Live: Will Cava Group (CAVA) Soar After Q2 Earnings Today?

Key Points

-

Street expects $285.23M in Q2 revenue and EPS of $0.13, up 22% and down 23% YoY respectively.

-

All eyes on same-store sales and loyalty program traction.

-

Four straight beats, all with bullish post-earnings moves.

Live Updates

My reaction

CAVA’s growth narrative hinges on SSS momentum and margin durability — and this quarter showed cracks in comp growth that offset strong new unit economics.

| Metric | Pre-Earnings Estimate | Post-Earnings Update | Direction |

|---|---|---|---|

| FY25 Revenue | $1.19B | Likely revised lower | 📉 |

| FY25 EPS (GAAP) | $0.58 | Unchanged (beat Q2) | ⚖️ |

| FY25 SSS Growth | 6–8% | 4–6% | 📉 |

| FY25 New Stores | 64–68 | 68–70 | 📈 |

Sentiment Snapshot

-

Negative: Slowing comps and guidance reset crushed the bull thesis short term.

-

Mixed: Margins held steady and AUVs remain strong.

-

Positive: New store class performing well; 400+ unit milestone hit.

Same Stores Sales Hurting the Stock

Again same stores sales growth is really the cog in the wheel, pushing the stock lower.

What Changed This Quarter

-

Same-store sales growth slowed sharply to just +2.1%, from +10.8% in Q1.

-

FY25 SSS guide lowered by 200bps to 4–6%.

-

Unit growth outlook raised to 68–70 new openings, up from 64–68.

-

Adjusted EBITDA outlook held steady, suggesting operating leverage remains.

-

Pre-opening costs guided higher, hinting at backloaded buildouts or cost inflation.

Key Operating Highlights

AUVs and restaurant-level margins remain strong, but SSS deceleration and modest margin compression hint at traffic softness and rising input costs despite digital strength.

| KPI | Q2 2025 | Q2 2024 | YoY Change |

|---|---|---|---|

| Revenue | $278.2M | $231.4M | +20.3% |

| Same-Store Sales Growth | +2.1% | +14.4% | ↓ Decelerated |

| Net New Restaurants | 16 | 18 | ↓ Slight |

| Restaurant-Level Profit Margin | 26.3% | 26.5% | ↓ 20 bps |

| AUV | $2.94M | $2.69M | ↑ Strong |

| Adjusted EBITDA | $42.1M | $34.3M | +22.6% |

| Digital Revenue Mix | 37.3% | N/A | — |

| Net Income (GAAP) | $18.4M | $19.7M | ↓ Slightly |

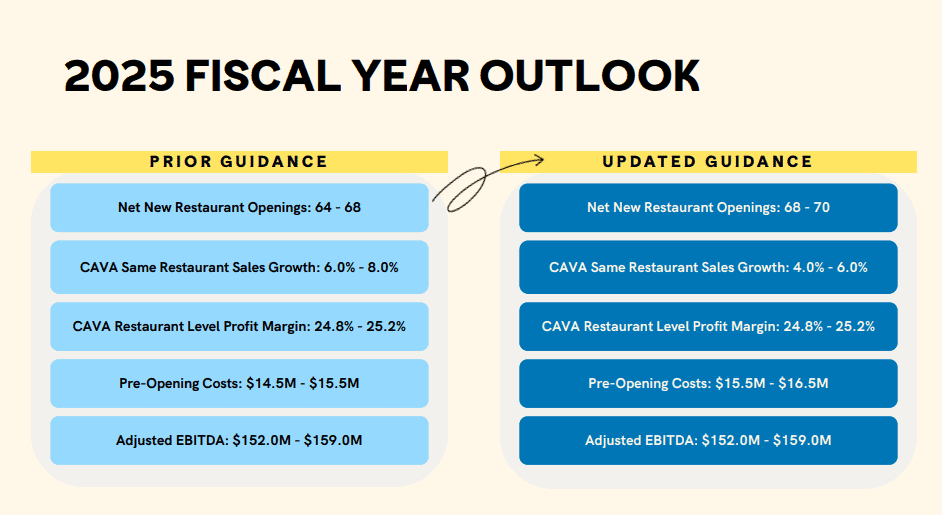

Guidance Update

| Metric | Prior (May 2025) | New (Aug 2025) | Direction |

|---|---|---|---|

| Net New Restaurants (FY25) | 64–68 | 68–70 | 📈 Raised |

| Same-Store Sales Growth (FY25) | 6.0%–8.0% | 4.0%–6.0% | 📉 Lowered |

| Restaurant-Level Profit Margin | 24.8%–25.2% | 24.8%–25.2% | ⚖️ Flat |

| Adjusted EBITDA | $152M–$159M | $152M–$159M | ⚖️ Flat |

| Pre-opening Costs | $14.5M–$15.5M | $15.5M–$16.5M | 📈 Raised |

Why it matters: The sharp downgrade to same-store sales growth (from 6–8% to 4–6%) is the key driver behind the market’s negative reaction — suggesting momentum is flattening earlier than expected

Management Commentary

“Despite the fluid macroeconomic environment, we grew CAVA Revenue 20.3%, and our 2025 new restaurant class is on track to deliver AUVs above $3 million.”

