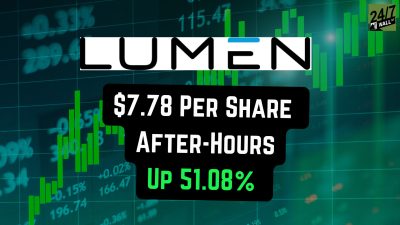

Lumen Technologies (NYSE: LUMN) and Verizon Communications (NYSE: VZ | VZ Price Prediction) just closed their Q3 2025 earnings reports, and the contrast is stark. Verizon posted $5.06 billion in net income while Lumen logged a $621 million loss. One is a dividend aristocrat leaning into customer-first transformation. The other is betting its future on AI infrastructure and enterprise connectivity.

One Bleeds Cash, One Generates It

Lumen missed revenue estimates at $3.09 billion but beat on adjusted EPS with a $0.20 loss versus the $0.27 expected. The $621 million net loss nearly tripled the $148 million loss in Q3 2024. Adjusted EBITDA fell to $787 million from $899 million. Mass markets revenue dropped 8% to $631 million. North America business revenue declined 3% to $2.38 billion.

CEO Kate Johnson emphasized disciplined execution and transformation. The company closed $1 billion in new Private Connectivity Fabric deals, targeting enterprises building out AI workloads. Lumen refinanced $2.4 billion in debt, saving $135 million annually in interest. Free cash flow hit $1.66 billion, and the company held $2.4 billion in cash. Johnson reaffirmed full-year guidance and expects to land at the high end of the EBITDA range.

Verizon delivered $33.82 billion in revenue, missing the $35.31 billion estimate, but met EPS expectations at $1.21. Net income climbed to $5.06 billion from $3.41 billion. Wireless service revenue rose 2.1% to $21.0 billion. Wireless equipment revenue increased 5.2% to $5.6 billion. Free cash flow over nine months reached $15.76 billion.

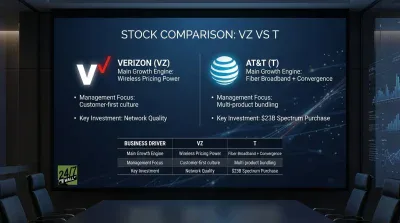

CEO Dan Schulman announced a strategic pivot to a customer-first culture and signaled bold action to redefine the company’s trajectory. Verizon raised its dividend for the 19th consecutive year to $0.69 quarterly, yielding 6.7%. The company reaffirmed full-year guidance for wireless service revenue growth of 2.0% to 2.8%, adjusted EBITDA growth of 2.5% to 3.5%, and EPS growth of 1.0% to 3.0%.

Infrastructure Bet vs. Scale Pivot

Lumen is shrinking its legacy telecom footprint and pivoting hard into AI infrastructure. The Private Connectivity Fabric platform targets enterprises moving compute to the edge. The company is scaling its Network-as-a-Service offering and launching IoD offnet capabilities. Revenue is declining, losses are widening, and book value is negative at $1.14 per share. The bet is that AI infrastructure demand will eventually offset legacy telecom erosion.

Verizon operates at massive scale with 11 times Lumen’s revenue and serves nearly all Fortune 500 companies. Schulman’s comments suggest urgency around cost structure and customer experience. The company is not pivoting to a new market but executing better in the market it already dominates. The dividend yield and profitability provide a cushion that Lumen lacks.

Key Differences in Risk Profiles

Verizon generates profits, pays a 6.7% dividend, and trades at a P/E of 8.8. The company posted $5.06 billion in net income for Q3 2025 and maintains a 19-year streak of consecutive dividend increases.

Lumen represents a turnaround situation with higher risk and potential reward tied to AI infrastructure adoption. The company is unprofitable, highly leveraged, and experiencing revenue declines while pivoting to new markets. The investment case depends on whether AI infrastructure deals scale quickly enough and margins improve before legacy telecom erosion accelerates further.