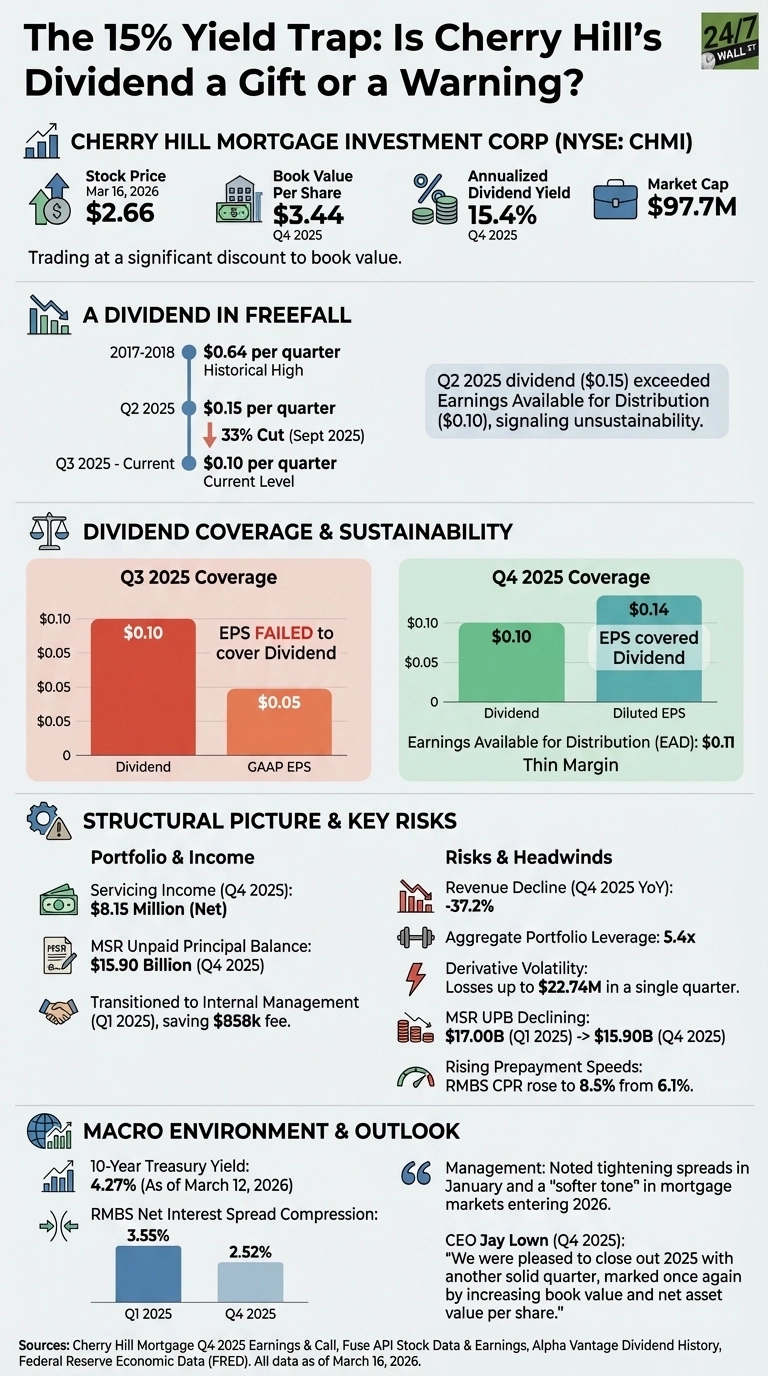

Founded in 2012, Cherry Hill Mortgage Investment Corporation, a prominent real estate finance company (NYSE:CHMI) is flashing a 15.04% annualized dividend yield at a stock price of $2.66, trading at a meaningful discount to a book value of $3.44 per share. For income investors, the number is hard to ignore, but you have to dig into the history to know why it deserves attention.

Cherry Hill Mortgage Investment Corporation (CHMI)

A Dividend in Freefall

This yield did not arrive from strength, as Cherry Hill’s dividend has been cut repeatedly over recent years, and quarterly payouts that once reached $0.49 per share in 2017-2018 have been reduced in stages to the current $0.10 per quarter. The most recent cut came in September 2025, when the board slashed the payout by 33% from $0.15, following a Q2 2025 quarter in which the $0.15 dividend exceeded earnings available for distribution of $0.10 per share, a clear signal that the prior rate was unsustainable.

Overall, coverage has been inconsistent, and in Q3 2025, GAAP EPS of $0.05 failed to cover the $0.10 dividend. Q4 2025 offered more relief, with diluted EPS of $0.14 covering the $0.10 payout with some cushion. However, earnings available for distribution came in at just $0.11 per share, leaving a thin margin above the dividend.

What the Numbers Actually Show

The structural picture is mixed as book value has recovered incrementally, rising from $3.34 in Q2 2025 to $3.36 by Q4 2025. Servicing income has been the portfolio’s backbone, generating $8.15 million in net servicing income in Q4 on an MSR unpaid principal balance of $15.90 billion. Management completed a transition to internal management in Q1 2025, eliminating an $858,000 external management fee.

On the other side, Q4 2025 revenue fell 37.2% year-over-year. The MSR portfolio has been shrinking, with the unpaid principal balance declining from $17.00 billion in Q1 2025 to $15.90 billion by Q4. Leverage stands at 5.4x, and derivative volatility has generated losses of up to $1.9 million in a single quarter. Prepayment speeds are rising: RMBS CPR rose to 8.5% from 6.1%, with the potential to reach 15% if mortgage rates fall to 5.5%.

Rate Environment Adds Complexity

The macro backdrop is not straightforward, as the 10-year Treasury yield currently sits at 4.27%, having risen sharply in recent weeks. Cherry Hill’s RMBS net interest spread compressed from 2.52% in Q1 2025 to 2.52% by Q4 2025. Meanwhile, management noted tighter spreads in January and a “softer tone” in mortgage markets entering 2026, in contrast to the more supportive Q4 environment.

CEO Jay Lown offered a measured tone on the quarter: “We were pleased to close out 2025 with another solid quarter, marked once again by increasing book value and net asset value per share.” The board has confirmed the $0.10-per-share dividend for Q1 2026, payable on April 30, 2026. The yield is real for now. Whether the earnings base can sustain it through a more challenging rate environment in 2026 is the question investors need to answer for themselves.

Data Sources

- Cherry Hill Mortgage Q4 2025 Earnings Report and Q4 Earnings Call Highlights provided earnings coverage, EAD figures, prepayment speed data, and management commentary on 2026 market conditions.

- Fuse API stock data and earnings history provide quarterly EPS, book value, MSR UPB, leverage, dividend history, and price performance metrics.

- Alpha Vantage’s dividend history and company overview provided the full dividend cut timeline from 2013 to present and current analyst price targets.

- The Federal Reserve Economic Data (FRED) via the Fuse API provided the 10-year Treasury yield context and yield-curve spread analysis relevant to RMBS spread sustainability.