Marriage and money rarely align perfectly, especially when childhood experiences shape opposing financial philosophies. When one spouse sees opportunity and the other sees risk in the same cash pile, resolution requires more than math.

On a January 2026 episode of The Dave Ramsey Show, Joe from Huntsville called in with a problem many couples face: conflicting money philosophies creating real tension. The couple had sacrificed for years while she stayed home raising their children, carefully setting aside every spare dollar until they’d accumulated $122,000—a sum that represented security to her husband but felt like wasted potential to Joe. That security blanket came with a hidden cost: $23,000 in student loan debt still hanging over them, draining their resources month after month.

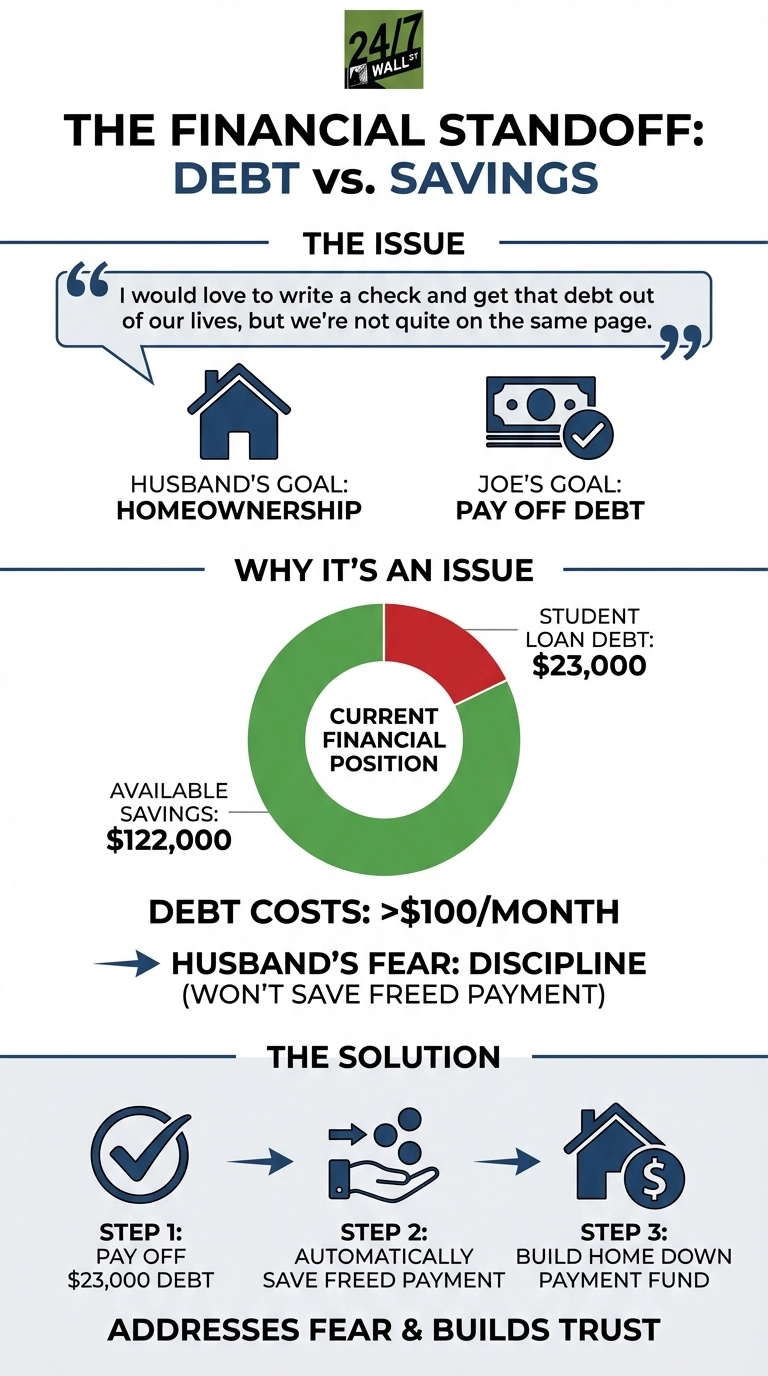

“I would love to write a check and get that debt out of our lives, but we’re not quite on the same page,” Joe explained. “My husband’s not comfortable with that yet because we’re not homeowners.”

Rachel Cruze identified the core issue. “He’s wanting to be a homeowner, which is one of the largest financial purchases you ever make,” she said. “He wants to do that big thing first before paying off debt.”

Joe had mapped out a path forward that addressed both their goals: eliminate the debt that cost them money every month, put down enough on a home to avoid the extra insurance fees that come with smaller down payments, and still keep enough cash on hand to weather unexpected storms. “That would leave us pretty comfortable,” she said. Her husband’s real fear centered on discipline: “That we wouldn’t actually save” the freed-up monthly payment. When Cruze asked about his upbringing, Joe revealed his family “spoke about money very often except during tight financial seasons”—a pattern that explained his anxiety about watching their cash reserves decline.

Where the Advice to Pay Off Debt First Holds Up

The math strongly favors Joe’s position. Their student loan debt wasn’t just a number on a statement—it represented more than $100 vanishing from their account every single month, money that could never be recovered or redirected toward their dreams. Eliminating that $23,000 debt would transform their monthly cash flow, turning payments that disappeared into interest into dollars they could funnel directly toward their home down payment fund.

Even after eliminating the debt, they’d maintain substantial financial flexibility. Their remaining cash would support a strong down payment that avoids private mortgage insurance while keeping ample reserves for emergencies. The couple wouldn’t be stretching themselves thin—they’d be optimizing their position for homeownership.

Where the Situation Needs Context

The husband’s concern about discipline isn’t irrational. Many households that eliminate debt fail to redirect freed payments toward savings, treating extra cash flow as lifestyle inflation. Without automatic transfers or clear accountability, monthly payments can disappear into restaurant meals and subscriptions.

Housing market timing also matters. In competitive markets, delaying a purchase while paying off debt could mean watching home prices rise faster than savings accumulate. If local prices increase annually, waiting to save additional funds could cost more in appreciation than the interest saved on debt.

Options This Couple Might Consider

This standoff requires addressing trust, not just spreadsheets. The husband’s childhood scarcity created legitimate fear that needs acknowledgment, not dismissal. One approach could involve proposing concrete accountability: automatic monthly transfers of the freed payment into a dedicated home savings account, with both spouses receiving notifications.

A middle path exists. Paying off the debt while committing to automated savings and setting a specific home purchase timeline represents one potential path. This approach eliminates interest costs, builds trust through demonstrated discipline, and maintains substantial reserves. Financial decisions made from fear often cost more than the risks being avoided.