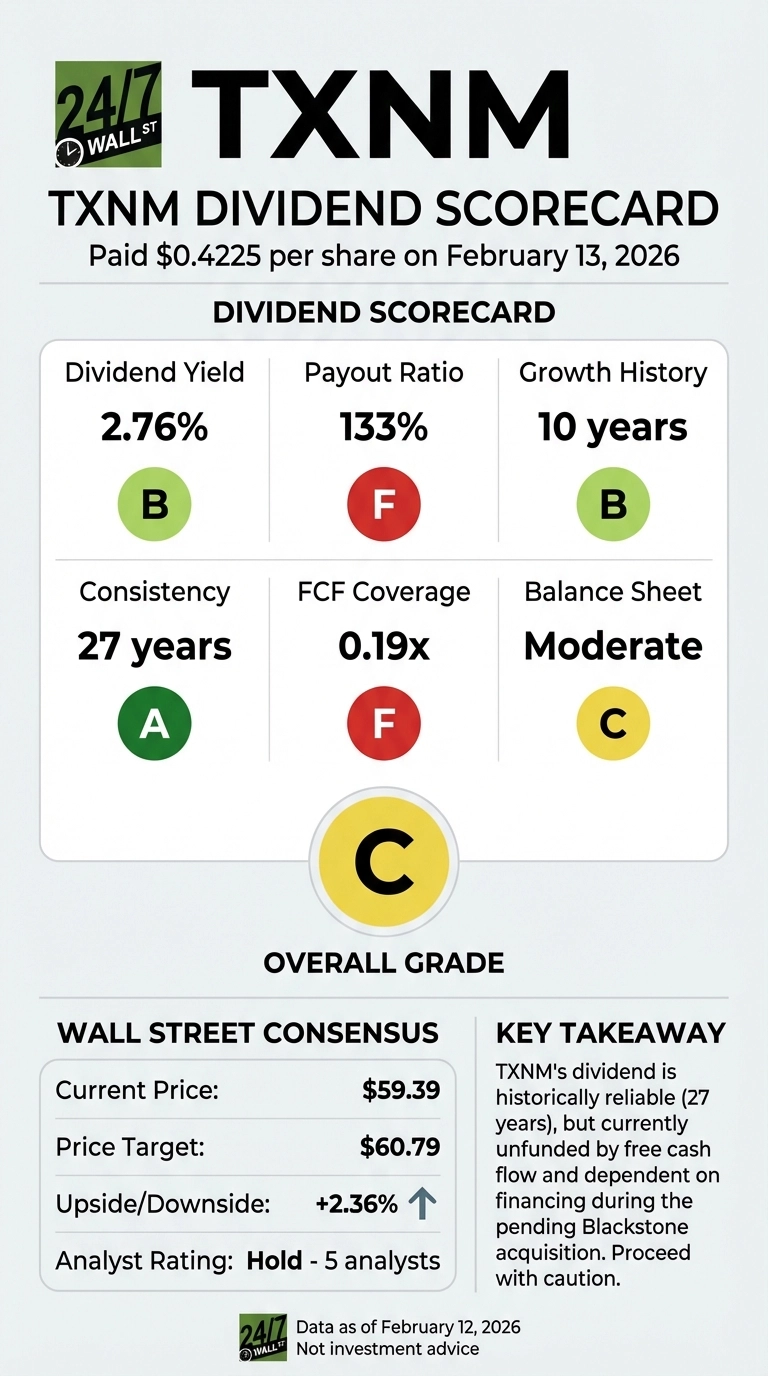

TXNM Energy just paid shareholders $0.4225 per share on February 13, 2026, marking a 3.7% increase from the previous quarter’s $0.4075 payment. The New Mexico and Texas utility has delivered 27 consecutive years of uninterrupted dividend payments, but a closer examination reveals warning signs that income-focused investors should understand before counting on this distribution.

The Dividend Profile: Steady Growth With Recent Momentum

TXNM’s dividend track record demonstrates consistency. The company has grown its quarterly payout from $0.22 in 2016 to $0.4225 in early 2026, representing 92% total growth over 10 years and a compound annual growth rate of approximately 6.8%. Recent annual increases have clustered in the 5-7% range, with the company maintaining a predictable quarterly payment schedule.

At the current stock price of $59.39, the annualized dividend of $1.63 translates to a yield of 2.76%. This sits just above the 2.75% yield offered by the Utilities Select Sector SPDR ETF, making TXNM marginally more attractive than the sector average on yield alone.

The Cash Flow Problem: Dividends Funded By Debt

The most concerning aspect of TXNM’s dividend is how the company funds it. Despite generating $508.2 million in operating cash flow during 2024, the utility spent $1.25 billion on capital expenditures, resulting in negative free cash flow of $738.9 million. This pattern has persisted for years. TXNM has posted negative free cash flow in every period from 2019 through 2024.

