For the better part of two decades, Wall Street operated under a simple assumption: when markets wobble, the Federal Reserve eventually steps in. That expectation shaped everything from stock valuations to bond prices to corporate borrowing. But what happens when the next Fed chair no longer views protecting asset prices as part of the job?

That is the likelihood after the Senate Banking Committee advanced Kevin Warsh as President Donald Trump’s nominee to replace Jerome Powell. Powell’s term as Fed chair ends May 15, and a full Senate confirmation vote is expected before then.

If confirmed, Warsh appears ready to reshape the Federal Reserve in ways markets may not fully appreciate yet.

Warsh Thinks the Fed Lost Its Way

Warsh has not been subtle about his criticism of Powell or the central bank more broadly.

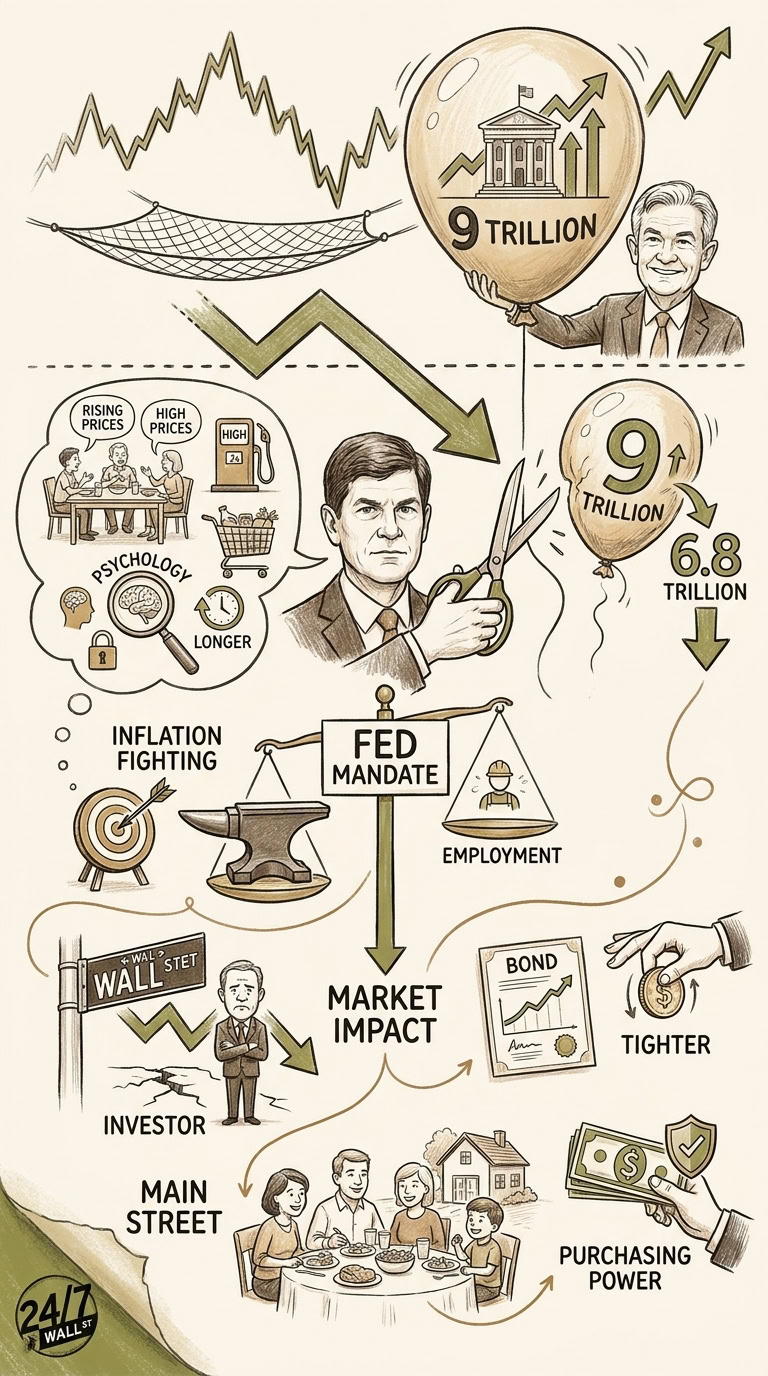

During his Senate Banking Committee testimony, Warsh argued inflation remains a problem because Americans still talk about rising prices “around kitchen tables and boardrooms.” He added that his preferred definition of price stability is simple: inflation is solved only when “no one’s talking about it.”

