Auto insurance premiums continue to climb across the United States, and even drivers with spotless records are feeling the pinch. While conventional wisdom suggests that careful driving should keep costs down, the reality is that insurers price policies based on factors far beyond individual driving history.

The mechanics of insurance pricing reveal why premiums keep rising regardless of personal behavior. Insurers calculate rates using a complex mix of regional repair costs, medical expense inflation, litigation trends, and regulatory approval processes. A driver in Cleveland with no accidents may still face steep increases because repair shops in their area charge more, or because local courts award larger settlements in injury cases.

Repair costs have become a particularly stubborn driver of premium growth. Modern vehicles packed with sensors, cameras, and advanced safety systems cost significantly more to fix after even minor collisions. A fender-bender that once required simple bodywork now often involves recalibrating multiple electronic systems, pushing repair bills higher. These costs flow directly into insurance pricing models.

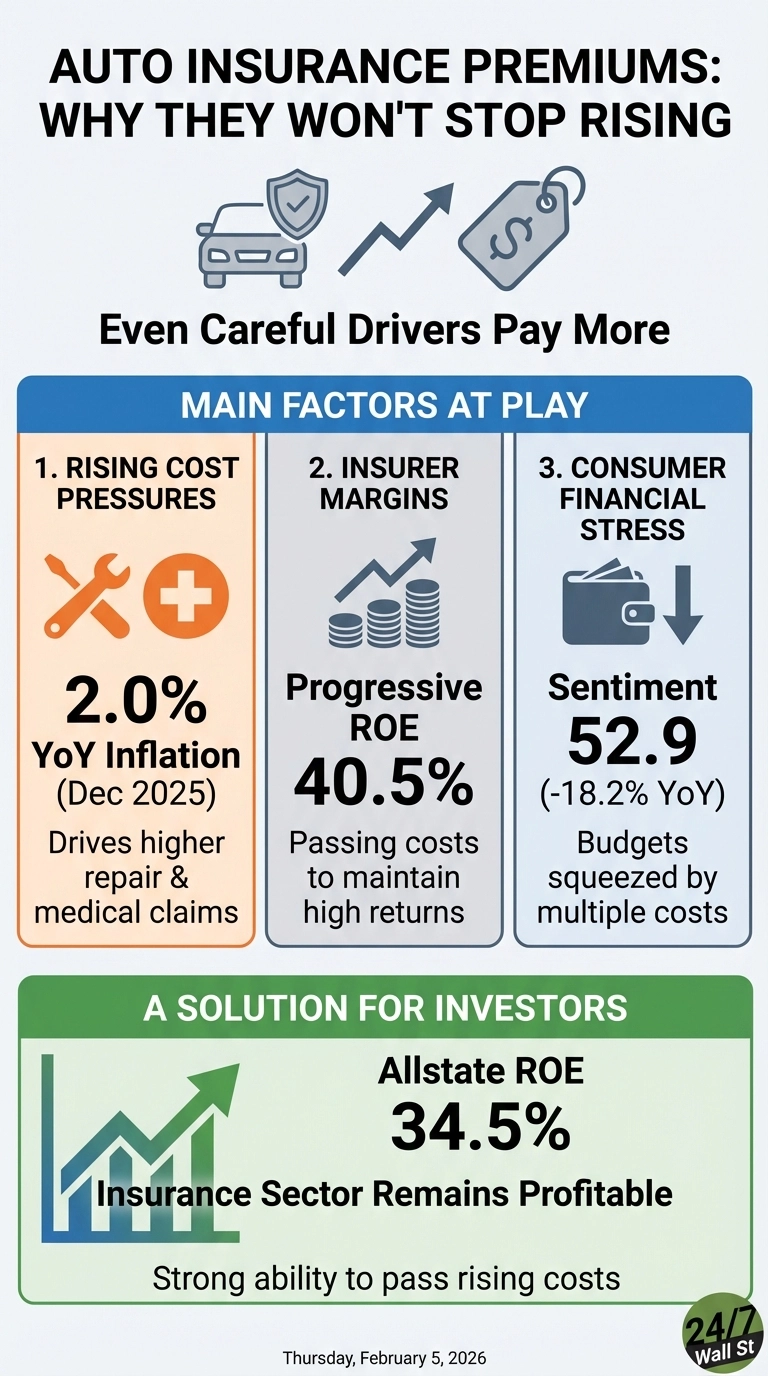

Medical inflation adds another layer of pressure. When someone gets injured in an accident, insurers cover medical bills that have been rising faster than general inflation. Overall inflation reached 2.0% year-over-year as of December 2025, but healthcare costs typically increase at a faster pace, forcing insurers to build higher payouts into their rate structures.

Litigation trends also play a crucial role. Some regions see more frequent lawsuits and larger jury awards in auto injury cases, creating what insurers call “social inflation.” These legal costs get distributed across all policyholders in affected areas, meaning careful drivers subsidize the rising cost of settling claims through the court system.

The insurance industry itself has demonstrated strong financial performance despite these cost pressures. Progressive Corp reported a 40.5% return on equity with quarterly earnings growth of 25.2% year-over-year, while Allstate posted a 34.5% return on equity with 222% quarterly earnings growth. These figures suggest insurers have successfully passed rising costs to consumers while maintaining healthy margins.

Consumer financial stress is mounting as premiums rise. The University of Michigan Consumer Sentiment Index fell to 52.9 in December 2025, down 18.2% from the previous year, reflecting growing household budget pressures from multiple cost categories including insurance.

For drivers seeking relief, the unfortunate truth is that individual driving records matter less than structural industry costs. Shopping around remains worthwhile, as different insurers weigh risk factors differently, but expecting premiums to stabilize based solely on safe driving is unrealistic given the broader economic forces at work.