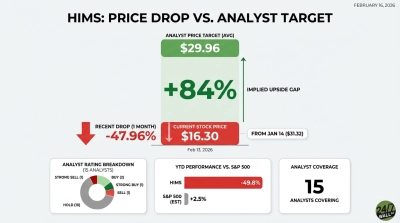

Hims & Hers Health (NYSE:HIMS) looked like a fallen growth star earlier this year. The telehealth platform was hammered by the FDA’s aggressive crackdown on compounded GLP-1 drugs, complete with warning letters accusing misleading marketing. Threats of Justice Dept. criminal investigations loomed, and Novo Nordisk (NYSE:NVO | NVO Price Prediction) slapped the company with a patent-infringement lawsuit over knockoff semaglutide. Shares cratered more than 75% from their peak.

Then came the surprise truce announced last Friday: Novo dropped the lawsuit (while reserving the right to refile), and Hims agreed to sell branded Wegovy and Ozempic — including the new oral Wegovy pill — directly on its platform. Hims will also stop advertising compounded versions except on a limited scale and transition most patients to the real thing. The market roared back. Since the deal, HIMS stock has soared 64%, capped by a stunning 40% one-day gain. With its growth engine seemingly restarted, is Hims the growth stock Wall Street now believes it is?

The Magnet That Powered — and Nearly Destroyed — Hims

GLP-1 medications have been central to Hims’ meteoric rise — and its recent near-collapse. Compounded versions of semaglutide and tirzepatide hundreds of thousands of new subscribers. Last year, Hims boasted roughly 418,000 weight-loss customers. These low-cost offerings (often around $199 to $300 per month) not only delivered direct sales but acted as a powerful funnel: once patients signed up for GLP-1s, many stayed for Hims’ core offerings — hair-loss treatments, erectile-dysfunction meds, skincare, and mental-health services. Cross-selling turned one-time weight-loss buyers into high-lifetime-value subscribers across the platform.

The compounded drugs carried risks, however. Regulatory scrutiny highlighted safety concerns around unapproved formulations, inconsistent dosing, and aggressive advertising. The FDA’s warnings last month and DOJ referrals created a cloud of legal and reputational danger. Hims’ pivot to branded products removes that taint.

Selling authentic Ozempic and Wegovy at self-pay prices comparable to other telehealth platforms instantly elevates the company’s profile. Questions about counterfeit safety or patent violations have been removed. Patients get FDA-approved drugs with proper labeling and supply-chain integrity, while Hims gains credibility as a legitimate healthcare partner rather than a compounding disruptor.

Branded Legitimacy Meets Elevated Valuations

The partnership delivers instant legitimacy. Hims now sits alongside established telehealth players offering the same blockbuster drugs, broadening appeal to risk-averse consumers and potentially opening doors to insurance or employer partnerships down the line. Analysts have responded with upgrades: Needham raised its rating to Buy with a $30 target, while Citi, Bank of America, and Deutsche Bank lifted price targets and moved to Hold. Revenue also projections remain robust — $2.35 billion in 2025 (up 59% year-over-year) with continued double-digit growth expected.

Yet the stock now trades at multiples that even the Novo deal struggles to justify. Forward sales multiples remain elevated relative to peers, and some analysts note that branded GLP-1s come with thinner margins than the high-profit compounded versions Hims previously enjoyed. While the legal overhang is gone, valuation concerns remain. Much depends on how quickly Hims can migrate its existing base to the pricier branded options without losing subscribers, and how much limited-scale compounding revenue remains.

The market’s 64% rebound already prices in a flawless handoff; any hiccup in patient retention or slower-than-expected branded uptake could pressure shares.

Key Takeaways

Even setting valuation aside, deeper risks remain. Hims and Novo have danced this dance before. A 2025 collaboration to sell branded Wegovy collapsed after less than two months. The concerns then — pricing, marketing, and control — were reportedly resolved this time, but history suggests partnerships can sour quickly.

Today, Hims becomes heavily dependent on a single supplier for its biggest growth engine. If Novo encounters production constraints, faces its own regulatory headaches (it is currently under FDA scrutiny over adverse-reaction reporting for GLP-1 drugs), or decides the telehealth channel no longer serves its interests, Hims’ momentum could evaporate overnight.

The truce has undeniably reignited Hims’ growth narrative and scrubbed away the compounded-drug stigma. Branded GLP-1 access plus cross-selling power gives the platform real staying power. But investors chasing the 64% surge must weigh the restored tailwind against single-supplier dependency and rich valuations.

Hims & Hers may indeed be a growth stock worth owning again — just not without acknowledging it could swing violently if the Novo partnership hits another rough patch.