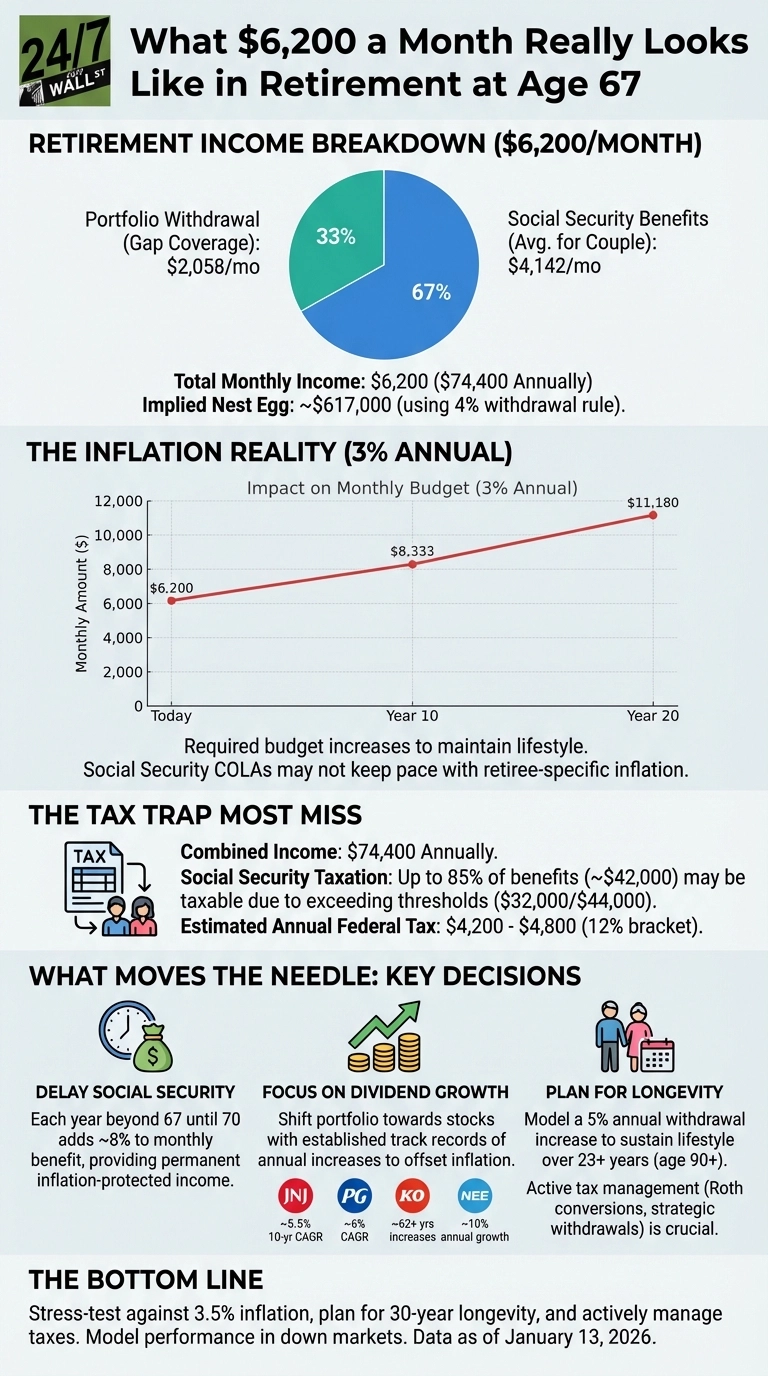

A retired couple living on $6,200 monthly ($74,400 annually) with average Social Security benefits of $2,071 each (totaling $4,142) withdraws approximately $2,058 from their portfolio to cover the gap. That suggests a nest egg around $617,000 using the 4% withdrawal rule. The challenge isn’t whether this works today—it’s whether it still works in year 15 or 20.

The Inflation Reality Nobody Talks About

At 3% annual inflation, that $6,200 monthly budget needs to become $8,333 in 10 years and $11,180 in 20 years just to maintain the same lifestyle. Social Security includes cost-of-living adjustments, but they don’t always keep pace with retiree-specific inflation, particularly healthcare costs.

If Social Security grows at 2.5% annually but actual expenses rise 3.5%, the gap widens every year. Portfolio withdrawals must increase faster than the 4% rule anticipates. A $617,000 portfolio generating modest growth might handle this for 15 years, but sequence-of-returns risk—poor market performance early in retirement—can derail the plan entirely.

The Tax Trap Most Retirees Miss

At $74,400 in combined income, this couple likely faces taxation on up to 85% of their Social Security benefits. The thresholds are $32,000 for any taxation and $44,000 for maximum taxation (married filing jointly), and these haven’t been adjusted for inflation since 1984. With roughly $50,000 in Social Security and $25,000 in withdrawals, their provisional income exceeds $44,000, meaning up to $42,000 of Social Security becomes taxable.

The 2026 standard deduction of $32,200 helps, but they’re still paying federal tax on approximately $35,000 to $40,000 of income. At 12% bracket rates, that’s $4,200 to $4,800 annually—money that can’t compound or cover rising expenses. The fix: Roth conversions in early retirement years, strategic withdrawal sequencing, or qualified charitable distributions after age 70½ can reduce lifetime tax bills substantially.

What Actually Moves the Needle

Three decisions matter most. First, delay Social Security beyond 67 if possible—each year until 70 adds roughly 8% to the monthly benefit, providing permanent inflation-protected income. Second, shift portfolio allocation toward dividend growth rather than pure yield. Dividend growth stocks with established track records of annual increases provide rising income without selling shares, helping offset inflation over time. High-yield investments may look attractive initially but can deliver negative total returns if the underlying business deteriorates, eroding capital.

Third, plan for longevity. A 67-year-old couple has significant odds that one spouse reaches 90 or beyond. That’s 23+ years of inflation compounding, healthcare cost increases, and potential long-term care needs. Building a 5% annual withdrawal increase into projections—rather than assuming static spending—reveals whether the portfolio can actually sustain the lifestyle.

The Bottom Line

This scenario works if the couple stress-tests it against 3.5% inflation, plans for 30-year longevity, and actively manages tax efficiency. The biggest mistake is assuming today’s comfort equals tomorrow’s security. Run the numbers assuming expenses rise faster than Social Security COLAs, model portfolio performance in down markets, and consider whether part-time work in early retirement could delay withdrawals by even three years. Those adjustments transform a marginal plan into a durable one.