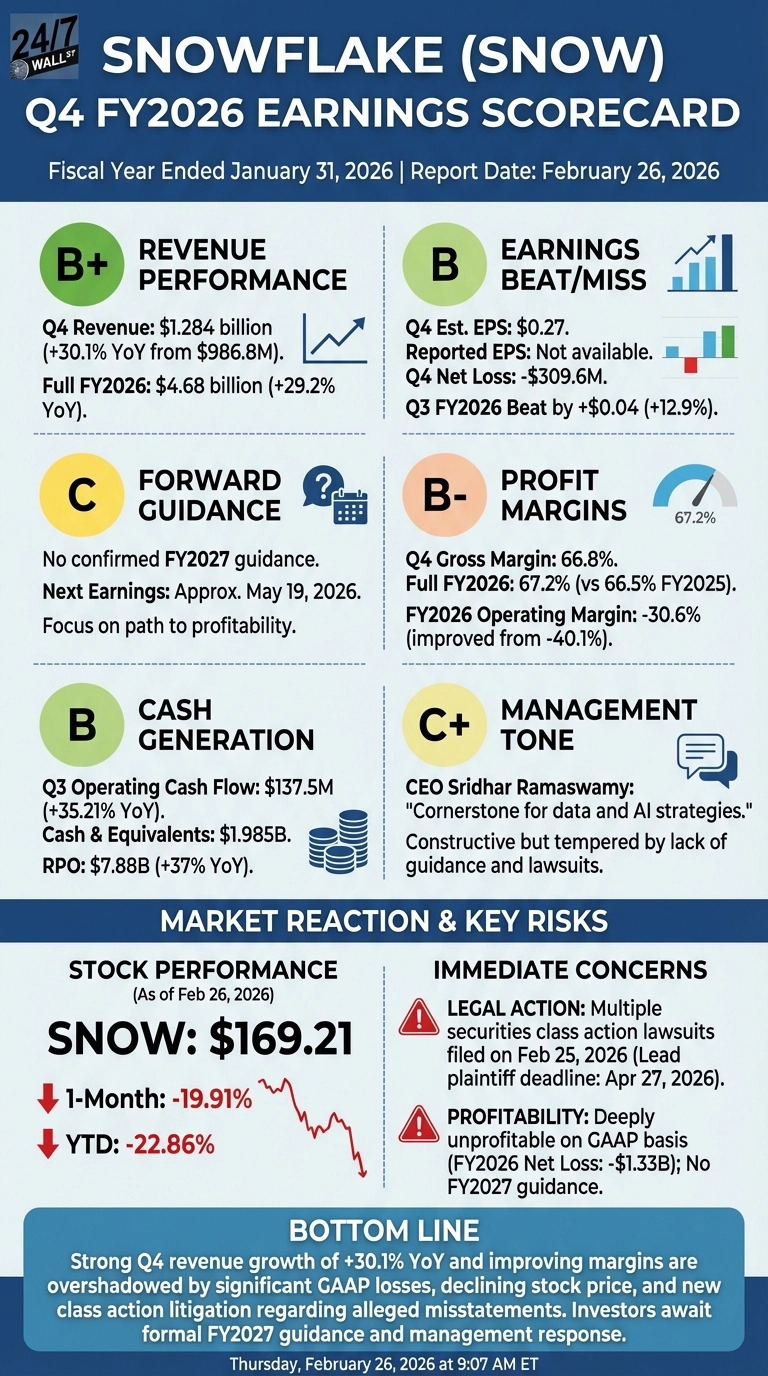

Snowflake closed out fiscal year 2026 with its strongest quarterly revenue on record, but a sharp stock decline signals investors are weighing more than just the top-line beat. Shares fell to $169.21 as of February 25, 2026, down nearly 20% over the prior month and nearly 23% year-to-date, as compounding concerns around profitability and newly filed securities class action lawsuits weigh on sentiment.

Q4 FY2026 Earnings Scorecard

| Category | Grade | Key Insight |

|---|---|---|

| Revenue Performance | B+ | Q4 revenue came in at $1.284 billion, up 30.1% year-over-year from $986.8 million, continuing a consistent growth trajectory across all four quarters of FY2026. |

| Earnings Beat/Miss | B | The analyst consensus EPS estimate for Q4 FY2026 stood at $0.27; actual reported EPS figures are not yet confirmed in available data, though the income statement shows a net loss of $309.6 million for the quarter. Prior quarters beat estimates: Q3 came in at $0.35 vs. $0.31 estimated (+13%). |

| Forward Guidance | C | No confirmed FY2027 guidance is available in current data. Next earnings are tentatively expected around May 19, 2026. Investors are watching whether management will provide a credible path to profitability. |

| Profit Margins | B- | Gross margin held at 66.8% in Q4, and the full-year FY2026 gross margin of 67.2% improved from 66.5% in FY2025. The operating loss narrowed meaningfully year-over-year, with the full-year operating margin improving to -30.6% from -40.1%. |

| Cash Generation | B | Operating cash flow in Q3 FY2026 grew 35.21% year-over-year to $137.5 million, with $1.985 billion in cash on the balance sheet. Remaining performance obligations of $7.88 billion, up 37% year-over-year, signal strong future revenue visibility. |

| Management Tone | C+ | CEO Sridhar Ramaswamy stated “Snowflake is the cornerstone for our customers’ data and AI strategies, driving real business impact at scale.” The tone was constructive, though the absence of detailed FY2027 guidance and the overhang from multiple securities class action lawsuits filed on February 25, 2026 temper confidence. |

Bottom Line

Snowflake’s Q4 results reflect a business still growing at a compelling pace, with full-year FY2026 revenue reaching $4.68 billion, up 29.2% year-over-year, and gross margins holding firm above 67%. The operating loss trajectory is improving, but the company remains deeply unprofitable on a GAAP basis. The more immediate concern is legal: multiple law firms including Rosen Law and Robbins LLP filed securities class action lawsuits on February 25, 2026, alleging misstatements related to product efficiency features and their impact on revenue. A lead plaintiff deadline of April 27, 2026 keeps this story active in the near term. Investors should watch for formal FY2027 guidance and any management response to the litigation before drawing conclusions about the stock’s direction.