launch

The upcoming rollout in hormonal health marks Hims’ entry into a market exceeding 50 million U.S. adults. Treatments for menopause and testosterone deficiencies could diversify growth and reinforce the brand’s credibility in clinically driven care.

3. Lab Testing and Preventative Care Ecosystem

The acquisition of a blood-testing lab signals a broader shift toward longitudinal care. Management plans to offer at-home diagnostics and integrate biomarker data into personalized treatment plans—laying groundwork for a future “health membership” model.

4. AI-Powered Personalization

New CTO Mo Elshenawy detailed plans to deploy AI-driven agents that support both providers and patients through continuous engagement. Near-term initiatives include 24/7 personalized care agents, unified data systems, and automated fulfillment capabilities.

5. International Expansion and ZAVA Integration

The completed ZAVA acquisition extends Hims’ footprint across the U.K., France, and Germany, with Canada slated for 2026. Investors will look for commentary on early synergies and cross-border scalability as the company eyes multibillion-dollar international potential.

Joel South covers large-cap stocks, dividend investing, and major market trends, with a focus on earnings analysis, valuation, and turning complex data into actionable insights for investors.

He brings more than 15 years of experience as an investor and financial journalist, including 12 years at The Motley Fool, where he served as an investment analyst, Bureau Chief, and later led the Fool.com investing news desk. He has also co-hosted an investing podcast and appeared across TV and radio discussing market trends.

© 24/7 Wall Street