— Brett Schulman, Co-Founder & CEO

While emphasizing growth and new unit strength, Schulman’s comments downplayed the soft 2.1% SSS figure and shift in guidance. The upbeat tone contrasts with how the market interpreted the quarter: growth is no longer accelerating.

Shares Plummet After Earnings Release

CAVA shares plunged nearly 20% after the company posted a rare miss on revenue and significantly lowered its same-restaurant sales growth forecast for the year. Despite a solid EPS beat and robust new unit economics, the slowdown in comps growth and the guidance cut caught investors off guard, breaking the streak of clean beats and post-earnings rallies.

| Metric | Actual | Estimate | Beat/Miss |

|---|---|---|---|

| Revenue | $278.2M | $285.23M | ❌ Miss |

| EPS (GAAP) | $0.16 | $0.13 | ✅ Beat |

| Same-Store Sales Growth (SSS) | +2.1% | ~+4.5% est. | ❌ Miss |

How Cava Performed In Recent Quarters

CAVA has beat EPS in each of the last four quarters, averaging a +4.91% gain seven days post-earnings — suggesting the market rewards its consistent operational delivery.

| Quarter | EPS Surprise | 1-Day Move | 7-Day Move | 14-Day Move |

|---|---|---|---|---|

| Q1 2025 | +56.29% | +4.27% | +7.66% | +7.53% |

| Q4 2024 | +1,004.05% | +7.14% | +2.30% | +2.17% |

| Q3 2024 | +49.27% | +8.50% | +4.83% | +4.22% |

| Q2 2024 | +40.55% | +7.94% | +4.83% | +5.23% |

Cava Group (NYSE: CAVA | CAVA Price Prediction) is set to report Q2 earnings after the close, with consensus modeling continued top-line growth and modest EPS deceleration. This quarter lands at a critical inflection point as CAVA leans into its loyalty program rollout, kitchen technology upgrades, and broader national expansion. Same-restaurant sales trends and unit-level margin dynamics will be front and center as investors assess the sustainability of the brand’s growth strategy. Following four straight beats and strong post-earnings reactions, expectations are high for another clean quarter.

We’ll be updating this live blog with news and analysis right after CAVA’s earnings hit the newswires. To receive updates, all you have to do is leave this page open, and updates will post automatically.

What’s Expected

Wall Street consensus for Q2 FY2025:

– Revenue: $285.23 million

– EPS (Normalized): $0.13

Full-year FY 2025 forecasts:

Key Areas to Watch

Loyalty Program Uplift

Reimagined loyalty program drove +200bps increase in loyalty-linked sales in Q1. Early adoption is strong, but management hasn’t yet disclosed frequency lift. Investors will watch for deeper penetration and stickiness.

Kitchen Tech & Labor Model Efficiency

Generative AI prep alerts and digital kitchen displays are live in select restaurants. New labor model aims to boost AUVs in low-volume stores by reallocating staffing — early signs suggest guest experience and throughput gains.

Menu Innovation and Attachments

New garlic ranch pita chips and national steak launch driving mix lift and social media engagement. Expect further updates on “flavor platform” potential and seasonal product cadence to support comps.

New Market Entry and White Space

CAVA reiterated plans to enter South Florida and two additional Midwestern markets in 2025. Class of ’24 new units are exceeding expectations on both sales and margins, with 17%+ unit growth targeted.

Margin Investment vs. Profit Decline

Despite higher revenue, EPS is projected to decline YoY due to higher G&A, team wage investments, and the potential Q4 DTA release ending the historical tax shield. Analysts will probe margin leverage and capital allocation discipline.

Joel South covers large-cap stocks, dividend investing, and major market trends, with a focus on earnings analysis, valuation, and turning complex data into actionable insights for investors.

He brings more than 15 years of experience as an investor and financial journalist, including 12 years at The Motley Fool, where he served as an investment analyst, Bureau Chief, and later led the Fool.com investing news desk. He has also co-hosted an investing podcast and appeared across TV and radio discussing market trends.

© 24/7 Wall Street