At different stages of life, you might have to make some tricky financial decisions. For example, if you decide to become a homeowner, you’ll need to calculate how much you can afford to spend on housing. And if you decide to pay for your kids’ college, you’ll need to weigh the cost of more expensive tuition against other financial goals.

Similarly, once you get older, you’ll need to decide when to start getting Social Security benefits. The earliest age you can file for them is 62.

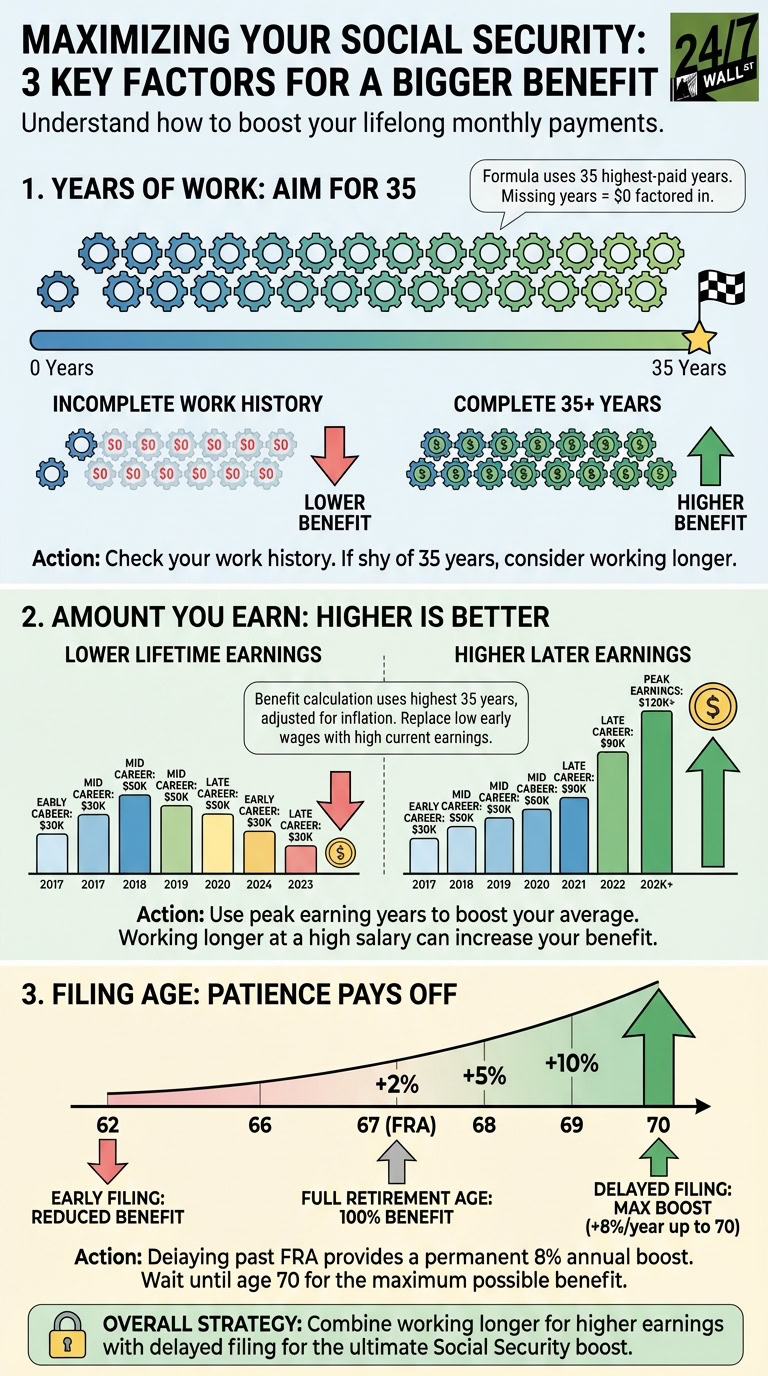

However, you’re not eligible for your complete Social Security benefit each month until full retirement age (FRA) arrives, which is 67 for anyone born in 1960 or later. If your FRA is 67 and you claim Social Security at 62, you’ll reduce your monthly benefits by about 30% for the rest of your life.

Not only that, but you can also claim benefits after FRA for larger ongoing payments. For each year you delay your claim past that point, up until age 70, your benefits get a permanent 8% boost.

If you ask financial guru Dave Ramsey when to claim Social Security, he might tell you to sign up at 62, despite that being a somewhat controversial answer. But there’s a big reason Ramsey is a fan of claiming Social Security at the earliest age possible.

Why Ramsey believes in signing up for Social Security at 62

Claiming Social Security at 62 can be risky, because if you don’t have a lot of savings to supplement your benefits, you could end up short on income. However, Ramsey thinks it makes the most sense to claim Social Security as soon as possible because, as he puts, it, “Your retirement payments die when you die…so you might as well take the money and make the most of it while you can.”

What Ramsey means is that if you don’t end up living a long life, you can get the most money out of Social Security by signing up for benefits at 62. And even if you end up living an average lifespan, at 62, you can’t predict whether that will happen. For this reason, Ramsey is a fan of taking the money sooner and, ideally, putting it to good use.

One thing he especially suggests is investing your Social Security benefits if you don’t need the money to cover your costs. As he says, “You can do a much better job investing that money than the government ever could.”

How to decide when to claim Social Security

If you’re having a tough time deciding when to sign up for Social Security, there are some important questions you can ask yourself to make that choice easier:

- How much income will my savings provide outside of Social Security?

- How good is my health, and do I think I’ll live an average lifespan or longer?

- What does my family history of longevity look like?

- Do I want to continue working in retirement, or will I need larger benefits to make ends meet?

You may also want to consult a financial advisor for guidance on when to claim Social Security. An advisor can look at your specific finances and situation to help you arrive at a decision that makes sense for you.