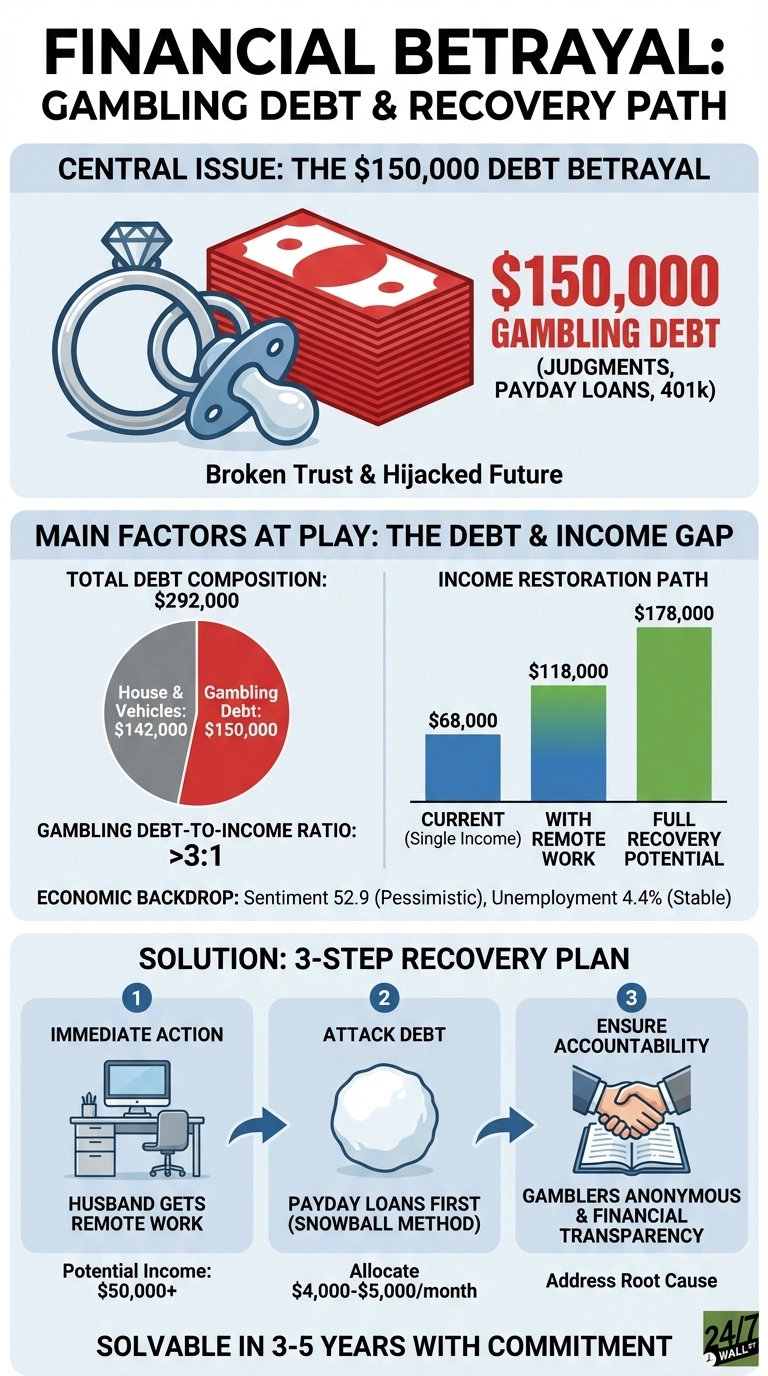

Discovering $150,000 in hidden gambling debt after marriage and a new baby ranks among the most devastating financial betrayals a spouse can face. This isn’t just about money, it’s about broken trust, deception during vulnerable life transitions, and the sudden realization that your financial future has been hijacked by addiction.

This scenario mirrors countless others playing out across the country. A Reddit user recently shared discovering their partner had accumulated £16,000 in gambling debt through loans and maxed credit cards, writing: “This has completely destroyed my plans for the financial future.”

The Core Financial Reality

| Category | Amount |

|---|---|

| Gambling debt (judgments, payday loans, emptied 401k) | $150,000 |

| Current household income (single earner) | $68,000 |

| Husband’s potential income (when recovered) | $95,000-$110,000 |

| Additional secured debt (house, vehicles) | $142,000 |

| Total debt burden | $292,000 |

The critical issue isn’t the debt size, it’s the income gap. On Heather’s $68,000 salary alone, they’re carrying a debt-to-income ratio over 3:1 on gambling debt alone. The $53,000 and $19,000 judgments likely carry 8-12% interest rates, while payday loans typically charge 15-30% APR. Every month of delay costs hundreds in interest.

With consumer sentiment at 52.9 in January 2026 (deep pessimism territory) and unemployment at 4.4%, the economic backdrop adds pressure. But the moderately healthy job market means remote work opportunities exist for someone with her husband’s earning potential.

The Path Forward Requires Immediate Action

Bankruptcy might seem appealing, but with her husband’s $95,000-$110,000 earning capacity, they’d likely fail the means test. The better path: aggressive income restoration and debt elimination.

First priority: Her husband must find remote work immediately. A torn Achilles doesn’t prevent computer-based work. Even a $50,000 remote role would nearly double household income. At $160,000+ combined income, they could eliminate gambling debt in three years by allocating $4,000-$5,000 monthly to debt payoff.

Second priority: Attack payday loans first. These carry the highest rates and most predatory terms. The debt snowball method builds psychological momentum as smaller balances disappear.

Third priority: Protect the marriage through accountability. Her husband needs Gamblers Anonymous, financial transparency (shared access to all accounts), and possibly addiction counseling. Without addressing the behavioral root cause, debt payoff is temporary.

What Matters Most Right Now

This situation is solvable in three to five years if her husband returns to full earning capacity and maintains gambling sobriety. The math works. The question is whether the marriage can withstand the strain of recovery, resentment, and constant temptation.

Evaluate his commitment to transparency and recovery first. If he’s genuinely broken by consequences and willing to submit to complete financial accountability, the path exists. If he’s minimizing, deflecting, or resistant to oversight, the financial problem is secondary to a much deeper issue that money can’t fix.