The company paid $140.3 million in dividends during 2024 while generating no free cash flow to support those payments. Instead, TXNM relied on $684.4 million in financing cash flow (primarily debt and equity issuances) to bridge the gap. Free cash flow coverage of the dividend stands at just 0.19x, meaning the company generates only 19 cents of free cash for every dollar it pays in dividends.

Capital expenditures have escalated dramatically, growing from 122% of operating cash flow in 2019 to 245% in 2024. This aggressive infrastructure investment program, driven by grid modernization, renewable energy transitions, and growing demand in Texas, has fundamentally altered the company’s cash flow profile.

Earnings Quality: Margin Improvement Masks Underlying Stress

TXNM’s earnings story shows recent improvement but reveals volatility. The company reported net income of $242.7 million in 2024, up 174.6% from $88.3 million in 2023. Net margin expanded from 4.6% to 12.3%, driven by gross margin improvement of 8.8 percentage points.

However, this recovery followed a difficult 2023 that included a $50.1 million net loss in Q4 alone. The most recent quarter (Q4 2025) showed net income of $130.71 million, essentially flat compared to $131.33 million in the prior-year period despite revenue growth of 13.69%.

The payout ratio based on reported earnings tells a troubling story. Using Q4 2025’s GAAP EPS of $1.22, the current quarterly dividend of $0.4075 represents a payout ratio exceeding 133%. Even using the company’s preferred non-GAAP EPS of $1.33, the payout ratio remains above 122%.

Interest expense has grown substantially, reaching $228.1 million in 2024, up from $190.4 million in 2023 and $127.9 million in 2022. This rising debt service burden (now consuming 11.6% of revenue) directly competes with dividend payments for available cash.

The Blackstone Acquisition: Uncertainty Ahead

TXNM operates under the shadow of a pending $11.5 billion acquisition by Blackstone Infrastructure, announced in May 2025. Shareholders have approved the deal, and the Public Utility Commission of Texas approved the acquisition in February 2026, noting it is “in the public interest” with $45 million in rate credits for customers.

However, the transaction still requires additional federal and state regulatory approvals and is expected to close in the second half of 2026. During this period, TXNM has suspended earnings guidance, creating a visibility gap for investors trying to assess dividend sustainability. The company’s previous attempted merger with Avangrid collapsed in 2021 after regulators rejected the deal, demonstrating that regulatory approval is not guaranteed.

CEO Don Tarry stated: “We have initiated the regulatory approval process for our transaction with Blackstone Infrastructure with filings that address the key issues raised during our conversations with local stakeholders and community groups.”

Balance Sheet Strength: The One Positive Signal

TXNM’s balance sheet provides the primary argument for dividend sustainability. Shareholders’ equity increased 28.76% year-over-year to $3.18 billion, strengthened by equity issuances. Total assets reached $11.68 billion, up 7.67%. The company maintains access to capital markets, which has proven essential for funding both infrastructure investments and dividend payments.

The debt-to-equity ratio of approximately 2.66x sits at the higher end of acceptable levels for regulated utilities but remains manageable given the predictable cash flows inherent to the utility business model.

Total Return Performance

Investors have benefited from strong price appreciation alongside dividend income. Over the past year, TXNM shares have gained 22.03%, significantly outpacing the dividend contribution. The five-year return of 43.19% and ten-year return of 150.11% demonstrate that capital gains have driven the majority of total returns.

This price performance likely reflects both the pending acquisition premium and investor optimism about growth prospects in Texas, where strong demographic growth and data center electricity demand are driving infrastructure needs.

The Verdict: A Dividend On Borrowed Time

TXNM’s dividend payment history deserves respect. 27 years without interruption and consistent growth demonstrate management commitment. However, the current dividend is not supported by free cash flow generation. The company is essentially borrowing money to pay dividends while investing heavily in infrastructure, a strategy that works only as long as capital markets remain accessible and regulators continue approving rate increases.

The 2.76% yield barely exceeds the sector average, offering minimal compensation for the elevated risk of holding a single utility stock versus a diversified fund. Operating cash flow coverage of 27.6% suggests the dividend could survive if capital spending normalizes, but the current trajectory shows capex intensifying rather than moderating.

The pending Blackstone acquisition adds another layer of uncertainty. While private equity ownership could provide patient capital for infrastructure investments, it could also lead to dividend policy changes once the deal closes. The lack of earnings guidance during the transaction period prevents investors from modeling future cash flows with any confidence.

For income investors, TXNM represents a dividend that has been reliable historically but faces structural challenges ahead. The payment will likely continue in the near term, supported by the company’s ability to access capital markets and the regulatory framework that allows utilities to pass infrastructure costs to customers. However, calling this a sustainable dividend in its current form requires ignoring the negative free cash flow, elevated payout ratios, and dependence on external financing that define TXNM’s current financial reality.