That may sound rhetorical, but it signals a deeper philosophical shift.

The Fed officially targets 2% inflation using the Personal Consumption Expenditures index, or PCE. March core PCE rose 2.8% year over year, according to the Bureau of Economic Analysis. Under Powell, the Fed has treated inflation as manageable so long as it trends toward that target over time.

Warsh disagrees.

He believes the Fed under Powell damaged its credibility by waiting too long to respond after inflation peaked at 9.1% in June 2022. In his view, inflation expectations matter as much as inflation data itself.

That’s another way of saying people’s psychology matters. If consumers and businesses expect prices to keep rising, inflation can become self-reinforcing even after headline numbers cool. For investors, that could mean a more aggressive Fed willing to keep interest rates higher for longer — even if markets dislike it.

The Balance Sheet Battle Could Reshape Markets

The biggest market impact could emerge with Warsh’s attack on the Fed’s balance sheet.

Before the 2008 financial crisis, the Federal Reserve’s balance sheet totaled less than $1 trillion. After years of quantitative easing and subsequent pandemic stimulus programs, it expanded to nearly $9 trillion in 2022. Even after two years of quantitative tightening, the balance sheet still sits near $6.8 trillion today, according to Federal Reserve data.

Warsh has repeatedly criticized that expansion. He argues the Fed became too involved in financial markets by purchasing massive amounts of Treasury bonds and mortgage-backed securities. In his view, those policies inflated asset prices, distorted risk-taking, and worsened wealth inequality by disproportionately benefiting investors who owned stocks and real estate.

Wall Street may not welcome a Fed chair trying to aggressively shrink that support system.

Here’s why the market cares:

| Fed Policy | Wall Street Impact |

| Large bond purchases | Lower Treasury yields, higher stock valuations |

| Expanded balance sheet | More market liquidity |

| Lower long-term rates | Cheaper corporate borrowing |

| Faster balance sheet reduction | Tighter financial conditions |

Surprisingly, the concern is not just about stocks. Treasury markets could also become more volatile if the Fed steps back as a major buyer of government debt while federal deficits continue running above $1.5 trillion annually, according to Congressional Budget Office projections.

That combination could push long-term yields higher — pressuring growth stocks, housing, and corporate financing costs.

Warsh Wants a Different Fed Mandate

The bigger change may involve the Fed’s core mission itself. Congress currently gives the Federal Reserve a “dual mandate”: maximize employment while maintaining stable prices. Warsh appears ready to tilt that balance more toward inflation fighting.

Granted, he has not explicitly called for abandoning the employment mandate. But his testimony and speeches suggest he believes the Fed spent too much time supporting labor markets and financial conditions after the pandemic while underestimating inflation risks.

Under Powell, the unemployment rate fell to 3.4% in 2023 — the lowest level since 1969 — while the Fed delayed rate hikes because officials believed inflation would prove “transitory.” Warsh argues that mistake damaged Main Street more than Wall Street because inflation hits essentials first — groceries, rent, gasoline, insurance, and utilities.

In any case, his framework implies the Fed may tolerate slower economic growth or even higher unemployment if that is what it takes to fully extinguish inflation pressures. Markets rarely enjoy hearing that.

Historically, investors benefited from the so-called “Fed put” — the belief the central bank would ease policy whenever economic conditions weakened sharply. Warsh’s comments suggest he may be less interested in cushioning markets and more focused on restoring institutional credibility.

Key Takeaway

In short, Kevin Warsh is not offering investors a continuation of the Powell era. He is proposing a reset. A more inflation-focused Fed could strengthen long-term confidence in the dollar, reduce speculative excesses, and restore credibility after the inflation surge of 2021 and 2022. Investors should not dismiss those benefits.

Still, the transition could prove uncomfortable for markets accustomed to easy money and rapid policy support during downturns. Higher bond yields, tighter liquidity, and a Fed less willing to rescue markets would likely pressure richly valued growth stocks first. But everyday Americans may welcome a central bank more focused on preserving purchasing power than protecting asset prices.

When all is said and done, Warsh’s message is clear: the Fed’s primary job is defending the value of money itself — even if Wall Street has to relearn how to live without constant support.