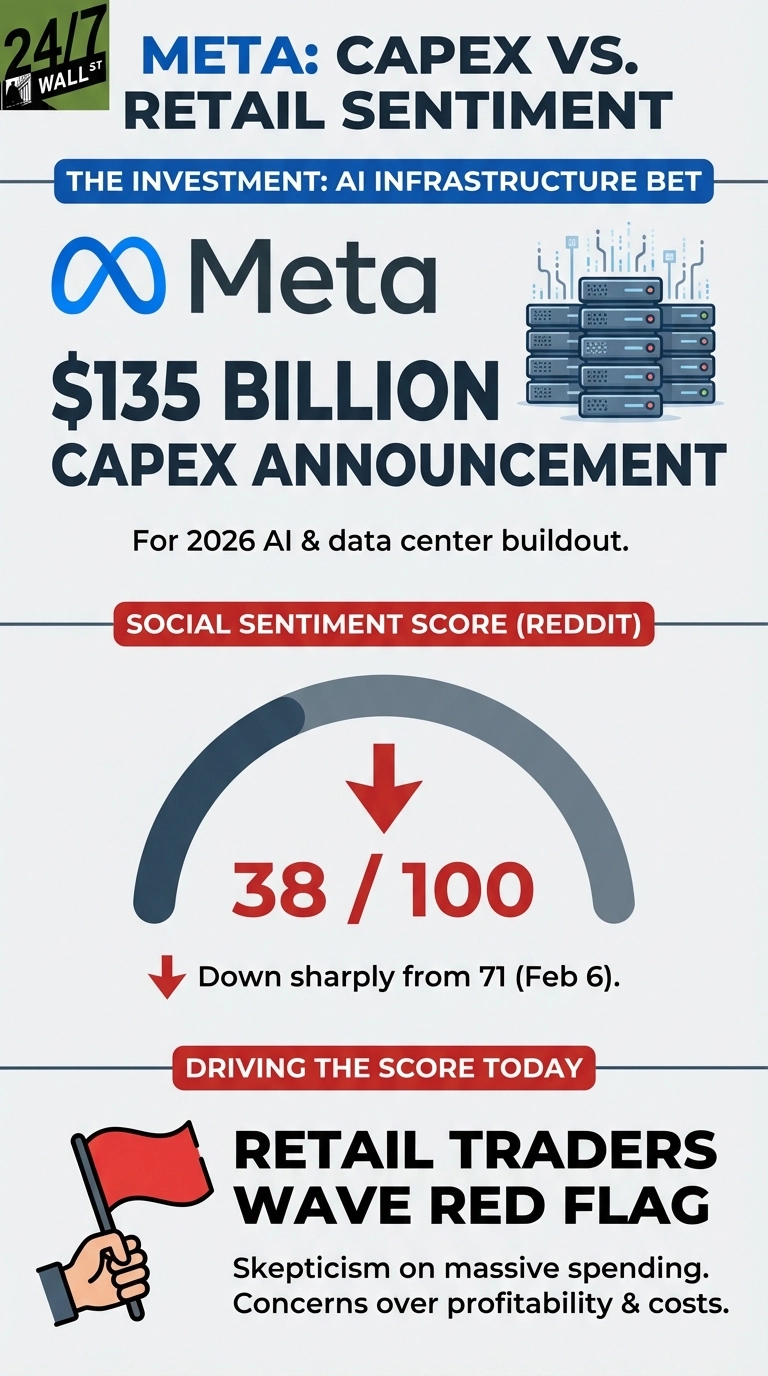

Shares of Meta Platforms (NASDAQ:META | META Price Prediction) surged 10.4% on January 29, 2026, the day after the company announced plans to spend up to $135 billion on capital expenditures in 2026. Wall Street cheered the massive AI infrastructure bet, but retail traders are waving red flags. Reddit sentiment sits at just 38 out of 100 as of February 9, down sharply from a 71 score on February 6. The divergence is striking. Institutional investors see Meta’s $115-135 billion capex guidance as necessary positioning in the AI race, while everyday traders question whether the spending spree will pay off.

Retail Traders Question the Math

Discussions on Reddit reveal deep skepticism about Meta’s spending trajectory. The $135 billion capex figure represents a near-doubling from $72.22 billion in 2025, and retail investors are asking tough questions. Activity spiked on r/wallstreetbets and r/investing as traders debated whether the AI infrastructure buildout justifies the cost. One highly engaged thread titled “GOOG: I’m spending $180b on Capex. AMZN: ‘Hold my beer'” captured the sentiment, with users comparing Big Tech’s capital spending arms race, including Amazon (NASDAQ:AMZN).

GOOG: I’m spending $180b on Capex. AMZN: ‘Hold my beer’

by Embarrassed-Egg-545 in stocks

The concerns are tangible:

- Reality Labs remains unprofitable despite billions in investment

- The capex commitment represents nearly 1.3x annual EBITDA of $101.9 billion

Wall Street Sees Different Picture

While retail sentiment has turned bearish, analysts remain overwhelmingly bullish with 62 of 67 analysts rating META a buy and a consensus price target of $859.85. Shares have since pulled back 7.68% over the past week to $661.46, giving up most of the post-earnings gains. Alphabet (NASDAQ:GOOGL) faces similar dynamics, with shares down 4.48% over the past week despite announcing its own $175-185 billion capex guidance. For investors trying to navigate this divergence, the key question is whether Meta’s four consecutive quarters of earnings beats and 24% revenue growth can continue absorbing the infrastructure costs, or if margin pressure will force a reckoning.