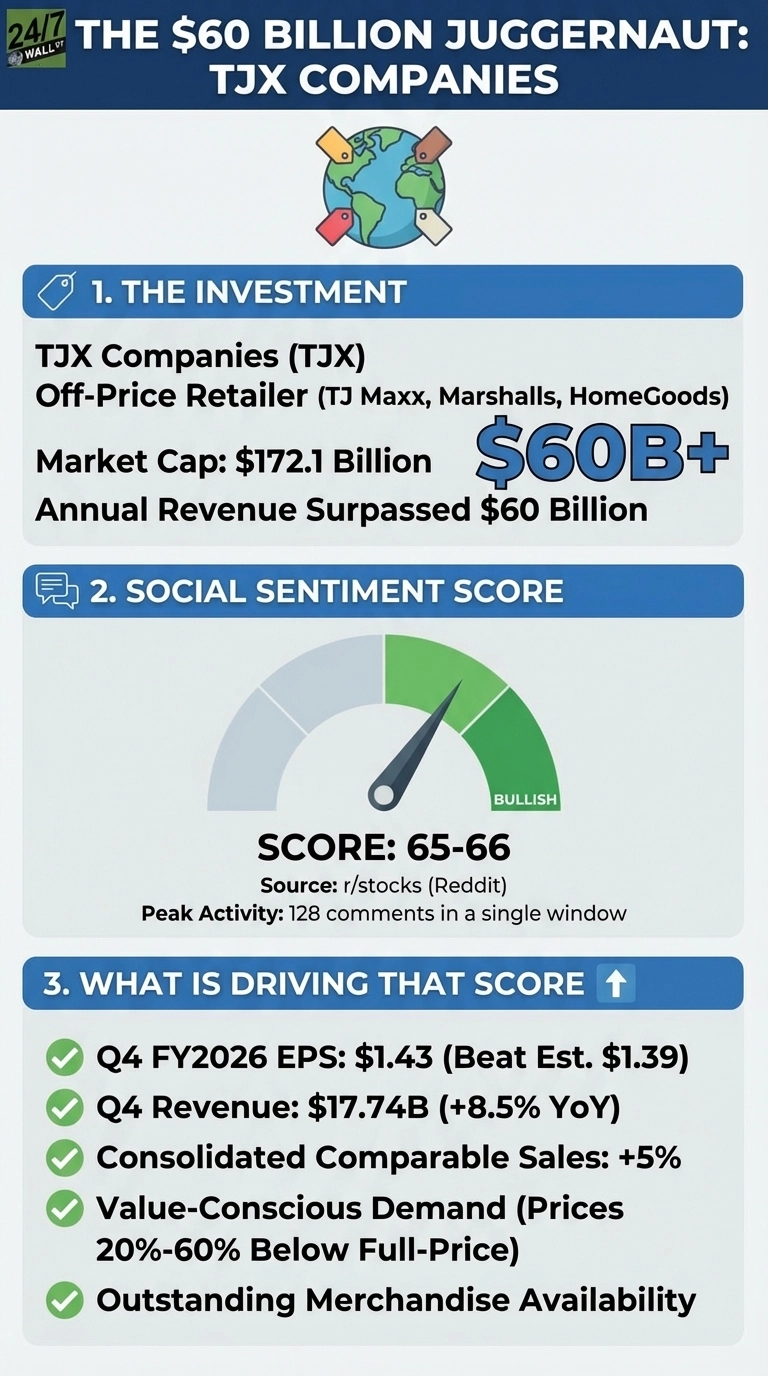

A beloved retailer across its store portfolio, TJX Companies (NYSE:TJX | TJX Price Prediction) just crossed a milestone most retailers only dream about: annual revenue surpassing $60 billion for the first time. Shares sit around $154, roughly flat since the February earnings beat, while the broader market has pulled back sharply. Retail investors on Reddit have noticed, and the debate centers on whether TJX’s structural advantages justify a valuation with little room for error.

TJX Companies’ Q4 FY2026 report, which was released on February 25, 2026, was broadly strong as EPS came in at $1.43, beating the $1.39 estimate, while revenue of $17.74 billion topped expectations of $17.38 billion and grew 8.5% year over year. Every division delivered: TJX Canada led with 7% comp growth, HomeGoods posted 5%, Marmaxx came in at 5%, and TJX International contributed 4%. CEO Ernie Herrman called the full-year result a “major milestone,” and Full-year operating income grew 13.9% to $7.18 billion, and free cash flow hit $4.92 billion, up 17.1%.

The macro backdrop favors TJX right now as data from the University of Michigan consumer sentiment index has spent most of the past year below 60, touching a trough of 51.0 in November 2025 and recovering only to 56.4 as of January 2026, levels associated with recessionary consumer behavior. That’s exactly the environment where TJX’s model of selling branded merchandise at 20% to 60% below full-price retailers attracts the most traffic.

r/stocks Is Bullish, But the Valuation Debate Is Real

Reddit sentiment for TJX has been consistently bullish over the past 30 days, with scores holding at 65 to 66 throughout the period, concentrated in r/stocks, where peak engagement hit 128 comments in a single window on Sunday, March 22. Community members have been debating whether TJX’s off-price model justifies its premium valuation, with the tension reflecting broader uncertainty about retail valuations in the current environment.

The bulls cite tariff-driven inventory windfalls, dividend growth, and store expansion. The skeptics keep circling back to price.

Three reasons the bullish case resonates:

- TJX benefits directly from tariff disruption: brands seeking alternative distribution channels increase quality merchandise available to off-price buyers, strengthening TJX’s inventory position at a time when management called merchandise availability “outstanding”

- TJX raised its quarterly dividend 13% to $0.425 per share, with plans to repurchase $2.50 to $2.75 billion in FY2027, signaling management’s confidence in cash generation

- The company added 129 net new stores in FY2026, bringing the total store count to over 5,000 locations across nine countries, expanding the physical footprint while competitors contract

The counterargument is valuation. TJX trades at a trailing P/E of roughly 32x and a forward multiple of 30x, with a return on equity of 59.1%. The composite sentiment score stands at 66.24, but the r/stocks crowd has flagged that a consumer spending slowdown could compress multiples even if earnings hold.

Ross Stores Adds Competitive Context

The closest peer is Ross Stores (NASDAQ:ROST), which reported revenue up 12% to $6.64 billion, same-store sales up 9%, and guided for Q1 comparable sales growth of 3% to 4%. That guidance is more aggressive than TJX’s own FY2027 comp outlook of 2% to 3%. Ross trades at a meaningful discount to TJX on a price-to-earnings basis, a talking point for investors weighing which off-price operator offers better risk-adjusted upside.

The next catalyst for TJX will be its Q1 FY2027 earnings, as management guided for Q1 EPS of $0.97 to $0.99 and called the quarter “off to a strong start.” With the stock up 33% over the past year while the S&P 500 has pulled back, TJX has earned its reputation as a defensive compounder. Whether it can sustain that premium at 30x forward earnings in a softening consumer environment is the question r/stocks keeps returning to.