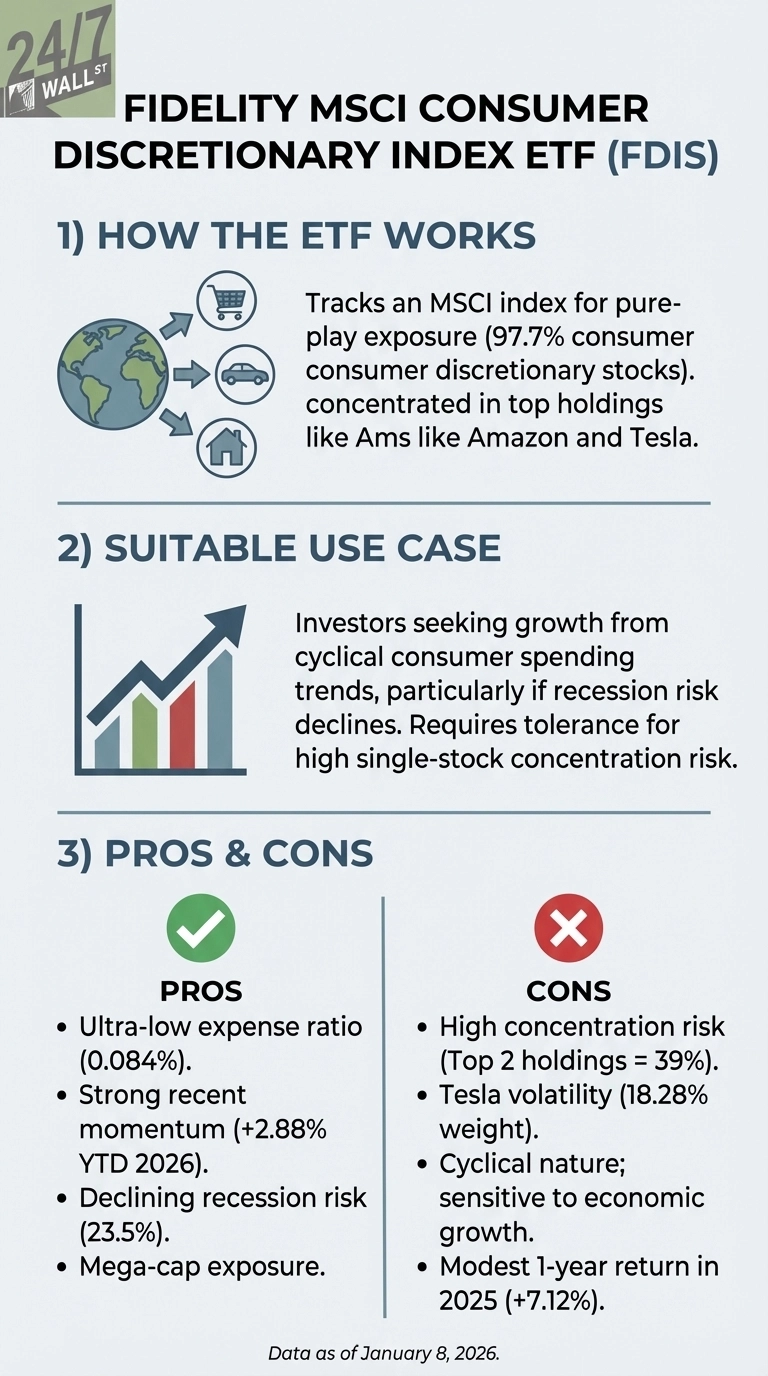

The Fidelity MSCI Consumer Discretionary Index ETF (NYSEARCA:FDIS) isn’t making headlines, and that’s the point. Up 3% to start 2026 after a 7% gain in 2025, this $1.9 billion fund has quietly underperformed the broader market while charging just 0.084% annually. The question is whether sleepy becomes profitable as consumer spending shifts in 2026.

FDIS gives investors pure-play exposure to consumer discretionary stocks, tracking an MSCI index that’s 97.7% concentrated in the sector. Nearly 40% of the portfolio sits in just two stocks. Amazon (NASDAQ:AMZN | AMZN Price Prediction) commands 21% while Tesla (NASDAQ:TSLA) holds 18.28%, creating a tug-of-war playing out in real time. Amazon is up nearly 6% year-to-date, while Tesla has declined 3.75%, explaining much of FDIS’s early momentum.

Consumer Spending: The Make-or-Break Factor

The biggest macro force shaping FDIS in 2026 is consumer spending growth, which economists expect to moderate significantly. S&P Global forecasts real consumer spending growth will slow to 2% in 2026 from 2.7% historically, marking a cycle low. This matters because consumer discretionary stocks live and die by discretionary income. When households tighten budgets, they cut restaurant visits, delay home improvement projects, and postpone new car purchases before touching essentials.

The positive signal? Recession probability on prediction markets has dropped from 32% to 23.5% over the past month, suggesting the economy may achieve a soft landing. For FDIS investors, this is the data point to watch. Monthly consumer spending reports from the Bureau of Economic Analysis, released around month-end, will show whether households are maintaining spending patterns or pulling back. If spending growth stays near 2%, FDIS should hold up. If it dips toward 1%, expect the ETF to struggle as investors rotate toward defensive sectors.

The Tesla Problem

While macro trends set the stage, FDIS’s micro challenge is Tesla’s earnings deterioration. The company’s annual earnings per share collapsed 63.8% in 2025, falling from $2.32 to just $0.84. Tesla’s Q1 2025 earnings missed estimates by 65.71%, posting $0.12 EPS versus $0.34 expected, in what was arguably the worst quarterly performance since the company turned consistently profitable.

At 18.28% of FDIS, Tesla’s fundamental weakness creates significant downside risk that Amazon’s strength may not fully offset. Investors should monitor Tesla’s quarterly earnings reports and delivery numbers. If Tesla can stabilize earnings around current levels, FDIS remains viable. If earnings continue deteriorating or delivery growth stalls, that 18% allocation becomes a millstone.

Consider VCR Instead

For investors seeking similar exposure with less single-stock risk, the Vanguard Consumer Discretionary ETF (NYSEARCA:VCR) offers a compelling alternative. VCR charges just 0.09% annually (only slightly higher than FDIS) but brings $6.9 billion in assets and a track record dating to 2004 versus FDIS’s 2013 inception. VCR’s concentration is marginally lower, with Amazon at 21.4% and Tesla at 17.4%. VCR’s larger asset base provides better liquidity and tighter bid-ask spreads for active traders.

The Bottom Line

FDIS’s 2026 performance hinges on whether consumer spending holds near 2% growth and whether Tesla can stop the earnings bleeding. Watch the monthly consumer spending reports and Tesla’s quarterly delivery numbers. Those two factors will determine if this sleepy ETF delivers easy money or just more mediocrity.