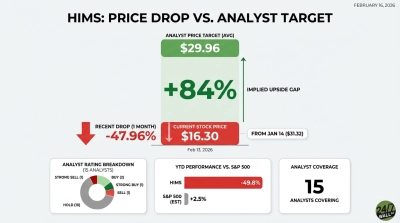

Two healthcare names are drawing fresh analyst attention this week as Wall Street recalibrates around a landmark GLP-1 truce and a fertility benefits company navigating a murky 2026 outlook. Barclays analyst Glen Santangelo raised his price target on Hims & Hers Health to $29 from $25, keeping an Overweight rating, after the company’s deal with Novo Nordisk removed a significant legal cloud from the stock. Meanwhile, Canaccord trimmed its price target on Progyny (NASDAQ:PGNY | PGNY Price Prediction) to $19 from $26 while maintaining a Hold, citing stable but uncertain business trends following Q4 results. Hims & Hers Health (NYSE:HIMS) is the other name in focus this week.

| Ticker | Company | Firm | Old → New Rating | New Price Target | One-Line Takeaway |

|---|---|---|---|---|---|

| HIMS | Hims & Hers Health | Barclays | Overweight → Overweight | $29 (from $25) | Legal overhang cleared; Barclays sees market underpricing new product opportunity |

| PGNY | Progyny | Canaccord | Hold → Hold | $19 (from $26) | Stable trends but cautious guidance keeps analyst on the sidelines |

The Analyst’s Case

Santangelo’s note frames the Novo Nordisk agreement as a dual catalyst. The rally following the deal highlights the incremental market opportunity and removal of the legal overhang for Hims & Hers shares, the analyst told investors. Beyond the deal itself, Barclays argues the market is still underappreciating Hims’ opportunity from new products — a signal that the firm sees the stock’s recent recovery as just the beginning of a re-rating, not the end of it.

The deal itself resolved a lawsuit Novo Nordisk filed in February after Hims launched and then pulled a compounded version of the Wegovy pill. Under the new arrangement, Hims will distribute approved Ozempic and Wegovy injectables, as well as the oral Wegovy pill, at Novo’s self-pay prices on its platform, while agreeing to stop advertising compounded GLP-1 drugs outside of clinically necessary cases. The FDA publicly endorsed the resolution, with commissioner Marty Makary calling the deal a win for access and affordability.

Canaccord’s trim reflects a straightforward post-earnings model update. The firm updated its model following Q4 results, which suggests business trends appear stable, but the uncertain outlook and environment keeps them cautious on the shares. With revenue growth decelerating and management repeatedly flagging variability in member engagement as a 2026 wildcard, Canaccord sees limited near-term catalyst to move off the sidelines.

Company Snapshot & Recent Performance

Hims & Hers had a turbulent 12 months heading into this week’s news. The stock is down 27.72% year-to-date and 31.91% over the past year, weighed down by regulatory uncertainty around compounded GLP-1 medications and the fallout from the original Novo partnership collapse in Q2 2025. But the Novo deal announced March 9 triggered an immediate market response: shares surged 48.36% in the week ending March 10, with the most recent trading day adding another 5.91%. The stock currently trades at $23.47.

Operationally, Hims delivered a strong finish to fiscal 2025. Full-year revenue reached $2.347 billion, up 59% year-over-year, with Q4 revenue of $617.82 million beating consensus estimates. The subscriber base crossed 2.5 million, growing 13% year-over-year, and monthly revenue per subscriber reached $83, up 11% year-over-year. The company’s international segment accelerated sharply, with Rest of World revenue up 825% year-over-year in Q4 from a small base.

Progyny has had an even steeper slide. Shares are down 30.26% year-to-date and sit at $17.91 — just above the 52-week low of $16.75 hit on March 4. The drop accelerated after Q4 earnings in late February, when shares fell roughly 22% as weak 2026 guidance overshadowed a solid quarter. Full-year 2025 revenue came in at $1.289 billion, up 10.4% year-over-year, with record adjusted EBITDA of $222.09 million and record operating cash flow of $210.19 million. The company carries no debt and ended the year with $112.24 million in cash.

Why the Move Matters Now

For Hims, the Barclays target raise arrives at an inflection point. The legal dispute with Novo was arguably the single largest overhang on the stock — it raised the specter of regulatory action, revenue disruption, and reputational damage all at once. With that risk now resolved and a formal distribution agreement in place, the investment thesis shifts from “can they survive the regulatory crackdown” to “how much can they grow through the Wegovy partnership.” Barclays raised its price target to $29 from $25, maintaining an Overweight rating, though the consensus average target sits at $23.12 — suggesting Barclays is notably more optimistic than the broader analyst community, which skews toward Hold ratings.

The company’s own 2026 guidance projects revenue of $2.7 billion to $2.9 billion and adjusted EBITDA of $300 million to $375 million, though that guidance explicitly assumes continued access to compounded semaglutide, a variable that the Novo deal partially addresses but does not fully eliminate. Capex is also climbing fast: full-year capital expenditures hit $242.59 million in 2025, up 137.61% year-over-year in Q4 alone, as the company invests heavily in pharmacy automation.

For Progyny, the Canaccord cut from $26 to $19 reflects a meaningful reset in expectations. The firm’s prior target implied significant upside that the guidance trajectory no longer supports. The company’s 2026 revenue guidance of $1.355 billion to $1.405 billion represents growth of just 5.1% to 9.0% — a sharp deceleration from 2025’s 10.4% pace and well below what the stock was priced for heading into earnings. Short interest surged 41% to 4.02 million shares in February 2026, reflecting growing skepticism even as the fundamental business remains profitable and debt-free. The departure of Progyny’s president at year-end 2025 adds a leadership dimension that investors are watching closely.

The consensus analyst price target for Progyny stands at $28.64, well above current trading levels, and the overall rating remains a moderate buy with 7 Buy ratings and 2 Hold ratings among covering analysts. Canaccord’s trim pulls in the same direction as recent cuts from Jefferies, Truist, and KeyBanc, all of whom lowered targets following Q4 results.

Context and Analyst Outlook

The Barclays upgrade on Hims is a meaningful signal that one of the key regulatory risks hanging over the stock has been resolved but analysts note that the stock already absorbed much of that news in a 48% one-week surge. The forward question is whether the Wegovy distribution deal can offset the margin pressure that comes with selling branded drugs at Novo’s self-pay prices rather than higher-margin compounded alternatives. Hims carries approximately $1 billion in convertible debt and a free cash flow profile that turned negative in Q4, factors analysts have noted when assessing the company’s financial picture even as the regulatory clouds clear.

For Progyny, the Canaccord target cut to $19, barely above the stock’s current price, reflects a narrowed gap between the target and current trading levels. The company’s debt-free balance sheet, active buyback program, and record 2025 cash generation are genuine strengths, but the 2026 guidance range and member engagement uncertainty have made it difficult for analysts to build a high-conviction bull case. The stock trades at a forward P/E of roughly 9x, and analysts note near-term catalysts are limited until the company demonstrates its 2026 growth trajectory is stabilizing.