Dividend Kings are stocks that’ve had their dividend payouts raised for 50 consecutive years or more, such as Target (NYSE:TGT | TGT Price Prediction), Becton Dickinson (NYSE:BDX), and Hormel Foods (NYSE:HRL). That is an exceptional feat that the vast majority of stocks in the market cannot match. For a business to pay rising dividends to its shareholders for half a century, it must truly be on a strong footing.

However, these Dividend King stocks sometimes trade at a discount. Sometimes, the market has an appetite for growth. In turn, dividend stocks can lose out. There are also times when interest rates are high and dividend stocks become unflattering. Why? Higher interest rates cause Treasury yields to rise, so investors feel more comfortable pursuing a 4% risk-free yield instead of investing in a Dividend King that yields the same.

We may be at a turning point, though.

The Federal Reserve is becoming more aggressive with interest rate cuts, and Treasury yields are declining. Dividend stocks can thus get a lot hotter in the coming months, especially undervalued Dividend King stocks.

Target (TGT)

Target was delivering hyper-explosive gains during the pandemic era, but has performed hideously since late 2021 as it corrected. The market may be taking things too far as TGT stock has slid down nearly 65% from its peak close. In fact, I see it as a steal.

In fiscal 2020 (ended on Feb 1, 2020), revenue was $78.1 billion, with $3.28 billion in net income. TGT stock’s price back then hovered in the $120-130 range. Both sales and profits grew sharply in the two years that followed, but the stock outran Target’s fundamentals. In fiscal 2025, revenue totaled $106.56 billion, with a net income of $4.09 billion.

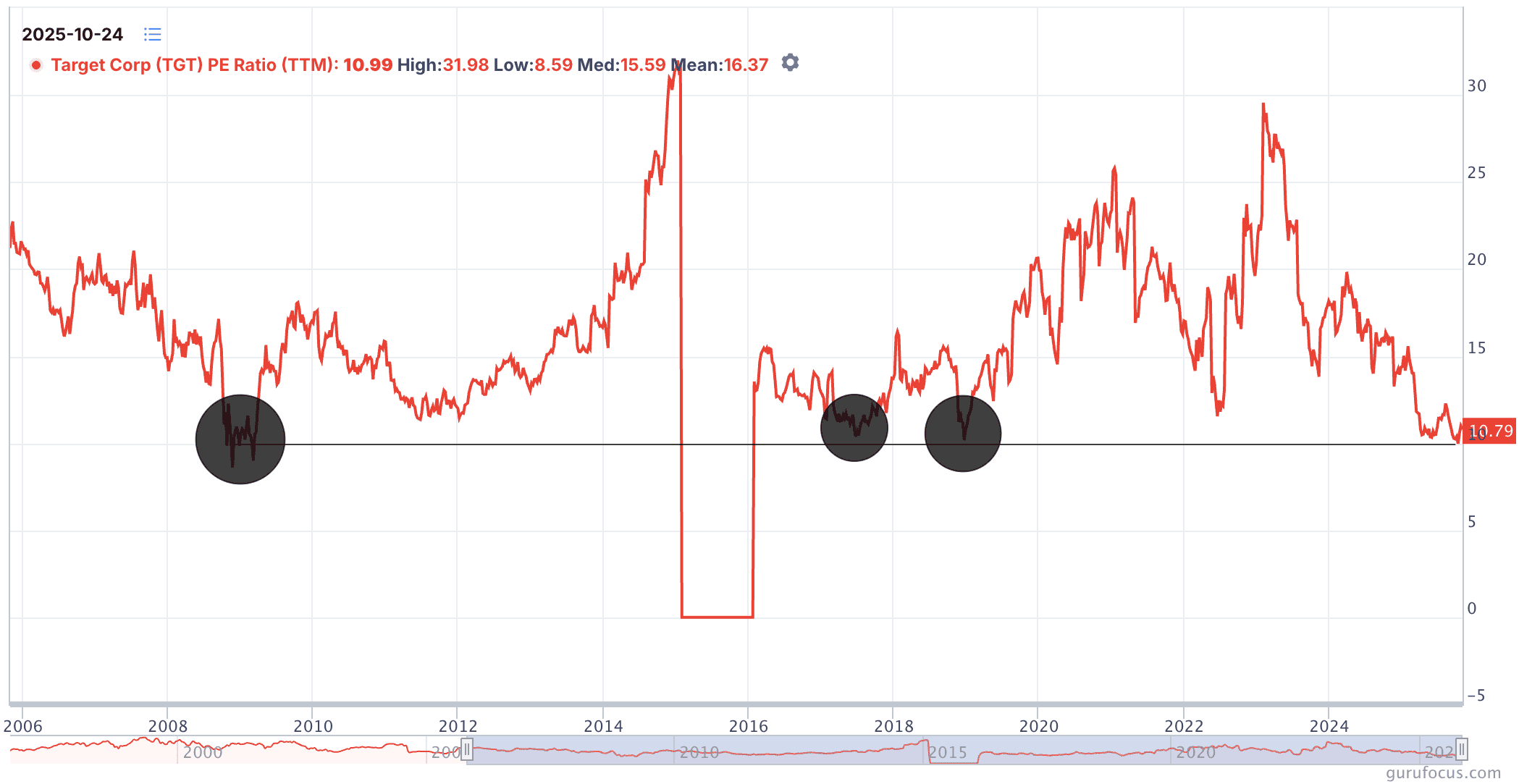

This is a slight correction compared to Target’s metrics in the two previous fiscal years. Wall Street already stripped out the unrealistic growth premium, and TGT stock trades in the $90 range today. A fair value would be closer to $140, even if you’re a conservative investor.

You’re paying less than 11 times earnings today, whereas TGT stock has historically traded at around 15 times earnings. Target stock has shown a tendency to bounce back strongly once it drops below 12 times earnings.

Therefore, I’m quite bullish, both in the short term and long term. And it doesn’t hurt that you can lock in a 4.92% dividend yield. Target has increased its dividends for 56 consecutive years.

Becton Dickinson (BDX)

Beckton Dickinson makes medical supplies, devices, laboratory equipment, and diagnostic products. Medical supplies, or most things related to hospitals and healthcare, are often considered the holy grail of stable businesses. Demand is always there, and it’s non-discretionary.

Unfortunately, 2025 has been a tough year for many healthcare businesses. Beckton Dickinson is no exception.

It’s facing a myriad of problems, namely tariffs and reduced research funding. Both can be dealt with and are unlikely to be a long-term drag. As management itself noted in its Q2 earnings call transcript, “…nearly 80% of our U.S. revenue currently sourced from our U.S. manufacturing network or tariff-exempt sources.”

Both the top line and the bottom line continue to grow. Analysts expect 9.4% EPS growth in fiscal 2025 (ended in September), with 7.92% revenue growth.

If you exclude one-time expenses, you’re paying a bit more than 12 times earnings. Historically, BDX stock has traded around 27 times earnings minus non-recurring items.

I expect the stock to bounce back as the cons are priced in. The market is yet to reward it for the pros. The dividend yield is 2.31%, with a payout ratio of 29%. BDX has 52 consecutive years of dividend growth.

Hormel Foods (HRL)

Hormel Foods makes branded food products like meat, nuts, and other meals. HRL stock is down 55.8% in the past five years, and the selloff has only accelerated. Year-to-date, it is down 31.8%.

Multiple negative catalysts lined up at once. Hormel dealt with a margin squeeze, a bird flu, plus a fire that damaged a production facility in Arkansas. Its recent earnings report slashed Q4 EPS guidance $0.08 to $0.09 below its previous forecast. The previous guidance had adjusted EPS between $0.38 and $0.40 in Q4, with the revised one forecasting $0.29 to $0.32.

It will take time for HRL stock to stabilize from its current beleaguered state. I expect it to eventually happen, as inflation and bird flu won’t be around forever, nor will a production facility catch fire every year. I see the rare bevy of negative events as a buying opportunity.

HRL stock gives you a fat dividend yield of 5.4%. The payout ratio is 78.4% and comfortably covers that dividend. Hormel also has 59 consecutive years of dividend growth under its belt.